Did you know that over 65% of aspiring online entrepreneurs fail to launch their side hustle simply because they lack initial seed capital—while simultaneously spending over $400 a month on takeout and inefficient grocery shopping? It is a fascinating blind spot in personal finance: people spend countless hours researching complex monetization strategies, yet they literally eat away the profit margins that could be funding their digital income dreams.

If you want to achieve true financial freedom and transition to a work from home lifestyle, mastering budget meals & cheap recipes is your mandatory first step. Your kitchen is essentially your first business headquarters. If you cannot manage the overhead costs of your daily food consumption, how will you manage the cash flow of a lucrative online business? By optimizing what you eat, you can rapidly free up hundreds of dollars a month—capital that can be directly invested into building powerful revenue streams.

In this comprehensive, data-driven guide, we will break down exactly how to slash your food expenses without sacrificing nutrition, and how to redirect those “kitchen savings” into a profitable online side hustle.

Quick Answer

Utilizing budget meals & cheap recipes involves basing your diet around low-cost, high-yield staple ingredients like rice, beans, and seasonal vegetables. By eliminating food waste and replacing expensive takeout with strategic batch cooking, you instantly create a monthly cash surplus that can be automatically redirected to fund online earnings and passive income investments.

What You’ll Need to Get Started

Before you can start redirecting your grocery savings into passive income streams, you need a highly efficient kitchen system. You do not need culinary school experience or expensive gadgets to execute this.

Here is the breakdown of what you need to successfully execute this food-to-wealth strategy:

- Meal Planning Tool: A free app like Mealime, or a simple Google Sheets template to map out your weekly menu and eliminate impulse buying. (Cost: Free)

- The “Side Hustle” Bank Account: A separate, free, high-yield savings account (HYSA) where the money you save on groceries will be deposited automatically. (Cost: Free)

- Pantry Staples: An initial stock of highly versatile, non-perishable bases (bulk rice, dried lentils, beans, pasta, and fundamental spices). (Estimated Cost: $25 – $40)

- Storage Containers: A set of durable glass or BPA-free plastic containers for batch cooking and meal prepping. (Estimated Cost: $15 – $25)

- Required Skills: Basic ability to follow instructions, boil water, and chop vegetables.

Time Investment

Optimizing your diet to act as an income generator requires a shift in your weekly routine. However, the time spent cooking is vastly outweighed by the financial return on that time.

- Setup Time Required: 2 to 3 hours on a Sunday. You will spend this time auditing your pantry, planning your meals, and doing your primary batch cooking for the week.

- Daily Time Commitment: 15 to 20 minutes a day to simply reheat your pre-made food or assemble simple ingredients.

- Timeline to First “Earnings”: Immediate. You will see your savings the very first time you skip the drive-thru or check out at the grocery store.

- Timeline to Side Hustle Capital: Most beginners free up $150 to $300 in their first 30 to 45 days.

- Comparison: If an hour of meal prep savings you $60 on takeout for the week, your “hourly rate” in the kitchen is $60/hour—far higher than many traditional part-time jobs.

Step-by-Step Implementation Guide

Follow these actionable steps to plug the financial leaks in your kitchen and boost your income potential.

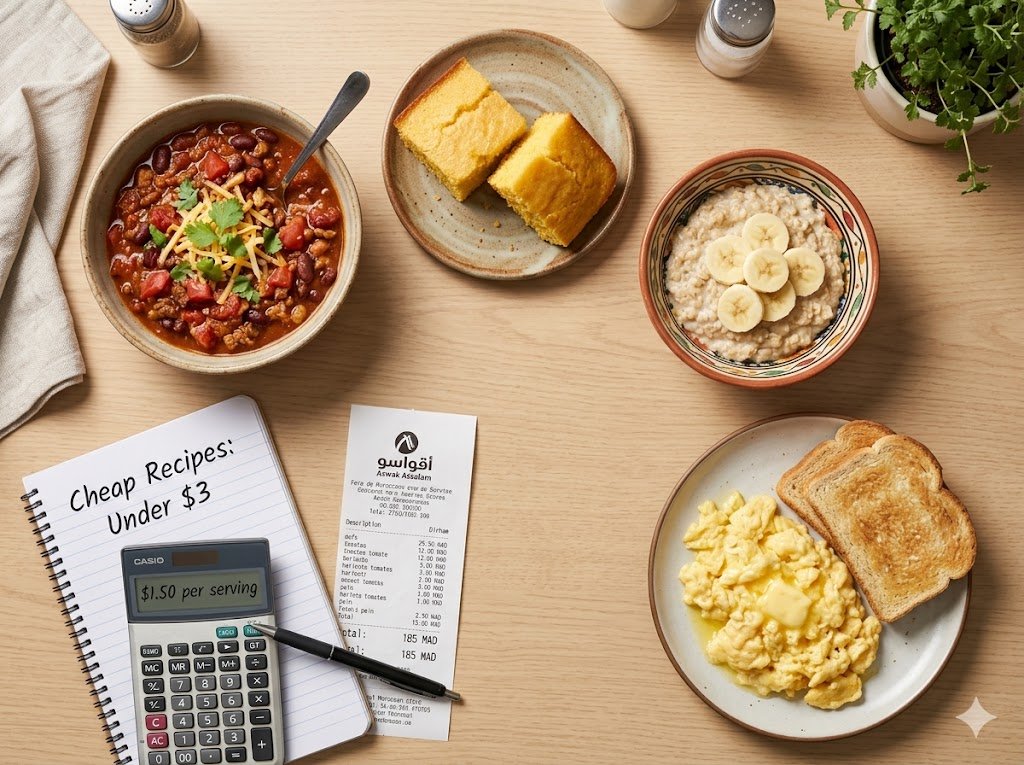

Step 1: The Pantry Audit & Menu Engineering

Never go to the store without knowing what you already own.

- Actionable Step: Pull everything out of your fridge and pantry. Design your budget meals & cheap recipes around the ingredients you already have. Need to use up a bag of potatoes and some ground beef? Search for a Shepherd’s Pie recipe.

- Pro Tip: Let local supermarket sales dictate your protein choices for the week, rather than choosing a recipe first and paying premium prices for out-of-season items.

Step 2: Master the “Base + Flavor + Protein” Formula

You don’t need 50 different recipes; you need one formula with endless variations.

- Actionable Step: Build every meal starting with a cheap base (rice, pasta, potatoes). Add a flavor profile (Mexican spices, Italian herbs, soy sauce). Finish with a low-cost protein (eggs, beans, canned tuna, or on-sale chicken).

- Insider Trick: Meat is the most expensive item in a grocery cart. By stretching your meals with beans or lentils, you instantly increase your household profit margins.

Step 3: Implement Batch Cooking for the Workweek

When you work from home or are busy building a side hustle, the temptation to order food delivery is highest when you are tired and hungry.

- Actionable Step: Cook large batches of soups, stews, or casseroles on Sunday. Portion them out into individual containers. When Wednesday night hits, your dinner is a two-minute microwave task.

Step 4: The “Profit Margin” Transfer

This is the most critical step for wealth building.

- Actionable Step: If your weekly food budget was previously $150, and your new budget meals cost you $70, you must immediately take that $80 difference and transfer it to your dedicated business fund. If you leave it in your checking account, you will accidentally spend it on lifestyle creep.

Income Potential & Earnings Breakdown

How does eating cheaper food translate to financial freedom? Capital saved is capital earned. Here is a realistic look at how optimizing your kitchen generates the seed money for your digital income:

| Savings Action | Estimated Monthly Savings | 1-Year Capital Generated | Digital Income Application |

|---|---|---|---|

| Replacing 3 Takeout Meals/Week | $180.00 | $2,160.00 | Covers domain hosting, premium themes, and software subscriptions. |

| Implementing “Meatless Mondays” | $40.00 | $480.00 | Funds targeted social media ads or freelance design assets. |

| Buying Bulk Staples (Rice/Beans) | $50.00 | $600.00 | Provides initial inventory capital for dropshipping or e-commerce. |

| Eliminating Weekly Food Waste | $45.00 | $540.00 | Pays for premium digital marketing or SEO courses. |

| Total Projected Capital | **$315.00** | $3,780.00 | A powerful launchpad for work-from-home ventures. |

Disclaimer: These figures are estimates based on average consumer data regarding takeout and food waste. Your specific savings will vary based on your location and prior spending habits.

Alternative Methods & Variations

If traditional meal prepping feels too restrictive, try these alternative strategies to lower your food costs and secure your side-hustle capital:

- The “Cook Once, Eat Twice” Method: Instead of dedicating an entire Sunday to batch cooking, simply double the recipe of whatever you are cooking for dinner. You immediately have lunch for the next day, preventing the $15 office lunch trap.

- Ugly Produce Subscriptions: Companies like Misfits Market or Imperfect Foods deliver organic produce with slight cosmetic blemishes at a 30-40% discount compared to grocery store prices.

- Bulk Buying Cooperatives: Splitting a membership to a warehouse club (like Costco) with a friend allows you to buy non-perishable staples at rock-bottom unit prices without requiring a massive pantry to store it all.

Best Practices & Optimization Tips

To squeeze maximum financial efficiency out of your kitchen and accelerate your journey toward passive income, keep these best practices in mind:

- Shop the Perimeter: The outer edges of the grocery store contain the essential, single-ingredient whole foods (produce, meat, dairy). The middle aisles are packed with highly processed, high-margin junk food that drains your wallet.

- Use Cashback Grocery Apps: Scan your receipts into apps like Ibotta, Fetch Rewards, or Checkout51. Route all cashback rewards directly to your digital business fund as an extra micro-revenue stream.

- Master the Freezer: Your freezer is a pause button for your money. If produce is about to go bad, chop it and freeze it for future soups or smoothies. Eliminate the “decay tax” of rotting food.

Common Mistakes to Avoid

Even highly motivated individuals fall into traps that derail their food savings. Watch out for these pitfalls:

- Frugal Fatigue (Cutting Too Deep): * The Mistake: Eating nothing but plain rice and beans for two weeks. You will get exhausted, rebel, and order $60 worth of pizza.

- The Prevention Strategy: Budget a small amount for sauces, spices, and occasional treats. Sustainability is better than extreme short-term deprivation.

- Ignoring Unit Pricing: * The Mistake: Buying a “sale” item that actually costs more per ounce than the generic brand sitting next to it.

- The Prevention Strategy: Always look at the small orange/yellow tag on the shelf that shows the “Price per Ounce” or “Price per 100g.”

- Failing to Redirect the Surplus:

- The Mistake: Saving $100 on groceries but accidentally absorbing that money into your entertainment budget.

- The Prevention Strategy: Treat your grocery savings as an immediate expense owed to your future self. Make the bank transfer the moment you return from the store.

Long-Term Sustainability & Growth

Optimizing your meals is an excellent financial sprint, but building lasting wealth requires a marathon mindset.

Reinvestment Strategies As your kitchen savings accumulate into a solid cash buffer, transition your focus. Do not spend the profits from your newly found capital on luxury items. Instead, reinvest those funds into assets: buy better tools for your freelance business, invest in dividend-paying index funds, or scale your online marketing efforts.

Future-Proofing Your Finances Food inflation will inevitably cause living costs to rise over time. To future-proof your finances, you must eventually shift from just saving money to making money. Use the discipline you learned by cooking budget meals to build diverse digital revenue streams that easily outpace inflation, ensuring your financial freedom remains intact regardless of the broader economy.

Conclusion

Mastering budget meals & cheap recipes is the secret weapon of successful digital entrepreneurs. By auditing your pantry, embracing batch cooking, and aggressively eliminating food waste, you manufacture your own seed capital in real time. Stop using the excuse that you don’t have the money to start a business; the cash you need to achieve your goals is waiting to be uncovered right on your dinner plate.

Ready to start your journey? Drop your favorite cheap recipe or biggest budgeting challenge in the comments below! Be sure to subscribe for weekly money-making strategies, share your progress in our community forums, and download our free side-hustle starter guide.

Frequently Asked Questions (FAQs)

How much money can I realistically make (or save) with these strategies?

By aggressively optimizing meal planning, avoiding convenience foods, and eliminating takeout, an average household can realistically free up $200 to $400 a month. If directed into a digital side hustle, the income potential of that saved capital becomes completely uncapped.

Do I need prior experience to start cooking budget meals?

No culinary experience is necessary. Utilizing basic, whole ingredients like rice, pasta, and frozen vegetables requires only foundational skills like boiling water and using a microwave or slow cooker. Free online tutorials can teach you the rest.

What is the initial investment required to start?

Zero dollars. Optimizing your food budget is entirely about modifying the cash flow you already spend on survival. Your only investment is the time it takes to plan your meals before heading to the store.

How long until I see results?

You will see immediate financial results at the checkout register on your very next shopping trip, and psychological results when you check your bank account at the end of the week. Measurable capital ready for your side hustle fund usually accumulates within 30 days.

Is this method still working in 2026 with high food inflation?

Yes. In fact, with food costs remaining high in 2026, utilizing budget meals and bulk ingredients is more crucial and effective than ever. As restaurant and convenience food prices rise, the savings gap between strategic home cooks and takeout consumers widens significantly.

What are the risks involved with this strategy?

There are virtually zero financial risks involved with optimizing your grocery budget. The only risk comes after you save the money—if you choose to invest your newly freed-up capital into high-risk, unverified online business ventures. Always research thoroughly before deploying your hard-earned savings.

Before you go, tap those stars!

Straightforward, no gimmicks, just solid banking advice

I clicked on this article expecting it to push some specific bank or financial product with referral links. I was pleasantly surprised. The advice was unbiased, focused on principles rather than promoting any particular institution, and gave me a clear framework to evaluate my own options. I appreciated that the article addressed the importance of FDIC insurance, automatic transfers, and goal-setting — things that seem obvious but that most people (including me) overlook. The writing was clear and concise, without the usual fluff or overly complex financial jargon. The only reason I’m giving four stars instead of five is that I would have liked even more detail on how to balance saving with paying down debt. Still, this was one of the most practical and trustworthy articles on saving I’ve read in a long time. Highly recommend.

Solid advice that cuts through the noise

I’ve been saving for years, but I kept wondering if my money was actually working as hard as it could be. There’s so much conflicting information out there — regular savings accounts, money market accounts, CDs, high-yield options — it gets confusing fast. This article did an excellent job comparing the options side by side, explaining the pros and cons of each, and helping me figure out which strategy made sense for my situation. I especially appreciated the section on the importance of emergency funds versus long-term savings, and the breakdown of how compound interest really adds up over time. I ended up moving my savings to a high-yield account and setting clearer goals. Practical, well-researched, and genuinely helpful.

Small changes, noticeable results

I’ll be honest — I clicked on this article expecting generic advice like “drive less” (thanks, captain obvious). But I was genuinely impressed. The article breaks down the actual science behind why certain habits affect fuel economy, with real numbers to back it up. I learned that my lead-foot acceleration and speeding were costing me way more than I realized. The section on vehicle maintenance was especially valuable — I didn’t know a dirty air filter could impact mileage that much. The tone was straightforward, no fluff, no upselling expensive products. Just solid, practical advice that actually works. My fuel expenses dropped by about 15% last month without me changing my overall driving needs.

Finally, practical advice that doesn’t require buying a new car

As someone who drives over 400 miles a week for work, gas expenses have been crushing my budget. I’ve read countless articles that basically just say “buy an electric vehicle” — which isn’t helpful when that’s not in my budget. This article was a game-changer. The tips were immediately actionable: combining trips, checking tire pressure (I didn’t realize how much that affects mileage!), and using gas price apps. I started implementing these suggestions last month, and I’ve already saved about $40. The writing was clear, well-organized, and respected that not everyone can just trade in their car. Highly recommend for anyone feeling the pain at the pump.

Perfect for renters who can’t install solar panels

As someone who rents an apartment, I often feel limited when it comes to making my home more energy-efficient. I can’t just install new appliances or add insulation to the walls. This article was a lifesaver because it focused on renter-friendly solutions—things like weatherstripping for doors, smart power strips, and optimizing how I use my existing appliances. The writing was straightforward and didn’t assume I owned a home. My only small critique is that I would have loved even more rent-specific examples, but overall, this was incredibly helpful. My electric bill dropped by about $15 last month!