Digital vs Paper Budgeting: Pros and Cons

Did you know that 67% of online entrepreneurs fail because they skip this ONE crucial step? While they focus intensely on monetization strategies, they often lose track of the very capital required to keep their business afloat. In the world of online earnings, your choice of tracking method is the difference between a thriving revenue stream and a bankrupt venture.

Whether you are managing a work from home business or scaling a small side hustle, the debate between digital vs paper budgeting is more than just a matter of preference—it’s about psychological connection and technical efficiency. Does the tactile nature of a pen-and-paper ledger help you curb impulse spending, or does the automation of a digital app unlock the time you need to focus on digital income growth? In this guide, we will dive deep into the pros and cons of both methods to help you maximize your profit margins and achieve lasting financial freedom.

What You’ll Need to Get Started

To decide between digital vs paper budgeting, you need to understand the tools required for each ecosystem. Here is your starter kit:

For Digital Budgeting:

- Budgeting Apps: YNAB (You Need A Budget), Monarch Money, or EveryDollar.

- Spreadsheets: Custom Google Sheets or Excel templates (often free).

- Automation Tools: Bank syncing features or Zapier integrations to track online earnings in real-time.

- Cost: Free (Google Sheets) to $15/month (Premium apps).

For Paper Budgeting:

- Ledgers & Planners: A dedicated financial planner or a simple bullet journal.

- Writing Tools: Multi-colored pens for categorizing fixed vs. variable costs.

- Cash Envelopes: For those using the “envelope method” alongside paper tracking.

- Cost: $5 (basic notebook) to $35 (high-end planners).

Skill Requirements:

- Digital: Basic tech literacy and comfort with cloud-based security.

- Paper: Discipline for manual entry and basic arithmetic.

Time Investment

How you manage your time is just as important as how you manage your money, especially when building income potential.

- Setup Time Required: * Digital: 1–2 hours to link accounts and categorize past transactions.

- Paper: 2–3 hours to design your layout and manually audit previous bank statements.

- Daily/Weekly Commitment: * Digital: 5–10 minutes a week (thanks to automation).

- Paper: 15–20 minutes every few days to log physical receipts.

- Timeline to Results: Most beginners see a significant shift in their spending awareness within 60 to 90 days with consistent effort.

- The Comparison: Digital is “set and forget” (best for busy entrepreneurs), while paper is “slow and intentional” (best for those prone to overspending).

Step-by-Step Implementation Guide

Step 1: Conduct a 30-Day Financial Audit

Before choosing your medium, you must see where your money is currently going. Look at your last month of side hustle expenses and personal bills.

- Action: Highlight your “leaks.” If you have many small digital transactions, a digital app might be easier to track them all.

Step 2: Choose Your Primary Medium

Decide if you value speed (Digital) or psychological connection (Paper).

- Pro Tip: Many successful practitioners use a “Hybrid Method”—digital for tracking digital income and paper for tracking daily “fun money” spending.

Step 3: Define Your Revenue and Expense Buckets

Create specific categories for your monetization strategies.

- Categories: Housing, Utilities, Side Hustle Reinvestment, and Tax Reserves.

Step 4: Set a Weekly “Money Date”

Whether you use an iPad or a notebook, you must reconcile your numbers.

- Digital: Check for miscategorized transactions.

- Paper: Calculate your totals for the week.

Step 5: Redirect the Surplus

The goal of digital vs paper budgeting is to find “extra” money.

- Action: The moment you find a surplus, move it into a high-yield account or reinvest it into your online earnings tools.

Income Potential & Earnings Breakdown

Budgeting isn’t just about saving; it’s about creating the capital necessary to scale revenue streams. A well-managed budget acts as a 0% interest loan to your business.

| Budgeting Metric | Impact on Profit Margin | Annual Capital Reclaimed | 5-Year Growth (at 7%) |

|---|---|---|---|

| Basic Tracking | +5% | $1,200 | $7,175 |

| Optimized Automation | +12% | $3,500 | $20,930 |

| Aggressive Management | +20%+ | $7,000+ | $41,860+ |

Case Study: A freelance designer switched to digital budgeting to track their digital income more accurately. By identifying $300/month in unused “ghost” subscriptions, they redirected that capital into Facebook Ads, eventually scaling their side hustle into a full-time work from home career.

Alternative Methods & Variations

If the binary choice of digital vs paper budgeting doesn’t fit, consider these variations:

- The Spreadsheet Hybrid: Uses the power of digital math but requires the manual entry of paper. Great for income potential awareness.

- Zero-Based Budgeting: Giving every dollar a job before the month starts (works on both paper and digital).

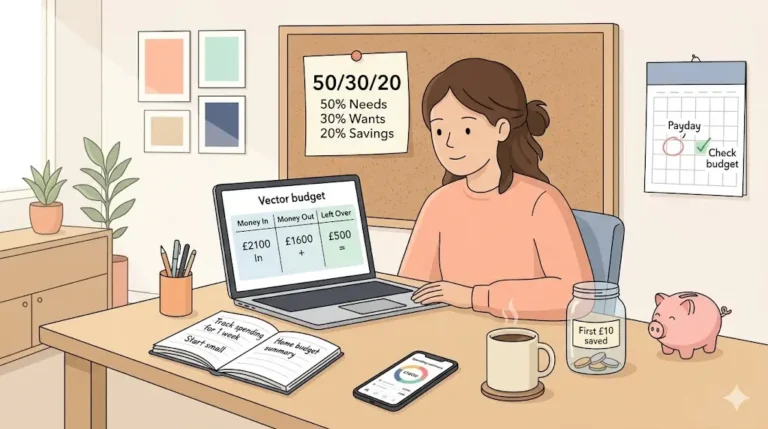

- The 50/30/20 Digital Method: Using an app to ensure 50% goes to needs, 30% to wants, and 20% to financial freedom goals.

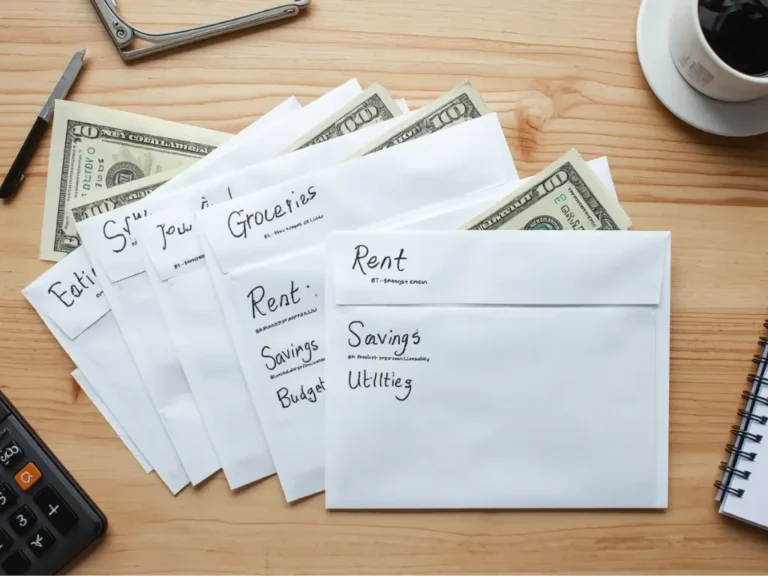

- Cash Envelope Paper System: Forcing a “hard stop” on variable spending by using physical cash.

Best Practices & Optimization Tips

- Sync with Reality: If you use digital, ensure your bank feeds are actually syncing. Don’t let a “connection error” derail your profit margins.

- Visual Aids: If using paper, use charts or “debt thermometers” to visualize your progress toward financial freedom.

- Audit Your Tech: Regularly review the software you use for your side hustle. If a digital budget shows you aren’t using a tool, cut it immediately.

- Community Recommendations: Join groups like r/personalfinance or digital nomad forums to see which templates are currently helping others grow their monetization strategies.

Common Mistakes to Avoid

- The “Notification Fatigue” (Digital): Ignoring app alerts until you’ve already overspent.

- The “Manual Error” (Paper): Math mistakes can lead to a false sense of security. Prevention: Always double-check your ledger with a calculator.

- Losing the Data: If your paper budget isn’t backed up (e.g., a photo), a lost notebook means lost history. Statistic: 12% of paper budgeters quit after losing their physical records.

- Over-complicating: Having 50 categories makes any method unsustainable. Keep it to 10–12 high-level buckets.

Long-Term Sustainability & Growth

The goal of your tracking system is to eventually outgrow the need for daily monitoring.

- Automation Opportunities: As your online earnings grow, move toward more automated digital systems so you can spend your time on high-level monetization strategies.

- Reinvestment: Use the “found money” from your budget to diversify your revenue streams (e.g., dividend stocks or niche affiliate sites).

- Future-Proofing: Review your budgeting method every 6 months. What worked for a small side hustle might not work for a scaling digital income empire.

Conclusion

In the debate of digital vs paper budgeting, the winner is whichever method you will actually stick to. Digital offers the speed and automation required for a scaling work from home business, while paper offers the tactile awareness needed to fix deep-seated spending habits. By mastering your cash flow, you protect your profit margins and ensure you always have the capital to fund your next big side hustle.

Ready to start your journey? Drop your questions in the comments! Subscribe for weekly money-making strategies and share your progress in our community. Download our free starter guide to begin tracking your way to financial freedom today.

FAQs

How much money can I realistically make by budgeting?

Most people identify $200–$500 in monthly waste. If reinvested into a side hustle at a 7% return, this can grow into a $40,000+ asset over five years.

Do I need prior experience?

No. Digital apps are designed for beginners, and paper ledgers only require basic math. The most important skill is consistency.

What’s the initial investment?

You can start for $0 using Google Sheets or a notebook you already own. Premium apps or planners usually cost between $10 and $35.

How long until I see results?

You will see “found money” in your first 30-day audit. The long-term stability needed for financial freedom usually takes 60 to 90 days to solidify.

Is this method still working in 2026?

Absolutely. In an era of high inflation and “subscription creep,” choosing between digital vs paper budgeting is more vital for your profit margins than ever before.

What are the risks involved?

The main risk is “budget burnout”—becoming so obsessed with the numbers that you stop enjoying your life. Balance is key to long-term sustainability.