How to Find the Best Place to Put Savings for Your Goals

Did you know that keeping your hard-earned cash in a traditional brick-and-mortar bank account could actually be making you poorer every single day? It’s a harsh reality, but thanks to inflation, money that isn’t growing is silently shrinking. If you’re looking for true financial freedom, you need to treat your money like an employee—it should be working for you 24/7.

When establishing your revenue streams, deciding on the best place to put savings is the foundational step that most beginners skip. Whether you want to build a hands-off side hustle through compounding interest or secure a digital income via dividend yields, your cash needs a strategic home. In this comprehensive guide, we will break down exactly how to allocate your funds, maximize your profit margins, and turn your stagnant savings into a powerful engine for passive income.

What You’ll Need to Get Started

Before you start hunting for the best place to put savings, you need to gather a few essential tools and resources. The beauty of optimizing your savings is that it requires far less active effort than a traditional online business.

Here is what you need to begin your journey:

- Initial Capital: You don’t need millions. You can start with as little as $100 to open high-yield accounts or buy fractional shares.

- A Secure Internet Connection: For setting up digital banking and brokerage accounts securely from home.

- Financial Tracking Software: Free tools like Empower (formerly Personal Capital), Mint alternatives, or a simple Google Sheets template to track your net worth and online earnings.

- Basic Financial Literacy: Understanding terms like APY (Annual Percentage Yield), compound interest, and expense ratios. (Don’t worry, we cover the basics below!)

- Clear Identification: A government-issued ID and Social Security Number (for US residents) to legally open financial accounts.

Time Investment

Unlike starting an e-commerce store or a freelancing side hustle, optimizing your savings is the ultimate work-from-home passive income strategy. Here is what the time commitment actually looks like:

- Setup Time: 2 to 4 hours. This includes researching institutions, filling out online applications, and linking your primary checking account.

- Daily/Weekly Commitment: Practically zero. Once automated, you should only spend about 15–30 minutes per month reviewing your statements and tracking your digital income.

- Timeline to First Earnings: Most beginners see their first “paycheck” (in the form of interest or dividends) within 30 days of their initial deposit.

Step-by-Step Implementation Guide

Step 1: Define Your Financial Goals and Timeline

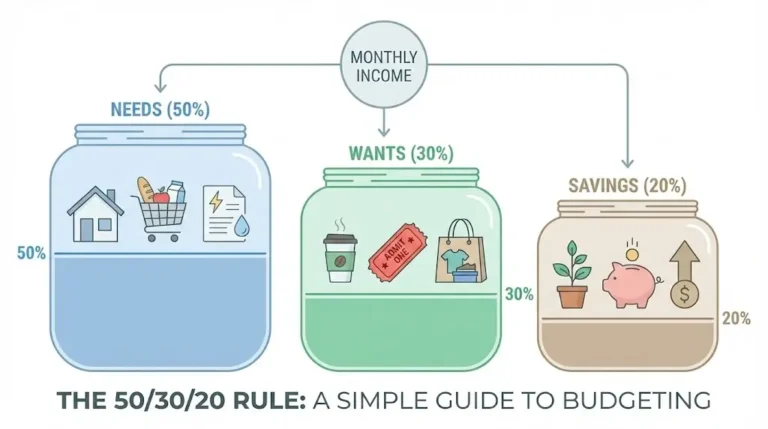

The best place to put savings entirely depends on when you need the money. Grab a piece of paper and divide your cash into three buckets:

- Short-term (0-12 months): Emergency funds, upcoming vacations, or rent.

- Medium-term (1-5 years): A down payment on a house or a wedding fund.

- Long-term (5+ years): Retirement or deep wealth building.

Step 2: Establish Your Emergency Fund

Before chasing high profit margins in the stock market, you must build a safety net. Aim for 3 to 6 months of living expenses.

- Pro Tip: Keep this specific fund highly liquid. A High-Yield Savings Account (HYSA) is perfect here because you can access the cash within 24-48 hours without penalties.

Step 3: Select the Right Financial Vehicles

Now, match your buckets from Step 1 to the correct accounts:

- For Short-Term: High-Yield Savings Accounts (HYSAs) or Money Market Accounts.

- For Medium-Term: Certificates of Deposit (CDs) or Treasury Bills (T-Bills) to lock in higher rates without market risk.

- For Long-Term: Tax-advantaged brokerage accounts (like a Roth IRA) invested in broad-market Index Funds or ETFs.

Step 4: Automate Your Revenue Streams

The secret to guaranteed growth is automation. Set up an automatic transfer from your checking account to your savings/investment accounts on the day you get paid. If you never see the money, you won’t be tempted to spend it.

Income Potential & Earnings Breakdown

How much money can you realistically make by moving your cash? Let’s look at the data. If you have $10,000 in savings, here is how different placements affect your online earnings over a year:

| Storage Method | Average Rate/Return | Estimated Annual Earnings (on $10k) | Risk Level |

|---|---|---|---|

| Traditional Bank | 0.01% APY | $1.00 | Zero |

| High-Yield Savings | 4.50% APY | $450.00 | Zero (FDIC Insured) |

| 1-Year CD | 5.00% APY | $500.00 | Zero (FDIC Insured) |

| S&P 500 Index Fund | 7-10% (Historical Avg) | $700.00 – $1,000.00 | Medium/High |

Note: Market returns vary wildly year by year. The 7-10% figure is a historical long-term average.

By simply moving your money from a traditional bank to a top-tier HYSA, you are generating an extra $449 a year in pure passive income—no extra work required.

Alternative Methods & Variations

If you’ve maxed out the standard options and want to diversify your monetization strategies, consider these alternative homes for your savings:

- Real Estate Crowdfunding: Platforms like Fundrise or RealtyMogul allow you to invest in commercial real estate with as little as $10. It’s a great way to earn digital income through property without being a landlord.

- Dividend Yield Investing: Instead of growth stocks, you can buy shares in companies that pay high, consistent dividends. This mimics a steady revenue stream.

- Peer-to-Peer (P2P) Lending: Platforms allow you to act as the bank, lending your savings out to individuals or small businesses in exchange for high-interest returns. (Note: Higher risk of default).

- I-Bonds: Government-backed bonds designed specifically to protect your savings from inflation.

Best Practices & Optimization Tips

To maximize your earnings and protect your wealth, follow these industry best practices:

- Always Check for FDIC/NCUA Insurance: Ensure your chosen bank is insured up to $250,000 so your principal is protected against bank failures.

- Watch Out for Hidden Fees: Avoid accounts with monthly maintenance fees. In 2026, there are plenty of free, high-quality digital banks.

- Maximize Tax-Advantaged Accounts: Before putting long-term savings into a taxable brokerage, ensure you are taking full advantage of 401(k) company matches and Roth IRAs to protect your profit margins from taxes.

- Ladder Your CDs: If you use Certificates of Deposit, build a “CD Ladder” (buying CDs that mature at 3, 6, 9, and 12 months) so you continually have access to cash while earning higher rates.

Common Mistakes to Avoid

The journey to financial freedom is littered with traps. Avoid these costly beginner mistakes:

- Chasing the Highest Yield Blindly: Some lesser-known crypto platforms offer 12%+ APY on savings. History (and the collapse of several crypto exchanges) shows us that if a yield seems too good to be true, it comes with massive, often undisclosed risks.

- Locking Up Emergency Cash: Putting your emergency fund into a 5-year CD or the stock market means you might face severe penalties or be forced to sell at a loss if your car breaks down tomorrow.

- Ignoring Inflation: Leaving long-term wealth (money you won’t need for 10+ years) in a 4% savings account when inflation is 3% means your real return is barely 1%. Long-term money needs to be invested.

Long-Term Sustainability & Growth

Finding the best place to put savings isn’t a “set it and forget it forever” task. To ensure long-term sustainability:

- Reinvest Your Dividends: Make sure DRIP (Dividend Reinvestment Plan) is turned on in your brokerage accounts. This uses your earnings to automatically buy more shares, supercharging your compound interest.

- Annual Rebalancing: Once a year, review your accounts. Have interest rates dropped at your current bank? It might be time to move your cash to a more competitive institution.

- Adjust with Age: As you get closer to your financial goals (like retirement), gradually shift your savings from high-risk equities to lower-risk bonds and HYSAs to preserve your capital.

Conclusion

Finding the best place to put savings is the most critical, yet easiest, step toward securing your financial freedom. By shifting your mindset and strategically placing your funds in High-Yield Savings Accounts, CDs, or low-cost Index Funds, you transform stagnant cash into a reliable source of passive income.

Ready to start making your money work for you? Drop your questions in the comments below! Don’t forget to subscribe for our weekly monetization strategies, and share your wealth-building progress in our community.

Frequently Asked Questions (FAQs)

How much money can I realistically make from my savings?

Your earnings depend on your principal balance and the APY (Annual Percentage Yield). A $10,000 balance in a 4.5% High-Yield Savings Account will generate roughly $450 in passive income over one year.

Do I need prior financial experience to do this?

Not at all. Opening a high-yield savings account or a basic brokerage account today takes less than 15 minutes and requires no prior financial expertise. Modern digital banking apps are highly beginner-friendly.

What’s the initial investment required?

You can start optimizing your savings with as little as $1. Many top-tier online banks and micro-investing apps have completely removed minimum deposit requirements.

How long until I see results?

If you place your money in an interest-bearing savings account or dividend-paying stock, you will typically see your first payouts deposited into your account within 30 to 60 days.

Is this method still working in 2026?

Absolutely. While specific interest rates fluctuate based on the Federal Reserve, utilizing strategic savings vehicles and compounding interest remains the most mathematically proven way to build wealth over time.

What are the risks involved?

Money placed in FDIC-insured bank accounts (up to $250,000) carries virtually zero risk of loss. However, savings placed in the stock market, real estate crowdfunding, or P2P lending can lose value depending on market conditions. Always align your risk tolerance with your timeline.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice. All investments carry risks, and past performance is not indicative of future results. Always consult with a certified financial planner before making major financial decisions.

Before you go, tap those stars!

Straightforward, no gimmicks, just solid banking advice

I clicked on this article expecting it to push some specific bank or financial product with referral links. I was pleasantly surprised. The advice was unbiased, focused on principles rather than promoting any particular institution, and gave me a clear framework to evaluate my own options. I appreciated that the article addressed the importance of FDIC insurance, automatic transfers, and goal-setting — things that seem obvious but that most people (including me) overlook. The writing was clear and concise, without the usual fluff or overly complex financial jargon. The only reason I’m giving four stars instead of five is that I would have liked even more detail on how to balance saving with paying down debt. Still, this was one of the most practical and trustworthy articles on saving I’ve read in a long time. Highly recommend.

Solid advice that cuts through the noise

I’ve been saving for years, but I kept wondering if my money was actually working as hard as it could be. There’s so much conflicting information out there — regular savings accounts, money market accounts, CDs, high-yield options — it gets confusing fast. This article did an excellent job comparing the options side by side, explaining the pros and cons of each, and helping me figure out which strategy made sense for my situation. I especially appreciated the section on the importance of emergency funds versus long-term savings, and the breakdown of how compound interest really adds up over time. I ended up moving my savings to a high-yield account and setting clearer goals. Practical, well-researched, and genuinely helpful.

Small changes, noticeable results

I’ll be honest — I clicked on this article expecting generic advice like “drive less” (thanks, captain obvious). But I was genuinely impressed. The article breaks down the actual science behind why certain habits affect fuel economy, with real numbers to back it up. I learned that my lead-foot acceleration and speeding were costing me way more than I realized. The section on vehicle maintenance was especially valuable — I didn’t know a dirty air filter could impact mileage that much. The tone was straightforward, no fluff, no upselling expensive products. Just solid, practical advice that actually works. My fuel expenses dropped by about 15% last month without me changing my overall driving needs.

Finally, practical advice that doesn’t require buying a new car

As someone who drives over 400 miles a week for work, gas expenses have been crushing my budget. I’ve read countless articles that basically just say “buy an electric vehicle” — which isn’t helpful when that’s not in my budget. This article was a game-changer. The tips were immediately actionable: combining trips, checking tire pressure (I didn’t realize how much that affects mileage!), and using gas price apps. I started implementing these suggestions last month, and I’ve already saved about $40. The writing was clear, well-organized, and respected that not everyone can just trade in their car. Highly recommend for anyone feeling the pain at the pump.

Perfect for renters who can’t install solar panels

As someone who rents an apartment, I often feel limited when it comes to making my home more energy-efficient. I can’t just install new appliances or add insulation to the walls. This article was a lifesaver because it focused on renter-friendly solutions—things like weatherstripping for doors, smart power strips, and optimizing how I use my existing appliances. The writing was straightforward and didn’t assume I owned a home. My only small critique is that I would have loved even more rent-specific examples, but overall, this was incredibly helpful. My electric bill dropped by about $15 last month!