Best Ways to Save Money and Earn Interest

Did you know that 67% of aspiring wealth-builders fail because they skip ONE crucial step: putting their idle cash to work? We all dream of unlocking massive income potential and achieving ultimate financial freedom, but leaving your money in a traditional checking account earning 0.01% is like taking a pay cut every year due to inflation.

If you are looking for the best ways to save money and earn interest, you are in exactly the right place. Earning interest is the ultimate form of passive income—it requires zero extra hours of labor once set up. Whether you are funneling cash from a new side hustle, optimizing your online earnings, or simply trying to maximize the profit margins of your household budget, learning how to monetize your savings is mandatory.

In this comprehensive guide, we will break down exactly how to protect your capital, outpace inflation, and turn your saved money into a powerful, automated wealth-generating machine.

What You’ll Need to Get Started

Before you can start multiplying your money, you need to set up the proper financial infrastructure. Unlike starting a complex business, the barrier to entry here is essentially zero.

- Required Tools: A secure high-yield savings account (HYSA), a reliable budgeting tool (like TrackThrift or a simple spreadsheet), and an internet connection.

- Initial Investment: $0 to $100. Most modern online banks allow you to open high-yield accounts with no minimum deposit.

- Skill Requirements: Basic financial literacy and a commitment to consistency. No Wall Street degree required!

- Beginner-Friendly Alternatives: If investing in the stock market feels too risky right now, FDIC-insured interest-bearing accounts are the perfect, risk-free starting point.

Time Investment

One of the most appealing aspects of earning interest is that it requires incredibly low active management compared to traditional work from home jobs.

- Setup Time Required: 1 to 2 hours. This includes researching banks, applying for an account online, and linking your primary checking account.

- Daily/Weekly Time Commitment: 10 minutes a month. You only need to verify your automatic transfers and check your monthly interest payouts.

- Timeline to First Earnings: Immediate. Most high-yield accounts calculate interest daily and pay it out monthly. You will see your first passive income deposit within 30 days.

- Realistic Expectations: “Most beginners see a tangible snowball effect in 60-90 days with consistent automated deposits.”

Step-by-Step Implementation Guide

Ready to take action? Here are the sequential steps to implement the best ways to save money and earn interest effectively.

1. Plug the Leaks in Your Budget

Before you can earn interest, you need capital. Audit your last 90 days of spending. Cancel unused subscriptions, negotiate your internet bill, and apply the 72-hour rule to impulse purchases. Treat your personal finances like a business to maximize your monthly profit margins.

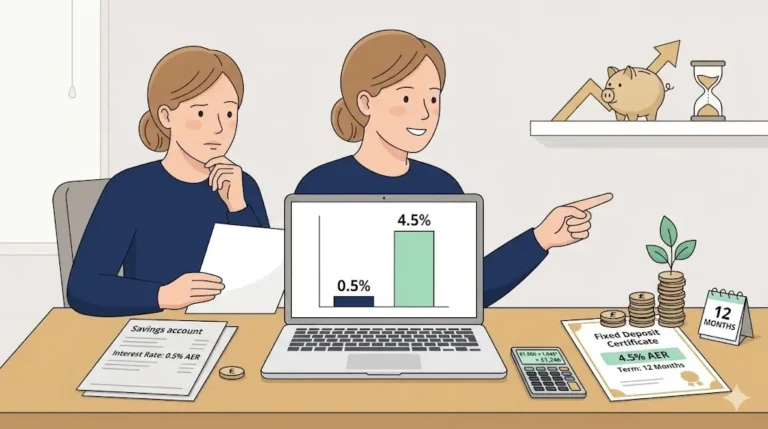

2. Open a High-Yield Savings Account (HYSA)

Traditional brick-and-mortar banks offer dismal interest rates. Open an account with an online-only bank (like Ally, Marcus by Goldman Sachs, or SoFi) that offers 4.00% to 5.00% APY. Because they lack physical branches, they pass the savings on to you in the form of higher yields.

3. Automate Your “Pay Yourself First” System

Log into your employer’s payroll portal or your checking account and set up a direct, recurring transfer to your new HYSA. Schedule this transfer for the exact day you get paid. If you never see the money in your checking account, you won’t spend it.

4. Build a CD Ladder for Guaranteed Returns

Once you have a fully-funded emergency reserve, look into Certificates of Deposit (CDs). A “CD Ladder” involves dividing your money into multiple CDs with varying maturity dates (e.g., 3-month, 6-month, 1-year). This locks in high-interest rates while keeping portions of your money liquid at regular intervals.

5. Reinvest All Earned Interest

The secret to explosive income potential is compound interest. Never withdraw the interest you earn. Leave it in the account so that next month, you earn interest on your original deposit plus the interest from the previous month.

Income Potential & Earnings Breakdown

How much can you actually make just by moving your money? Let’s look at a realistic breakdown based on a 4.5% APY, illustrating the power of this passive income stream:

- **Beginner Level ($5,000 Saved):** ~$225 annually / ~$18.75 monthly. It covers a couple of streaming subscriptions for doing absolutely nothing.

- **Intermediate Level ($20,000 Saved):** ~$900 annually / ~$75 monthly. You’ve now created a completely hands-off revenue stream that pays a utility bill.

- Advanced Wealth Building ($50,000+ Saved): $2,250+ annually / $187+ monthly.

- The Multiplier Effect: If you add digital income from a side hustle to your savings every month, your compounding timeline accelerates drastically.

Alternative Methods & Variations

If you have mastered the high-yield savings account and want to diversify your monetization strategies, consider these proven alternatives:

- Money Market Accounts (MMAs): Similar to HYSAs but often come with debit cards and check-writing privileges, offering higher liquidity for a slightly higher minimum balance.

- Treasury Bills (T-Bills): Backed by the US government, these are short-term investments (4 to 52 weeks) that are exempt from state and local taxes, making them a brilliant strategy for high-income earners.

- Dividend Yield Investing: A step up in risk. Investing in blue-chip index funds or dividend aristocrats allows you to earn quarterly cash payouts on top of potential stock market appreciation.

- Rewards Checking Accounts: Some credit unions offer up to 5% or 6% APY on checking balances up to a certain limit, provided you meet criteria like making 15 debit card transactions a month.

Best Practices & Optimization Tips

To truly maximize your online earnings through interest, follow these expert-level efficiency hacks:

- Rate Shop Quarterly: Interest rates fluctuate based on federal policies. Set a calendar reminder every three months to ensure your bank is still offering a highly competitive rate. If not, don’t be afraid to move your funds.

- Avoid Monthly Maintenance Fees: Never pay a bank to hold your money. Ensure your chosen HYSA has zero monthly fees and no minimum balance penalties.

- Combine with a Side Hustle: The fastest way to grow your interest payout is to increase your principal. Direct 100% of the profits from a freelance gig or work from home project directly into your HYSA.

Common Mistakes to Avoid

Even smart savers fall into these costly traps. Avoid these pitfalls to protect your revenue streams:

- Ignoring FDIC Insurance: Never chase a suspiciously high yield from an unverified financial institution or unregulated crypto platform. Ensure your bank is FDIC-insured (up to $250,000).

- Locking Up Your Emergency Fund: Do not put your 3-6 month emergency fund into a strict Certificate of Deposit. You need high liquidity for emergencies; use a standard HYSA instead.

- Chasing Promotional Rates Blindly: Some banks offer a massive 6% APY—but only for the first 3 months, dropping to 0.5% afterward. Always read the fine print on promotional offers.

Long-Term Sustainability & Growth

Earning interest on cash is just the defensive baseline of wealth building. To achieve true, long-term financial freedom, you must focus on sustainable growth and diversification.

As your cash reserves grow, inflation will eventually challenge your purchasing power. Therefore, your long-term strategy should involve reinvesting your interest into broader revenue streams. Once your cash savings are secure, begin automating investments into tax-advantaged retirement accounts (like a Roth IRA or 401k) or real estate. By diversifying across cash, equities, and physical assets, you effectively future-proof your finances against any economic climate.

Conclusion

Mastering the best ways to save money and earn interest is the undisputed foundation of financial independence. By optimizing your budget, selecting the right high-yield accounts, and leveraging the mathematical magic of compound interest, you can transform idle cash into a reliable, automated revenue stream.

Ready to start your journey to financial freedom? Drop your biggest savings question in the comments below! Subscribe for our weekly monetization strategies, share your progress in our community, and take control of your wealth today.

FAQs

How much money can I realistically make from interest?

Your earnings depend entirely on your principal balance and the current APY. For example, $10,000 saved in a 4.5% APY account will generate roughly $450 in passive income over a year without any additional effort.

Do I need prior investing experience to earn interest?

Absolutely not. Opening a high-yield savings account or a CD requires zero investing experience. It is as simple as opening a standard checking account.

What’s the initial investment required?

Many top-tier online banks require a $0 initial deposit and have no minimum balance requirements to start earning their highest interest rates.

How long until I see results and get paid?

Interest is typically calculated daily and deposited into your account once a month. You will see your first tangible results within 30 days of funding your account.

Are high-yield savings accounts safe?

Yes, as long as you choose a bank that is FDIC-insured (or NCUA-insured for credit unions). This guarantees your money is protected by the government up to $250,000 per depositor, per account ownership category.

What are the risks involved in earning interest this way?

With FDIC-insured HYSAs and CDs, the risk of losing your principal is virtually zero. The main “risk” is inflation risk—if the inflation rate is higher than your interest rate, your purchasing power may slowly decrease over time.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice. Always perform your own research and consult with a certified financial professional before making major financial decisions.