8 Proven Strategies and the Best Way to Save Money Today

Did you know that according to recent financial surveys, nearly 78% of workers in developed nations are living paycheck to paycheck, regardless of their income bracket? Most people believe that the secret to wealth is simply making more money through a side hustle or passive income, but the reality is much simpler. The “leaks” in your current budget are often larger than the new revenue streams you are trying to build. If you aren’t managing what you already have, you’ll never reach true financial freedom.

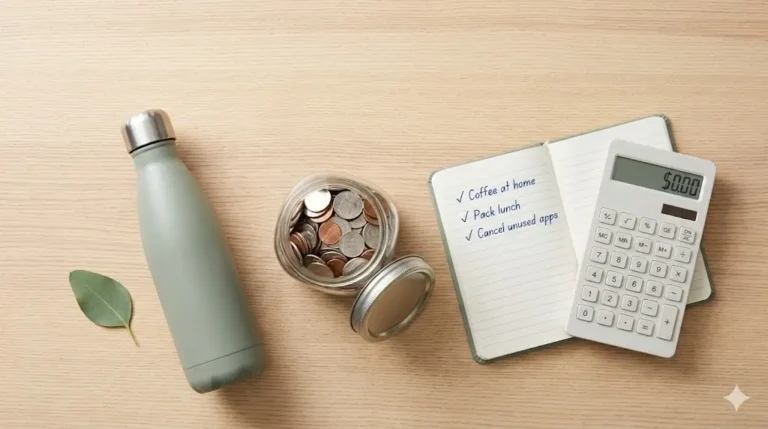

Quick Answer

The best way to save money today is a combination of automated micro-saving and a zero-based budget audit. By automating your transfers to a high-yield savings account and using an interactive tracking tool to identify “ghost” expenses, the average person can recover $300 to $600 in monthly capital without changing their primary lifestyle.

The High Cost of Invisible Spending

In the digital age, our money has become invisible. Between “one-click” purchases and automatic subscription renewals, capital flows out of our accounts before we can even process the transaction. While many focus on monetization strategies to increase their digital income, they often ignore the most efficient way to grow their net worth: optimization.

Finding the best way to save money today isn’t about deprivation; it’s about intentionality. Whether you are looking to fund a new work from home business or simply want to escape the cycle of debt, the strategies outlined below will help you maximize your profit margins on your own life.

2. What You’ll Need to Get Started

Before implementing these strategies, you need a basic financial “infrastructure.” You don’t need a professional accountant, but you do need the right tools:

- A High-Yield Savings Account (HYSA): Traditional savings accounts pay 0.01% interest. A modern HYSA can pay upwards of 4.5%, effectively giving you free passive income on your stashed cash.

- A Budgeting App or Spreadsheet: Use tools like YNAB or our interactive calculator below to visualize your cash flow.

- Automatic Transfer Capabilities: Most banking apps allow you to “Pay Yourself First” through recurring transfers.

- Skill Requirements: Basic math and the willingness to be honest with yourself about your spending habits.

- Estimated Costs: $0 (using free tools and existing accounts).

3. Time Investment: What to Expect

Managing your money effectively is a habit, not a one-time event. Here is the realistic breakdown of the time required:

- Initial Setup: 2 hours. This includes auditing your bank statements and setting up your automated systems.

- Weekly Check-in: 15 minutes. Review your transactions to ensure you are staying within your categories.

- Timeline to Results: You will see an immediate “liquidity boost” within 30 days. Most users report a significant change in their income potential after 90 days of consistent tracking.

- Comparison: Unlike a traditional job where you trade time for money, saving money is a “high-leverage” activity. A 2-hour audit can save you $2,400 a year—that’s a “wage” of $1,200/hour for your effort.

4. 8 Proven Strategies to Save Money

Step 1: Automate the “First 10%”

The best way to save money today is to remove the human element. Set your bank to move 10% of your paycheck to savings the moment it hits your account. If you never see the money, you won’t miss it.

Step 2: Kill the “Ghost” Subscriptions

Audit your digital apps. The average American spends over $200 a month on subscriptions, many of which are unused. Canceling these is an instant boost to your profit margins.

Step 3: Implement the “72-Hour Rule”

For any non-essential purchase over $30, wait 72 hours. Usually, the dopamine hit of “the hunt” fades, and you realize you don’t actually need the item.

Step 4: Master Strategic Grocery Shopping

Grocery costs have inflated significantly. Using store apps for digital coupons and sticking strictly to a list can save a family of four over $150 a month.

Step 5: Optimize Your Utility Bills

Call your internet and phone providers. Mention you are considering a switch to a competitor. More often than not, they will apply a “retention discount” that lasts for 12 months.

Step 6: Use “Cash Back” Portals

If you must shop online, use portals like Rakuten or Honey. This is a form of digital income that adds up over time.

Step 7: Downsize Your Transport Costs

Between insurance, gas, and maintenance, cars are one of the biggest wealth-killers. Explore how to save money on transportation to see if carpooling or public transit could save you thousands.

Step 8: Reduce Energy Consumption at Home

Small changes like smart thermostats and LED bulbs significantly impact your monthly overhead. Learn more in our guide on how to save money at home.

5. Interactive: Calculate Your Potential Savings

Are you curious how much these “small” changes actually add up to? Use the calculator below to see your personalized results based on your current income and spending habits.

[Insert Interactive Savings Calculator Shortcode Here] (Note: Use the “Savings Potential Calculator” HTML code provided in the previous step)

6. Income Potential & Recovered Capital

Many people ask, “How much can I realistically save?” Let’s look at the data ranges:

- Beginner: Saving $2,400/year. This is achieved by simply cutting two unused subscriptions and bringing lunch to work 3 days a week.

- Intermediate: Saving $6,000/year. This involves bill negotiation, switching to a generic grocery brand, and automating 10% of income.

- Advanced: Saving $12,000+/year. This is where you begin to see financial freedom. By optimizing housing or transport and investing the difference, your “saved money” begins generating its own passive income.

7. Alternative Methods & Scaling Strategies

If you have already optimized your spending, the next step is to increase the gap between income and expenses by scaling your revenue streams.

- The Side Hustle Stack: Combine your savings with a low-cost side hustle.

- Monetization of Skills: Turn your hobbies into digital income through freelancing or content creation.

- Frugal Living: For those who want to reach retirement early, the frugal living guide offers deep-cut strategies for extreme savings.

8. Common Mistakes to Avoid

- The “Coupon Fallacy”: Buying something you don’t need just because it’s on sale. A $100 item on sale for $70 isn’t “saving $30″—it’s spending $70.

- Frugal Fatigue: Cutting too much at once leads to a “spending binge” later. Focus on sustainable changes.

- Ignoring the Big Wins: People often spend hours trying to save $0.50 on eggs but ignore the $200 they could save by refinancing a loan. Focus on the best way to save money fast first.

9. Long-Term Sustainability & Growth

Saving money is the fuel for your investment engine. To maintain this long-term:

- Reinvest the Difference: Don’t let your saved money sit idle. Learn about saving money vs. investing to make your capital work for you.

- Audit Quarterly: Subscriptions and habits creep back in. Every three months, re-run your numbers.

- Future-Proof: Build an emergency fund of 3–6 months to ensure that a car breakdown or medical bill doesn’t wipe out your progress.

10. Conclusion

The best way to save money today isn’t found in a single “hack,” but in the cumulative power of small, automated decisions. By following these 8 strategies, you are doing more than just cutting costs—you are building the foundation for a lifetime of financial freedom. Whether you want to stop wasting money or start your first online earnings journey, the first step is always the same: take control of your cash flow.

Ready to start? Use our calculator above and share your potential savings in the comments below!

11. FAQs

Q: How much money can I realistically make by saving?

A: While it isn’t “earnings” in the traditional sense, the capital you recover is tax-free. Saving $500 a month is equivalent to earning an extra $700 before taxes at a traditional job.

Q: Do I need prior experience in finance?

A: No. Start with budgeting for beginners and use the automated tools recommended in this post.

Q: Is it still possible to save money with high inflation?

A: Yes. In fact, it is more necessary. Focusing on generic brands and reducing energy consumption are the best ways to save money today specifically because of inflation.

Q: What are the risks involved?

A: The main risk is “underspending” on essentials (like health or car maintenance), which leads to higher costs later. Always prioritize “Needs” over “Wants.”

Q: How long until I see results?

A: You will see an increase in your bank balance by the end of your first full billing cycle (30 days).

Before you go, tap those stars!

Straightforward, no gimmicks, just solid banking advice

I clicked on this article expecting it to push some specific bank or financial product with referral links. I was pleasantly surprised. The advice was unbiased, focused on principles rather than promoting any particular institution, and gave me a clear framework to evaluate my own options. I appreciated that the article addressed the importance of FDIC insurance, automatic transfers, and goal-setting — things that seem obvious but that most people (including me) overlook. The writing was clear and concise, without the usual fluff or overly complex financial jargon. The only reason I’m giving four stars instead of five is that I would have liked even more detail on how to balance saving with paying down debt. Still, this was one of the most practical and trustworthy articles on saving I’ve read in a long time. Highly recommend.

Solid advice that cuts through the noise

I’ve been saving for years, but I kept wondering if my money was actually working as hard as it could be. There’s so much conflicting information out there — regular savings accounts, money market accounts, CDs, high-yield options — it gets confusing fast. This article did an excellent job comparing the options side by side, explaining the pros and cons of each, and helping me figure out which strategy made sense for my situation. I especially appreciated the section on the importance of emergency funds versus long-term savings, and the breakdown of how compound interest really adds up over time. I ended up moving my savings to a high-yield account and setting clearer goals. Practical, well-researched, and genuinely helpful.

Small changes, noticeable results

I’ll be honest — I clicked on this article expecting generic advice like “drive less” (thanks, captain obvious). But I was genuinely impressed. The article breaks down the actual science behind why certain habits affect fuel economy, with real numbers to back it up. I learned that my lead-foot acceleration and speeding were costing me way more than I realized. The section on vehicle maintenance was especially valuable — I didn’t know a dirty air filter could impact mileage that much. The tone was straightforward, no fluff, no upselling expensive products. Just solid, practical advice that actually works. My fuel expenses dropped by about 15% last month without me changing my overall driving needs.

Finally, practical advice that doesn’t require buying a new car

As someone who drives over 400 miles a week for work, gas expenses have been crushing my budget. I’ve read countless articles that basically just say “buy an electric vehicle” — which isn’t helpful when that’s not in my budget. This article was a game-changer. The tips were immediately actionable: combining trips, checking tire pressure (I didn’t realize how much that affects mileage!), and using gas price apps. I started implementing these suggestions last month, and I’ve already saved about $40. The writing was clear, well-organized, and respected that not everyone can just trade in their car. Highly recommend for anyone feeling the pain at the pump.

Perfect for renters who can’t install solar panels

As someone who rents an apartment, I often feel limited when it comes to making my home more energy-efficient. I can’t just install new appliances or add insulation to the walls. This article was a lifesaver because it focused on renter-friendly solutions—things like weatherstripping for doors, smart power strips, and optimizing how I use my existing appliances. The writing was straightforward and didn’t assume I owned a home. My only small critique is that I would have loved even more rent-specific examples, but overall, this was incredibly helpful. My electric bill dropped by about $15 last month!