7 Cash Stuffing Tips to Organize Your Monthly Budget and Fund Your Side Hustle

Did you know that an estimated 82% of new online entrepreneurs and freelancers fail because of poor cash flow management? They spend months researching how to build passive income and generate online earnings, but they completely neglect their personal finances. If your personal budget is chaotic, trying to scale a work from home business will feel like pouring water into a leaky bucket. You cannot achieve true financial freedom if you don’t know exactly where your money is going.

This is where the power of cash stuffing comes in. Cash stuffing is a highly effective, tactile budgeting method that forces you to allocate every physical dollar to a specific category. By getting hands-on with your money, you plug the leaks in your finances, drastically improve your personal profit margins, and free up the seed capital needed to launch your next big venture.

Quick Answer

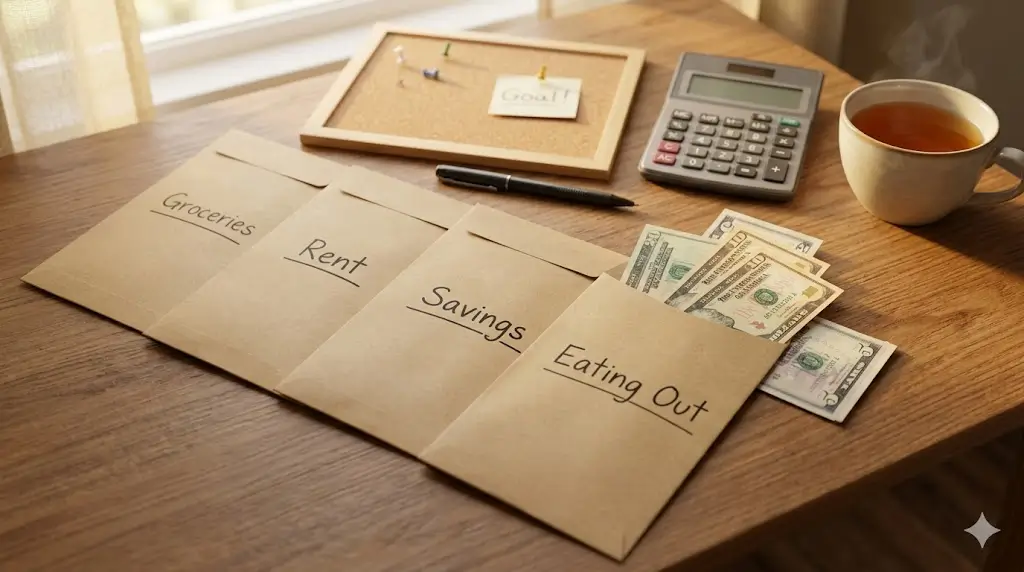

Cash stuffing involves cashing your paycheck and physically dividing the bills into labeled envelopes for different spending categories (like groceries, gas, or side hustle funding). To organize your monthly budget successfully, start by tracking your expenses, setting strict envelope limits, and never spending outside of what is physically inside that specific envelope.

What You’ll Need to Get Started

Before you can organize your budget to maximize your income potential, you need to gather a few simple tools. Treating this process like the foundation of your future digital income is crucial.

- A Cash Stuffing Binder: A specialized binder with clear, zippered envelopes (usually A6 size).

- Initial Investment: $10 to $30 for a high-quality budgeting binder on Amazon or Etsy. (Free alternative: regular paper mailing envelopes and a sharpie).

- Budget Tracking Sheets: To write down your incoming cash and outgoing allocations.

- A Reliable Bank Account: You still need a bank to receive your primary income and pay digital bills before withdrawing your physical cash.

- Clear Financial Goals: Know exactly why you are saving—whether it’s to pay off debt, build an emergency fund, or buy equipment for your side hustle.

Time Investment

Implementing a strict budgeting system requires a little upfront work, but the return on investment is massive when it comes to long-term wealth building.

- Setup Time Required: 1 to 2 hours to review your past bank statements, calculate your monthly fixed expenses, and create your initial envelope categories.

- Daily/Weekly Time Commitment: 15 to 30 minutes a week to physically stuff your envelopes, track your spending, and balance your remaining cash.

- Timeline to First Results: Most beginners see a tangible difference in their savings within 30 to 60 days. By month three, you will have established a solid baseline, freeing up consistent cash to invest in new revenue streams.

Step-by-Step Implementation Guide

1. Calculate Your Baseline “Profit Margins”

Treat your personal household like a business. Before you withdraw any money, calculate your total monthly income and subtract your fixed digital bills (rent, utilities, software subscriptions). The remaining amount is your household “profit margin”—this is the cash you will be stuffing.

2. Define Your Variable Spending Categories

Create specific envelopes for expenses that fluctuate. Common categories include Groceries, Dining Out, Gas, Personal Care, and Entertainment. Pro tip: Keep your categories broad enough to be manageable; having 30 different envelopes will cause immediate burnout.

3. Create a “Digital Income Seed Fund” Envelope

If your goal is to make money online, you need capital. Dedicate one envelope strictly to funding your monetization strategies. Whether it is $20 or $100 a month, physically stuffing cash into a “Business” or “Side Hustle” envelope builds the psychological commitment required to succeed.

4. Withdraw and Stuff Systematically

Go to the bank, withdraw your variable budget in cash, and physically place the designated amounts into their respective envelopes. The psychological weight of parting with physical cash is proven to reduce impulse buying compared to swiping a credit card.

5. Follow the “Empty means Empty” Rule

This is the most critical step. If your “Dining Out” envelope runs out of cash on the 20th of the month, you are eating at home for the remaining ten days. Do not borrow from your “Groceries” or “Business” envelopes to fund a lifestyle choice.

6. Track Every Single Cent

Keep a ledger inside your binder. Write down every purchase and the remaining balance of the envelope. This data is crucial. If you constantly run out of grocery money but have leftover entertainment money, you need to adjust your allocations next month.

7. Reinvest Your Leftovers

At the end of the month, take any leftover physical cash and roll it over into your savings, debt payoff, or your side hustle envelope. This rollover strategy is how standard budgeting transforms into wealth creation.

Savings & Income Potential Breakdown

While cash stuffing is a savings mechanism, the money you retain effectively acts as a tax-free raise. By optimizing your budget, you gather the capital required to unlock serious online earnings.

- Beginner Savings Potential: Most users report saving $200 – $400 a month simply by curbing impulse spending at the grocery store and restaurants.

- Intermediate Capital Generation: Saving $300 a month equals $3,600 a year. That is enough seed capital to launch a high-quality drop-shipping store, fund an affiliate marketing blog, or invest in premium digital courses.

- The ROI of Budgeting: If you take the $3,600 saved through cash stuffing and invest it into a side hustle that generates a modest 20% return, your disciplined budgeting has directly created a brand new, profitable income stream.

Alternative Methods & Variations

If carrying large amounts of physical cash makes you uncomfortable, there are excellent variations of this strategy:

- Digital Cash Stuffing: Use apps like Goodbudget or YNAB (You Need A Budget). These apps act as digital envelopes, requiring you to allocate every dollar electronically.

- The 50/30/20 Rule: A simpler variation where 50% of your income goes to needs, 30% to wants, and 20% directly into savings or business investments.

- Hybrid Stuffing: Leave your grocery and gas money in your checking account (since they are necessities), and only use physical cash stuffing for high-risk impulse categories like dining out and entertainment.

Best Practices & Optimization Tips

To squeeze the absolute maximum value out of this budgeting method, follow these advanced strategies:

- Zero-Based Budgeting: Combine cash stuffing with zero-based budgeting, where Income minus Expenses exactly equals zero. Every dollar must have a named job before the month begins.

- Use Denomination Breakdowns: Before going to the bank, calculate exactly how many $100s, $20s, $10s, and $5s you need. Hand this “teller slip” to the bank teller to save time and ensure your envelopes are perfectly balanced.

- Gamify the Process: Participate in “No Spend Challenges” for a weekend or a week. Take the money you would have spent and immediately stuff it into your side hustle funding envelope.

Common Mistakes to Avoid

- Forgetting Sinking Funds: Sinking funds are envelopes for large, predictable annual expenses (like car registration, Christmas, or yearly web hosting). If you don’t stuff a little cash for these each month, they will derail your entire budget when they hit.

- Keeping Zero Buffer in the Bank: Always leave a small buffer ($100-$200) in your checking account to prevent accidental overdraft fees from auto-pay bills.

- Giving Up After Month One: Month one of cash stuffing is always a disaster. You will inevitably budget incorrectly. Do not quit. Use the data from month one to create a hyper-accurate budget for month two.

Long-Term Sustainability & Growth

The ultimate goal of cash stuffing isn’t to live out of physical envelopes forever; it is to retrain your financial habits so you can focus on building sustainable wealth.

- Transitioning to Automation: Once you have mastered your spending habits and built up emergency funds, you can begin automating your finances. You can shift from physical cash back to digital tracking without the fear of impulse buying.

- Reinvestment Strategies: As your budget stabilizes, aggressively funnel your extra cash into income-producing assets. Buy index funds, start a YouTube channel, or invest in digital real estate.

- Future-Proofing: An organized budget ensures that when your online businesses do take off, your new influx of wealth won’t be squandered on lifestyle inflation.

Conclusion

Mastering cash stuffing is about far more than just organizing physical bills in a binder; it is a transformative financial strategy that reclaims your hard-earned money. By tracking your spending, enforcing strict limits, and plugging the leaks in your budget, you free up the crucial capital needed to fund your side hustles and build lasting financial freedom.

Ready to start your journey? Drop your questions in the comments below! Tell us which envelope category you struggle with the most, and be sure to subscribe for weekly strategies on budgeting and scaling your online income.

FAQs

How much money can I realistically save with cash stuffing?

Most beginners realistically save between $200 and $400 in their first month by eliminating impulse purchases. Over a year, this can equate to thousands of dollars in retained capital that can be used for investments.

Do I need prior budgeting experience to start cash stuffing?

Not at all. Cash stuffing is actually one of the best methods for beginners because it relies on simple math and the physical, tangible reality of holding cash, making it incredibly intuitive.

What is the initial investment required for this method?

The initial investment is incredibly low. You can purchase a high-quality A6 budgeting binder with zippered envelopes for around $10 to $30. Alternatively, you can start for free using standard paper envelopes.

How long until I see results in my finances?

You will notice an immediate psychological shift the first time you hand over physical cash. Tangible savings results usually become evident at the end of the first 30 to 60 days of consistent tracking.

Is cash stuffing safe to do in 2026?

Yes, but you must be smart about it. Never keep your entire life savings in cash. Cash stuffing should only be used for your monthly variable expenses (groceries, dining, gas), while your main savings remain secure in an FDIC-insured bank account.

Can I use cash stuffing to fund my work from home business?

Absolutely. By creating a dedicated “Business Fund” envelope, you can redirect the money you save from areas like entertainment or dining out directly into seed capital for your digital ventures.

Before you go, tap those stars!

Straightforward, no gimmicks, just solid banking advice

I clicked on this article expecting it to push some specific bank or financial product with referral links. I was pleasantly surprised. The advice was unbiased, focused on principles rather than promoting any particular institution, and gave me a clear framework to evaluate my own options. I appreciated that the article addressed the importance of FDIC insurance, automatic transfers, and goal-setting — things that seem obvious but that most people (including me) overlook. The writing was clear and concise, without the usual fluff or overly complex financial jargon. The only reason I’m giving four stars instead of five is that I would have liked even more detail on how to balance saving with paying down debt. Still, this was one of the most practical and trustworthy articles on saving I’ve read in a long time. Highly recommend.

Solid advice that cuts through the noise

I’ve been saving for years, but I kept wondering if my money was actually working as hard as it could be. There’s so much conflicting information out there — regular savings accounts, money market accounts, CDs, high-yield options — it gets confusing fast. This article did an excellent job comparing the options side by side, explaining the pros and cons of each, and helping me figure out which strategy made sense for my situation. I especially appreciated the section on the importance of emergency funds versus long-term savings, and the breakdown of how compound interest really adds up over time. I ended up moving my savings to a high-yield account and setting clearer goals. Practical, well-researched, and genuinely helpful.

Small changes, noticeable results

I’ll be honest — I clicked on this article expecting generic advice like “drive less” (thanks, captain obvious). But I was genuinely impressed. The article breaks down the actual science behind why certain habits affect fuel economy, with real numbers to back it up. I learned that my lead-foot acceleration and speeding were costing me way more than I realized. The section on vehicle maintenance was especially valuable — I didn’t know a dirty air filter could impact mileage that much. The tone was straightforward, no fluff, no upselling expensive products. Just solid, practical advice that actually works. My fuel expenses dropped by about 15% last month without me changing my overall driving needs.

Finally, practical advice that doesn’t require buying a new car

As someone who drives over 400 miles a week for work, gas expenses have been crushing my budget. I’ve read countless articles that basically just say “buy an electric vehicle” — which isn’t helpful when that’s not in my budget. This article was a game-changer. The tips were immediately actionable: combining trips, checking tire pressure (I didn’t realize how much that affects mileage!), and using gas price apps. I started implementing these suggestions last month, and I’ve already saved about $40. The writing was clear, well-organized, and respected that not everyone can just trade in their car. Highly recommend for anyone feeling the pain at the pump.

Perfect for renters who can’t install solar panels

As someone who rents an apartment, I often feel limited when it comes to making my home more energy-efficient. I can’t just install new appliances or add insulation to the walls. This article was a lifesaver because it focused on renter-friendly solutions—things like weatherstripping for doors, smart power strips, and optimizing how I use my existing appliances. The writing was straightforward and didn’t assume I owned a home. My only small critique is that I would have loved even more rent-specific examples, but overall, this was incredibly helpful. My electric bill dropped by about $15 last month!