13 Transformative Money Saving Hacks for Everyday Expenses

Did you know that 67% of aspiring online entrepreneurs fail simply because they lack the initial capital to sustain their business? Most people believe they need to make dramatically more money to achieve financial freedom, but they skip the ONE crucial foundational step: optimizing what they already have.

Mastering practical money saving hacks is the undisputed secret to unlocking your financial potential. Whether your goal is to fund a new side hustle, build lasting passive income, or simply stop living paycheck to paycheck, retaining more of your current earnings is where the journey begins.

In this comprehensive guide, we are going to dive deep into data-driven, highly effective money saving hacks for everyday expenses. By treating your personal finances like a business, you’ll learn how to widen your personal profit margins and redirect that cash into lucrative revenue streams.

What You’ll Need to Get Started

Before diving into the specific hacks, you need the right foundation. Treating your savings strategy like a path to online earnings requires a few basic tools and a solid mindset.

- A Reliable Budgeting Tool: * Free Alternative: Google Sheets or Excel (highly customizable).

- Premium Option: YNAB (You Need A Budget) or EveryDollar (approx. $10-$15/month).

- Expense Tracking Apps: Mint, PocketGuard, or your native banking app to monitor cash flow.

- Cash-Back Extensions: Browser plugins like Rakuten or Honey (Free to install).

- Initial Investment: $0. The beauty of saving money is that it requires zero upfront financial capital—only a commitment of your time.

- Skill Requirements: Basic math, consistency, and a willingness to break old spending habits. Beginner-friendly templates can automate 90% of the heavy lifting.

Time Investment

Unlike building complex digital income platforms, implementing these money saving hacks yields almost immediate ROI (Return on Investment).

- Setup Time Required: 2 to 3 hours initially to review your past 90 days of bank statements, audit subscriptions, and set up your tracking system.

- Daily/Weekly Time Commitment: 10 to 15 minutes a week for a “budget check-in” to categorize expenses.

- Timeline to First Savings: Immediate. Most beginners see a tangible increase in their bank account retention within the first 30 days.

- Realistic Data: Most individuals applying these methods consistently free up $200 to $500 monthly within 60 to 90 days. Compared to traditional income methods (asking for a raise or taking a second job), this is the fastest way to increase your usable cash.

Step-by-Step Implementation Guide

Ready to increase your income potential by stopping the leaks in your wallet? Here are 13 actionable money saving hacks.

1. Automate Your Savings (Pay Yourself First)

Set up an automatic transfer from your checking to a high-yield savings account the exact day your paycheck hits. If the money isn’t in your main account, you won’t spend it.

- Pro Tip: Start with just 5% of your income. Once you adjust to that baseline, increase it to 10%.

2. Implement the 24-Hour Rule for Purchases

Impulse buying is the enemy of financial freedom. For any non-essential purchase over $50, force yourself to wait 24 hours before checking out.

- Insider Trick: Leave items in your online shopping cart. Often, retailers will email you a 10-15% discount code to complete the purchase the next day!

3. Audit and Cancel Unused Subscriptions

Subscription fatigue is real. Streaming services, gym memberships, and software apps drain your accounts silently.

- Action Step: Print your last two bank statements. Highlight every recurring charge. Cancel anything you haven’t used in 30 days. Use apps like Rocket Money to automate this process.

4. Embrace Meal Planning and Batch Cooking

Food is arguably the most controllable everyday expense. Eating out daily destroys your budget.

- Pro Tip: Dedicate Sundays to cooking large batches of proteins and grains. Portion them out for work from home lunches or office meals to save an average of $15 a day.

5. Negotiate Your Bills Annually

Your internet, cell phone, and car insurance providers expect you to quietly accept yearly price hikes.

- Action Step: Call your providers once a year and ask for the “retention department.” Mention that you are shopping around with competitors. They frequently offer unadvertised loyalty discounts.

6. Utilize Cash-Back Apps and Browser Extensions

Never buy anything online without passing through a cash-back portal.

- Insider Trick: Stack your savings. Use a rewards credit card, click through a portal like Rakuten, and apply a coupon code via Honey.

7. Switch to Generic Brands for Pantry Staples

Brand loyalty costs you a premium. For single-ingredient items (flour, sugar, spices, cleaning supplies), the generic store brand is often manufactured in the exact same facility as the name brand.

- Pro Tip: Test generic brands one at a time. If you don’t notice a drop in quality, make the switch permanent.

8. Optimize Energy Consumption at Home

Lowering your utility bills adds up significantly over a year.

- Action Step: Switch to LED bulbs, use smart plugs to kill “vampire” energy drain from electronics, and adjust your thermostat by just 2 degrees.

9. Maximize Credit Card Rewards (Responsibly)

If you pay off your balance in full every month, put all everyday expenses on a cash-back or travel rewards card.

- Warning: This hack only works if you never carry a balance. Credit card interest will instantly negate any rewards you earn.

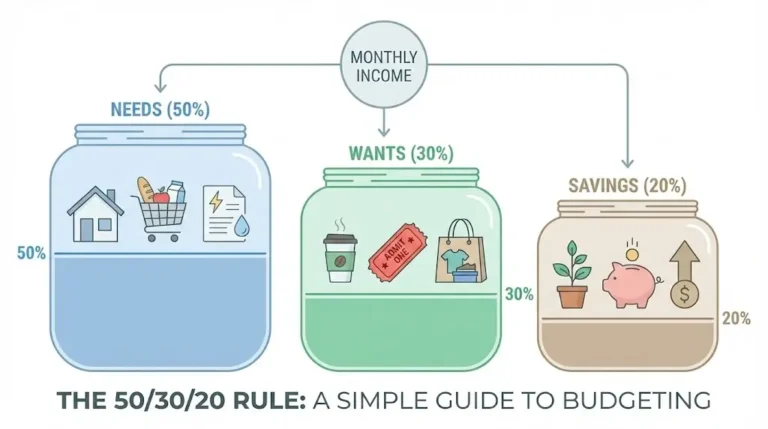

10. Adopt the 50/30/20 Budgeting Rule

Allocate 50% of your income to needs, 30% to wants, and 20% to savings/investing. This simple framework ensures you are always building your safety net while still enjoying life.

11. Buy Refurbished or Second-Hand Tech

Need a new laptop for your side hustle? Never buy brand new.

- Pro Tip: Check Apple Certified Refurbished or reputable eBay sellers. You get a device that looks and performs like new, usually with a warranty, for 20-40% less.

12. Create a “Sinking Fund” for Irregular Expenses

Car repairs, holiday gifts, and annual premiums often derail budgets because they aren’t monthly.

- Action Step: Divide the estimated annual cost of these events by 12, and save that amount monthly in a dedicated “Sinking Fund” envelope or sub-account.

13. DIY Routine Maintenance and Simple Repairs

From changing your car’s air filter to fixing a leaky faucet, YouTube is a goldmine of free tutorials. Stop paying $100/hour for labor on tasks you can safely do yourself in 20 minutes.

Income Potential & Earnings Breakdown

While you aren’t “making” new money, a penny saved is a penny earned. Here is a realistic breakdown of how these money saving hacks translate into retained earnings (your personal profit margins):

| Savings Category | Estimated Monthly Savings | Annual Income Retained |

|---|---|---|

| Dining Out / Coffee | $150 – $300 | $1,800 – $3,600 |

| Subscription Audit | $30 – $80 | $360 – $960 |

| Bill Negotiation | $40 – $100 | $480 – $1,200 |

| Generic Groceries | $100 – $200 | $1,200 – $2,400 |

| Total Potential | $320 – $680/mo | **$3,840 – $8,160/year** |

Disclaimer: Earnings and savings vary wildly based on your starting income, geographical location, and current spending habits.

Alternative Methods & Variations

If traditional budgeting feels too restrictive, try these variations:

- The Zero-Based Budget: Give every single dollar a “job” at the beginning of the month so your income minus expenses equals exactly zero.

- The Cash Envelope System: Best for chronic overspenders. Withdraw your “wants” budget in cash. When the envelope is empty, you stop spending.

- The No-Spend Month Challenge: A highly aggressive variation where you commit to 30 days of buying absolutely nothing except bare-bones essentials (rent, utilities, basic groceries). Great for a quick cash injection for your monetization strategies.

Best Practices & Optimization Tips

To maximize the impact of your money saving hacks, focus on these advanced optimization tips:

- Gamify Your Savings: Challenge a friend or spouse to see who can save the most in a week.

- Use the Right Tools: Automate your insights with apps like Monarch Money or Copilot.

- Community Support: Join subreddits like r/personalfinance or r/frugal to stay motivated and discover niche-specific savings tricks.

Common Mistakes to Avoid

Even well-intentioned savers fall into traps. Avoid these common pitfalls:

- Frugal Fatigue: Depriving yourself of everything you enjoy will lead to a spending binge. Budget for “fun money” intentionally.

- Focusing on Pennies, Ignoring Dollars: Spending 3 hours clipping coupons to save $2, while ignoring a $400/month car payment, is a poor use of time. Focus on big wins first.

- Not Tracking Small Cash Expenses: That $4 daily coffee seems harmless until you realize it’s draining over $1,400 a year from your potential investments.

Long-Term Sustainability & Growth

Saving money is only half the equation. To achieve true financial freedom, you must transition from a “saver” to an “investor.”

Once you have optimized your everyday expenses, take that newly freed-up $500 a month and deploy reinvestment strategies. Use it to fund inventory for an e-commerce store, buy dividend-paying index funds, or invest in courses to learn high-income skills.

By diversifying your efforts—combining strict money management with active revenue streams—you future-proof your finances against inflation and economic downturns.

Conclusion

Mastering these 13 money saving hacks is the ultimate first step toward taking control of your financial destiny. By automating your savings, cutting the fat from your subscriptions, and adopting a mindful spending approach, you can easily free up thousands of dollars a year to fund your dreams.

Remember, it’s not always about how much you make, but how much you keep.

Ready to start your journey? Drop your biggest budgeting challenge in the comments below! Subscribe to our newsletter for weekly money-making strategies, and be sure to share your progress in our community.

FAQs

How much money can I realistically make or save with these hacks?

While it depends on your current spending habits, the average person can save between $300 to $600 a month by rigorously applying these strategies, translating to $3,600 to $7,200 annually.

Do I need prior financial experience to start budgeting?

Not at all. These money saving hacks are designed for beginners. If you can use a basic smartphone app or a simple spreadsheet, you have all the experience required.

What’s the initial investment required?

Zero dollars. Unlike starting a business, optimizing your current expenses requires only an investment of your time—usually 1 to 3 hours to set up your initial budget.

How long until I see results?

You will see immediate results on your very next paycheck by simply canceling unused subscriptions and halting impulse purchases. Long-term compounding results become highly visible within 60 to 90 days.

Are these methods still working in the current economic climate?

Yes, they are more relevant now than ever. With rising inflation, tactics like negotiating bills, meal prepping, and cash-back stacking are vital for maintaining your purchasing power.

What are the risks involved?

There is virtually zero financial risk in saving money. The only “risk” is falling into frugal fatigue by being too restrictive, which is easily prevented by intentionally budgeting a small amount of “fun money” each month.

Before you go, tap those stars!

Straightforward, no gimmicks, just solid banking advice

I clicked on this article expecting it to push some specific bank or financial product with referral links. I was pleasantly surprised. The advice was unbiased, focused on principles rather than promoting any particular institution, and gave me a clear framework to evaluate my own options. I appreciated that the article addressed the importance of FDIC insurance, automatic transfers, and goal-setting — things that seem obvious but that most people (including me) overlook. The writing was clear and concise, without the usual fluff or overly complex financial jargon. The only reason I’m giving four stars instead of five is that I would have liked even more detail on how to balance saving with paying down debt. Still, this was one of the most practical and trustworthy articles on saving I’ve read in a long time. Highly recommend.

Solid advice that cuts through the noise

I’ve been saving for years, but I kept wondering if my money was actually working as hard as it could be. There’s so much conflicting information out there — regular savings accounts, money market accounts, CDs, high-yield options — it gets confusing fast. This article did an excellent job comparing the options side by side, explaining the pros and cons of each, and helping me figure out which strategy made sense for my situation. I especially appreciated the section on the importance of emergency funds versus long-term savings, and the breakdown of how compound interest really adds up over time. I ended up moving my savings to a high-yield account and setting clearer goals. Practical, well-researched, and genuinely helpful.

Small changes, noticeable results

I’ll be honest — I clicked on this article expecting generic advice like “drive less” (thanks, captain obvious). But I was genuinely impressed. The article breaks down the actual science behind why certain habits affect fuel economy, with real numbers to back it up. I learned that my lead-foot acceleration and speeding were costing me way more than I realized. The section on vehicle maintenance was especially valuable — I didn’t know a dirty air filter could impact mileage that much. The tone was straightforward, no fluff, no upselling expensive products. Just solid, practical advice that actually works. My fuel expenses dropped by about 15% last month without me changing my overall driving needs.

Finally, practical advice that doesn’t require buying a new car

As someone who drives over 400 miles a week for work, gas expenses have been crushing my budget. I’ve read countless articles that basically just say “buy an electric vehicle” — which isn’t helpful when that’s not in my budget. This article was a game-changer. The tips were immediately actionable: combining trips, checking tire pressure (I didn’t realize how much that affects mileage!), and using gas price apps. I started implementing these suggestions last month, and I’ve already saved about $40. The writing was clear, well-organized, and respected that not everyone can just trade in their car. Highly recommend for anyone feeling the pain at the pump.

Perfect for renters who can’t install solar panels

As someone who rents an apartment, I often feel limited when it comes to making my home more energy-efficient. I can’t just install new appliances or add insulation to the walls. This article was a lifesaver because it focused on renter-friendly solutions—things like weatherstripping for doors, smart power strips, and optimizing how I use my existing appliances. The writing was straightforward and didn’t assume I owned a home. My only small critique is that I would have loved even more rent-specific examples, but overall, this was incredibly helpful. My electric bill dropped by about $15 last month!