15 Realistic Ways to Save Money and Grow Your Savings

Did you know that over 65% of aspiring entrepreneurs struggle to launch their digital income streams simply because they lack the initial seed capital? In the rush to start a side hustle or build an online business, many people overlook the absolute highest-yield investment available to them: optimizing their own personal spending. Finding realistic ways to save money isn’t about extreme frugality or living in deprivation; it is about treating your household budget like a business and maximizing your personal profit margins.

By plugging the financial leaks in your daily life, you instantly free up cash that can be redirected toward investments, debt payoff, or funding your journey to true financial freedom.

Quick Answer

The most effective and realistic ways to save money involve auditing your recurring subscriptions, automating a “pay yourself first” transfer to a high-yield savings account, and optimizing your highest variable expenses like groceries and utilities. By treating your budget as a business profit margin, you can immediately free up hundreds of dollars a month to fund investments and passive income streams.

What You’ll Need to Get Started

Optimizing your expenses is the ultimate foundational work from home task. You don’t need a business loan, complex software, or specialized financial training to begin reclaiming your cash flow.

Required Tools & Resources:

- A Financial Dashboard: A free budgeting app (like TrackThrift, EveryDollar, or Mint) or a basic Google Sheets template.

- Your Last 90 Days of Data: Three months of bank and credit card statements to accurately assess your baseline spending.

- Cashback Tools: Free browser extensions like Rakuten or Honey, and mobile apps like Ibotta or Fetch Rewards.

- A High-Yield Savings Account (HYSA): An online bank account yielding 4-5% APY to store your newfound savings.

Initial Investment Breakdown:

- Estimated Cost: $0.00. The best tools for auditing your finances are completely free.

- Skill Requirements: Basic addition, subtraction, and the discipline to honestly face your spending habits.

Time Investment

Unlike building a blog, launching a YouTube channel, or developing digital income assets—which can take months or years to yield returns—optimizing your budget provides immediate, guaranteed results.

- Setup Time Required: 1 to 2 hours for an initial deep-dive audit of your accounts and subscriptions.

- Daily/Weekly Time Commitment: 15 to 30 minutes a week to categorize transactions, check progress, and adjust your budget.

- Timeline to First Results: Immediate. Most beginners see a tangible increase in their cash flow within 30 to 60 days just by eliminating “ghost” subscriptions and optimizing their grocery trips.

- Comparison: Earning an extra $300 a month through a new side hustle takes massive marketing effort. Saving $300 a month by auditing your expenses requires a fraction of the time and achieves the exact same positive impact on your net worth.

Step-by-Step Implementation Guide

To hit our target of 15 realistic ways to save money, we have broken the strategies down into 5 actionable, step-by-step implementation phases:

Step 1: Automate and Audit Your Baseline

- Automate the “Pay Yourself First” Transfer: On payday, automatically transfer 10-20% of your income straight to an HYSA. If you never see the money in your checking account, you won’t spend it.

- Audit and Cancel Ghost Subscriptions: Use your 90-day bank statements to identify streaming services, gym memberships, or software you no longer use. Cancel them immediately.

- Negotiate Fixed Bills: Call your car insurance provider, internet provider, and cell phone company. Threatening to switch to a competitor often unlocks hidden “retention department” discounts.

Step 2: Optimize Your Daily Consumption

- Implement the 24-Hour Rule: For any non-essential purchase over $50, force yourself to wait 24 hours. This eliminates the emotional impulse buy and protects your capital.

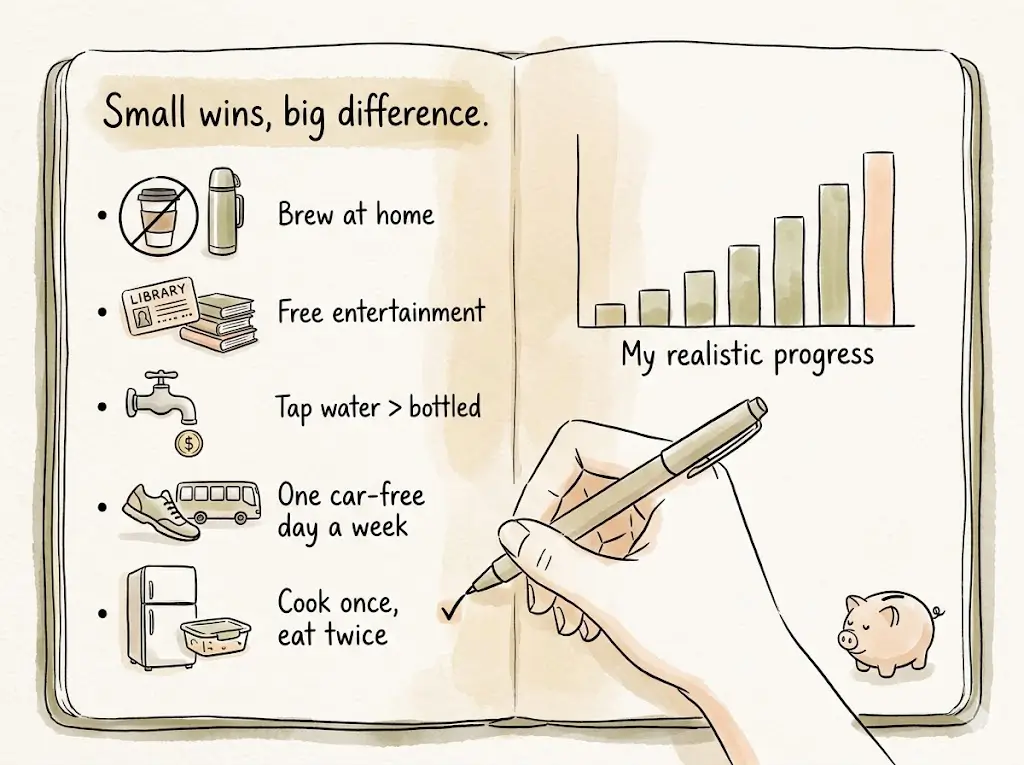

- Master Reverse Meal Planning: Plan your weekly meals strictly around what is already in your pantry and what is actively on sale in the local grocery circulars.

- Switch to Store Brands: Over 80% of generic store brands are made in the exact same factories as name-brand counterparts. Make the switch to instantly cut 20% off your grocery bill.

- Use Cashback Apps Religiously: Never make a purchase without routing it through a cashback portal (like Rakuten) or scanning your receipt (via Fetch Rewards).

Step 3: Hack Your Housing and Utility Costs

- Install a Smart Thermostat: Automate your home’s climate control to lower heating/cooling when you are asleep or away at work.

- Slay “Vampire” Energy Devices: Unplug appliances with digital clocks or standby lights (like microwaves and TVs) when not in use, or put them on smart power strips.

- DIY Basic Home Maintenance: Use YouTube tutorials to fix simple plumbing leaks, replace filters, or patch drywall instead of outsourcing to expensive contractors.

- Check Your Mortgage Rate: If interest rates have dropped, consult a free mortgage broker to see if remortgaging could save you hundreds of dollars a month.

Step 4: Re-evaluate Transportation

- Bundle Your Errands: Cold-starting your car for multiple short trips burns excess fuel. Bundle your grocery shopping, pharmacy runs, and other errands into one strategic weekly loop.

- Maintain Optimum Tire Pressure: Under-inflated tires decrease your gas mileage by up to 3%. Check them monthly to maximize fuel efficiency.

Step 5: Protect and Reinvest Your Profit Margins

- Build a Cash Buffer (Emergency Fund): Save a bare minimum of $1,000 to $3,000 immediately to prevent you from going into high-interest credit card debt when the car breaks down.

- Channel Savings into Investments: The ultimate savings hack is ensuring your saved money makes more money. Move your slashed expenses directly into dividend-paying index funds or seed capital for a business.

Income Potential & Earnings Breakdown

When you implement these strategies, the financial impact is identical to giving yourself a massive, tax-free raise. Here is a realistic look at how optimizing your spending translates into newfound capital:

| Expense Category | Monthly Savings Potential | Annual Capital Created | Best Reinvestment Use |

|---|---|---|---|

| Subscriptions & Bills | $40 – $80 | $480 – $960 | Web hosting / domain names for an online business |

| Grocery & Meal Optimization | $150 – $300 | $1,800 – $3,600 | Seed money for e-commerce inventory |

| Utilities & Home Hacking | $30 – $60 | $360 – $720 | High-Yield Savings Account for compound interest |

| Total Reclaimed Income | $220 – $440+ | **$2,640 – $5,280+** | Investing for long-term passive income |

Note: Individual results vary heavily based on your current baseline spending, family size, and local cost of living.

Alternative Methods & Variations

If tracking every single penny feels too overwhelming, try these alternative budgeting frameworks:

- The 50/30/20 Rule: A simpler, percentage-based approach where 50% of your income is strictly allocated to needs, 30% to wants, and 20% to savings/debt payoff.

- The Envelope System: A physical, cash-based system. At the start of the month, put your allocated grocery and entertainment budgets into paper envelopes. When the cash is gone, you stop spending.

- The “No-Spend” Challenge: A gamified variation where you challenge yourself to spend absolutely zero dollars on non-essentials (no dining out, no coffee shops, no clothes) for a strict 7-day or 30-day period to inject a massive amount of cash into your savings goals.

Best Practices & Optimization Tips

To truly maximize your savings rate and accelerate your path to digital income generation, adopt a CEO mindset regarding your personal finances:

- Track Your “Profit Margins”: Calculate your net worth on the 1st of every month. Just like a business tracks revenue streams, you must track your personal asset growth to stay motivated.

- Stack Your Rewards: Maximize online earnings by stacking deals. Buy a needed item through a cashback portal, pay with a 2% cashback credit card (if you pay it in full), and scan the final receipt for rewards points.

- Visualize the Time-Value of Money: Before making a $150 impulse purchase, divide that cost by your hourly wage. Ask yourself: “Is this item worth 6 hours of my life?”

Common Mistakes to Avoid

Even well-intentioned savers fall into traps that silently erode their wealth. Protect your progress by avoiding these common pitfalls:

- Frugal Fatigue: Cutting out every single joy in your life (like a $4 latte) while ignoring massive structural costs (like an overpriced car loan) leads to burnout. Focus on the big wins first.

- The “Spend to Save” Mentality: Buying a gadget you don’t actually need just because it is 40% off means you still lost 60% of your capital.

- Leaving Cash in “Dead” Accounts: Saving money is useless if inflation eats it. Never leave bulk savings in a standard checking account earning 0.01%. Always move idle cash to high-yield vehicles.

Long-Term Sustainability & Growth

Finding realistic ways to save money is only the first half of the wealth-building equation. True financial freedom is achieved through what you do with the surplus.

As your savings grow, beware of lifestyle creep. If you get a raise at work or clear a debt, do not increase your living expenses to match it. Maintain your optimized budget and funnel 100% of that new income into your investment portfolio.

Channel your reclaimed capital into creating true passive income. Whether you use your $5,000 in annual savings to buy dividend-paying stocks, fund a real estate syndication, or launch an affiliate marketing website, leverage your savings to build systems that will eventually replace your 9-to-5 income.

Conclusion

Securing your personal financial baseline is the absolute prerequisite to building sustainable wealth. By implementing these realistic ways to save money, you stop the quiet drain on your resources and systematically buy back your own capital. You aren’t just cutting coupons; you are generating the seed money necessary to fund your entrepreneurial dreams.

Ready to start your journey? Let us know which of these 15 strategies you are implementing today in the comments below! Don’t forget to subscribe for our weekly monetization strategies, and share your progress in our community forums!

FAQs

1. How much money can I realistically save in my first month?

Most households can easily find $100 to $300 in their first 30 days simply by canceling unused subscriptions, negotiating internet/insurance bills, and implementing strict meal planning.

2. Do I need financial experience to start budgeting?

2. Do I need financial experience to start budgeting? Not at all. You just need a clear understanding of your monthly take-home pay and a list of your recurring expenses. Free apps automate the hard math for you.

3. What’s the initial investment to optimize my finances?

Zero dollars. The tools you need—like budgeting spreadsheets, bank apps, and cashback extensions—are entirely free.

4. How long until I see results from these strategies?

You will see immediate cash flow improvements on your very next billing cycle. Within 60 to 90 days, you will notice a significant, tangible increase in your bank balances.

5. Are these money-saving methods still working in 2026?

Yes. In fact, with fluctuating economic conditions and rising costs, optimizing your budget, renegotiating bills, and utilizing cashback technology is more critical today than ever before.

6. What are the risks involved in extreme frugality?

The main risk is “frugal fatigue,” which leads to burnout and binge spending. It is vital to build a realistic budget that still allows for small, calculated joys so your financial plan remains sustainable long-term.

Before you go, tap those stars!

Straightforward, no gimmicks, just solid banking advice

I clicked on this article expecting it to push some specific bank or financial product with referral links. I was pleasantly surprised. The advice was unbiased, focused on principles rather than promoting any particular institution, and gave me a clear framework to evaluate my own options. I appreciated that the article addressed the importance of FDIC insurance, automatic transfers, and goal-setting — things that seem obvious but that most people (including me) overlook. The writing was clear and concise, without the usual fluff or overly complex financial jargon. The only reason I’m giving four stars instead of five is that I would have liked even more detail on how to balance saving with paying down debt. Still, this was one of the most practical and trustworthy articles on saving I’ve read in a long time. Highly recommend.

Solid advice that cuts through the noise

I’ve been saving for years, but I kept wondering if my money was actually working as hard as it could be. There’s so much conflicting information out there — regular savings accounts, money market accounts, CDs, high-yield options — it gets confusing fast. This article did an excellent job comparing the options side by side, explaining the pros and cons of each, and helping me figure out which strategy made sense for my situation. I especially appreciated the section on the importance of emergency funds versus long-term savings, and the breakdown of how compound interest really adds up over time. I ended up moving my savings to a high-yield account and setting clearer goals. Practical, well-researched, and genuinely helpful.

Small changes, noticeable results

I’ll be honest — I clicked on this article expecting generic advice like “drive less” (thanks, captain obvious). But I was genuinely impressed. The article breaks down the actual science behind why certain habits affect fuel economy, with real numbers to back it up. I learned that my lead-foot acceleration and speeding were costing me way more than I realized. The section on vehicle maintenance was especially valuable — I didn’t know a dirty air filter could impact mileage that much. The tone was straightforward, no fluff, no upselling expensive products. Just solid, practical advice that actually works. My fuel expenses dropped by about 15% last month without me changing my overall driving needs.

Finally, practical advice that doesn’t require buying a new car

As someone who drives over 400 miles a week for work, gas expenses have been crushing my budget. I’ve read countless articles that basically just say “buy an electric vehicle” — which isn’t helpful when that’s not in my budget. This article was a game-changer. The tips were immediately actionable: combining trips, checking tire pressure (I didn’t realize how much that affects mileage!), and using gas price apps. I started implementing these suggestions last month, and I’ve already saved about $40. The writing was clear, well-organized, and respected that not everyone can just trade in their car. Highly recommend for anyone feeling the pain at the pump.

Perfect for renters who can’t install solar panels

As someone who rents an apartment, I often feel limited when it comes to making my home more energy-efficient. I can’t just install new appliances or add insulation to the walls. This article was a lifesaver because it focused on renter-friendly solutions—things like weatherstripping for doors, smart power strips, and optimizing how I use my existing appliances. The writing was straightforward and didn’t assume I owned a home. My only small critique is that I would have loved even more rent-specific examples, but overall, this was incredibly helpful. My electric bill dropped by about $15 last month!