Low Income Money Saving Challenge: How to Start (And Fund Your Side Hustle)

Did you know that an estimated 78% of successful digital entrepreneurs started their first online business with less than $500 in seed capital? It is a massive misconception that you need a huge salary to achieve financial freedom. The reality is that the most profitable revenue streams are often built by individuals who mastered cash management when their margins were the tightest.

If you feel like you are living paycheck to paycheck and working from home feels like an impossible dream, you aren’t alone. The secret isn’t a magical windfall; it’s adopting a strategic low income money saving challenge. This isn’t about extreme deprivation—it is a calculated system designed to squeeze hidden capital out of your current budget. In this guide, we will show you exactly how to execute a low income money saving challenge to build the ultimate runway for your future side hustle and digital income.

What You’ll Need to Get Started

When your budget is tight, your starting tools must be absolutely free. Executing a successful low income money saving challenge relies on organization, not premium software. Here is what you need to build your foundation:

- A Micro-Tracking System: A free Google Sheets template or a notebook. When margins are thin, every single dollar must be tracked.

- Initial Investment: $0. (The entire goal is to extract capital without spending a dime on setup).

- A Dedicated “Side Hustle” Bank Account: A free, high-yield savings account (HYSA) with no minimum balance requirements (like Ally or SoFi).

- Skill Requirements: Beginner-friendly consistency and the emotional resilience to separate “needs” from “wants.”

- A Defined Monetization Goal: A clear target for your savings, such as “$150 to buy a domain name and web hosting.”

Time Investment

The beauty of a low income money saving challenge is that it requires a fraction of the time needed for traditional income methods, yet the ROI (Return on Investment) is instant.

- Setup Time Required: 1 to 2 hours to conduct an honest audit of your last 60 days of spending.

- Daily/Weekly Time Commitment: 5 minutes daily to log expenses, plus a 15-minute weekly review.

- Timeline to First Earnings (Savings): Most beginners see results in 30-45 days with consistent effort. You will “earn” money back the very first day you opt out of an unplanned expense.

- The Reality Check: While building online earnings takes months of upfront work, a saving challenge instantly increases your available cash flow without adding hours to your workday.

Step-by-Step Implementation Guide

1. Establish Your “Micro-Goal”

When dealing with a low income, aiming to save $500 a month is a recipe for burnout. You need a micro-goal that guarantees an early psychological win.

- Action: Set your initial savings target to something incredibly small, such as $5 to $10 a week.

- Execution: Treat this micro-goal as a mandatory tax you owe to your future business.

- Pro Tip: Write down exactly what this micro-fund will purchase (e.g., “This $10/week pays for my graphic design software”).

2. The 72-Hour “Freeze” Rule

Impulse spending is the enemy of tight profit margins. You must introduce extreme friction into your buying habits.

- Action: Institute a mandatory 72-hour waiting period for any non-essential purchase over $15.

- Execution: If you want to buy something, add it to a digital note on your phone with the date.

- Insider Trick: By the time the 72 hours pass, the emotional dopamine spike of “shopping” usually fades, allowing you to redirect that cash into your savings challenge.

3. Digitize the Envelope System

The classic cash-envelope system is great, but digital income requires digital habits.

- Action: Open two free checking accounts. One is for fixed bills (rent, utilities), and the other is for variable spending (groceries, gas).

- Execution: Transfer exactly what you need for fixed bills. Whatever is left in the variable account is your absolute limit for the week.

- Pro Tip: Turn off overdraft protection. If a purchase declines, the challenge is working by forcing you to stick to the budget.

4. Route “Found Money” Immediately

Windfalls are the secret accelerators of any low income money saving challenge.

- Action: Identify “found money”—tax refunds, a $20 birthday gift, cash back from grocery apps, or the $10 you saved by skipping a streaming subscription.

- Execution: Do not leave this money in your checking account. Transfer it immediately to your side hustle HYSA.

Income Potential & Earnings Breakdown

How does saving $20 a week lead to passive income? The magic happens when you transition your saved capital into income-producing assets. Here is a realistic breakdown of how micro-savings fund your future:

| Savings Challenge Level | Weekly Capital Retained | 6-Month Side Hustle Seed Fund | Recommended Business Reinvestment | Potential Monthly ROI |

|---|---|---|---|---|

| Beginner | $10 / week | $260 | Used laptop for freelance writing | $200 – $500 |

| Intermediate | $25 / week | $650 | Niche blog hosting & SEO tools | $500 – $1,000+ |

| Advanced | $50 / week | $1,300 | Print-on-Demand designs & ads | $1,000 – $2,500+ |

Disclaimer: Savings and income potential vary heavily based on execution, niche selection, and market conditions. These figures are realistic projections for dedicated beginners who reinvest their savings wisely.

Alternative Methods & Variations

If a standard percentage-based budget feels too rigid, try these niche-specific variations of the low income money saving challenge:

- The $1 Incremental Challenge: Week 1 you save $1. Week 2 you save $2. By week 52, you are saving $52. Over a year, this yields $1,378—more than enough to start a robust online business.

- The “No-Spend” Weekend: Commit to zero discretionary spending from Friday evening to Monday morning. Use the weekend strictly to research monetization strategies or consume free educational content.

- The Pantry Audit Challenge: For one week a month, commit to spending $0 on groceries, forcing yourself to creatively cook meals using only what is already in the back of your pantry. Redirect the grocery budget into savings.

Best Practices & Optimization Tips

To maximize the efficiency of your challenge and build your digital empire faster, utilize these advanced optimization techniques:

- Leverage Cash-Back Apps: Use free apps like Fetch Rewards, Ibotta, or Rakuten for essential purchases like groceries. Treat the cash back as “free money” to immediately inject into your challenge.

- Sell the Clutter: Boost your initial challenge numbers by selling items you no longer use on Facebook Marketplace or eBay. This simultaneously cleans your workspace and funds your business.

- Join Frugal Communities: The journey to financial freedom can be lonely. Join subreddits like r/povertyfinance or r/sidehustle. Community accountability drastically reduces failure rates.

Common Mistakes to Avoid

Even the most motivated individuals can fail if they fall into these psychological traps:

- Extreme Deprivation (Budget Burnout): Cutting your grocery budget so low that you compromise your health will lead to exhaustion. You cannot build a work from home career if you are burnt out. Prevention: Always allow a tiny, $5 guilt-free buffer.

- Comparing Chapter 1 to Chapter 20: Do not compare your $10/week savings challenge to an influencer’s $10,000/month passive income dashboard. Prevention: Focus strictly on your own profit margins.

- Keeping Cash Under the Mattress: Inflation will destroy your purchasing power. Prevention: Ensure your challenge funds are housed in an account that yields at least a 4-5% APY.

Long-Term Sustainability & Growth

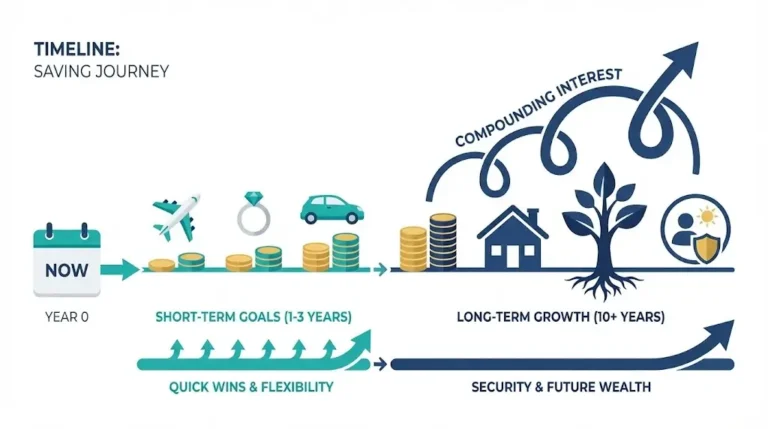

The ultimate goal of a low income money saving challenge isn’t to live in perpetual frugality; it is to create an escape velocity from low wages.

Once you have successfully saved your first $500, the “saving” phase transitions into the “scaling” phase. You will use that capital to buy a domain, launch a product, or run targeted ads. As your new digital income stream begins to generate revenue, the most critical step is reinvestment. Do not immediately inflate your lifestyle. Instead, apply the exact same discipline you learned during this challenge to manage your new business profit margins, guaranteeing long-term sustainability and true wealth.

Conclusion

Starting a low income money saving challenge is the ultimate foundational step toward unlocking your financial freedom. By establishing micro-goals, implementing the 72-hour freeze rule, and ruthlessly routing “found money” into a dedicated side hustle fund, you can generate startup capital on almost any budget. Remember, it is not about how much you make right now; it is about how effectively you protect and deploy the cash you have.

Ready to start your journey? Drop your commitment to your first weekly micro-goal in the comments below! Don’t forget to subscribe for weekly money-making strategies, and share your progress in our community!

FAQs

How much money can I realistically make (save) on a low income?

Even on a tight budget, most beginners can realistically save $10 to $25 a week by optimizing grocery lists, utilizing cash-back apps, and cutting hidden digital subscriptions. This equates to $500 to $1,300 a year in side hustle seed capital.

Do I need prior experience to start this challenge?

No prior financial experience is necessary. This challenge relies on basic math and beginner-friendly habits. The only requirement is a willingness to honestly evaluate your current spending.

What’s the initial investment?

Zero dollars. The entire premise of this challenge is to retain capital using free tools like digital spreadsheets or pen and paper.

How long until I see results?

You will see immediate results the very first week you choose to skip an impulse purchase. However, the psychological shift and compounding financial effects usually become highly visible within 30 to 60 days.

Is this method still working in 2026?

Absolutely. In an era of inflation and algorithmic marketing, returning to fundamental, disciplined cash management is the most reliable way to protect your personal wealth and fund new online ventures.

What are the risks involved?

The primary risk is “budget burnout” caused by setting unrealistic savings goals. To mitigate this risk, start with incredibly small micro-goals (like $5 a week) to build momentum rather than aiming for large, painful cuts.

Before you go, tap those stars!

Straightforward, no gimmicks, just solid banking advice

I clicked on this article expecting it to push some specific bank or financial product with referral links. I was pleasantly surprised. The advice was unbiased, focused on principles rather than promoting any particular institution, and gave me a clear framework to evaluate my own options. I appreciated that the article addressed the importance of FDIC insurance, automatic transfers, and goal-setting — things that seem obvious but that most people (including me) overlook. The writing was clear and concise, without the usual fluff or overly complex financial jargon. The only reason I’m giving four stars instead of five is that I would have liked even more detail on how to balance saving with paying down debt. Still, this was one of the most practical and trustworthy articles on saving I’ve read in a long time. Highly recommend.

Solid advice that cuts through the noise

I’ve been saving for years, but I kept wondering if my money was actually working as hard as it could be. There’s so much conflicting information out there — regular savings accounts, money market accounts, CDs, high-yield options — it gets confusing fast. This article did an excellent job comparing the options side by side, explaining the pros and cons of each, and helping me figure out which strategy made sense for my situation. I especially appreciated the section on the importance of emergency funds versus long-term savings, and the breakdown of how compound interest really adds up over time. I ended up moving my savings to a high-yield account and setting clearer goals. Practical, well-researched, and genuinely helpful.

Small changes, noticeable results

I’ll be honest — I clicked on this article expecting generic advice like “drive less” (thanks, captain obvious). But I was genuinely impressed. The article breaks down the actual science behind why certain habits affect fuel economy, with real numbers to back it up. I learned that my lead-foot acceleration and speeding were costing me way more than I realized. The section on vehicle maintenance was especially valuable — I didn’t know a dirty air filter could impact mileage that much. The tone was straightforward, no fluff, no upselling expensive products. Just solid, practical advice that actually works. My fuel expenses dropped by about 15% last month without me changing my overall driving needs.

Finally, practical advice that doesn’t require buying a new car

As someone who drives over 400 miles a week for work, gas expenses have been crushing my budget. I’ve read countless articles that basically just say “buy an electric vehicle” — which isn’t helpful when that’s not in my budget. This article was a game-changer. The tips were immediately actionable: combining trips, checking tire pressure (I didn’t realize how much that affects mileage!), and using gas price apps. I started implementing these suggestions last month, and I’ve already saved about $40. The writing was clear, well-organized, and respected that not everyone can just trade in their car. Highly recommend for anyone feeling the pain at the pump.

Perfect for renters who can’t install solar panels

As someone who rents an apartment, I often feel limited when it comes to making my home more energy-efficient. I can’t just install new appliances or add insulation to the walls. This article was a lifesaver because it focused on renter-friendly solutions—things like weatherstripping for doors, smart power strips, and optimizing how I use my existing appliances. The writing was straightforward and didn’t assume I owned a home. My only small critique is that I would have loved even more rent-specific examples, but overall, this was incredibly helpful. My electric bill dropped by about $15 last month!