Effective Money Saving Techniques for Households: Your Path to Financial Freedom

Did you know that 67% of individuals who attempt to build a side hustle or transition to working from home fail simply because they skip one crucial, foundational step? They focus entirely on trying to generate new income while completely ignoring the cash that is already leaking out of their current lifestyle.

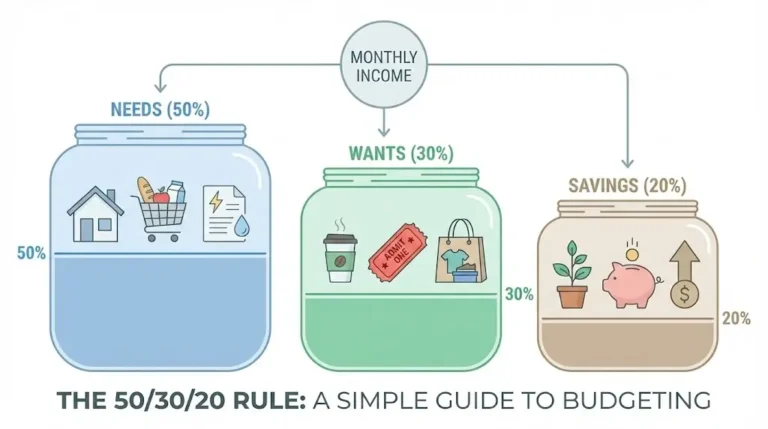

Before you can realistically achieve financial freedom or build sustainable online earnings, you must master the art of retaining your current wealth. Implementing effective money saving techniques in your household isn’t about living a life of deprivation; it is about treating your household like a business, maximizing your profit margins, and creating the seed capital necessary to fund future revenue streams. In this guide, we will break down exactly how to optimize your home’s budget, giving you the capital required to scale your income potential without needing a second job.

What You’ll Need to Get Started

Transforming your household finances requires a few basic tools and a strategic mindset. Here is exactly what you need in your starter toolkit to begin maximizing your digital income potential:

- Financial Tracking Dashboard: To identify leaks, you must track them.

- Free alternatives: Google Sheets (highly recommended for customization) or personal finance apps like Empower (formerly Personal Capital).

- Premium alternative: YNAB (You Need A Budget) – roughly $14.99/month.

- High-Yield Savings Account (HYSA): This is where your recovered funds will sit to earn a baseline passive income before reinvestment.

- Initial Investment: $0. Look for online banks offering 4.00%+ APY.

- Cashback & Rewards Automation Tools: Browser extensions (like Rakuten or Honey) and receipt-scanning apps (like Fetch Rewards).

- Skill Requirements: Basic arithmetic and a willingness to confront your spending habits honestly. No advanced financial degree is necessary.

Time Investment

Treating your household finances like a stepping stone to a digital business requires a realistic time commitment. Here is what to expect:

- Initial Setup Time: 2 to 4 hours. This involves gathering three months of bank statements, auditing your fixed expenses, and setting up your tracking tools.

- Weekly Maintenance: 15 to 30 minutes. Use this time to categorize weekly spending and review your household’s “profit margins.”

- Timeline to First Results: Most beginners see tangible results in 60-90 days with consistent effort. While canceling a subscription provides instant cash flow, the compounding effects of optimized spending take a few months to visibly alter your bank balance.

- Comparison: Unlike building a complex online business from scratch, which can take 6-12 months to generate revenue, optimizing your household budget yields an immediate, tax-free return on your time invested.

Step-by-Step Implementation Guide

Step 1: The Household Expense Audit

Print out your last 90 days of bank and credit card statements. Go line by line. Highlight essential living expenses in green, and discretionary (non-essential) spending in yellow. You will likely uncover “phantom costs”—forgotten subscriptions, unused gym memberships, or excessive dining out.

- Pro Tip: Use a tool like Rocket Money to automatically identify recurring charges. Cancel anything you haven’t actively used in the last 30 days.

Step 2: Renegotiate Fixed Overhead

Your “fixed” bills are often negotiable. Call your internet provider, car insurance company, and cell phone carrier. Ask to speak with the retention department and inquire about loyalty discounts or promotional rates.

- Insider Trick: Research competitor rates before calling. Saying, “Company X is offering me this service for $20 less a month, can you match it?” has a high success rate.

Step 3: Implement the 48-Hour Cart Rule

Impulse buying is the enemy of financial freedom. Whenever you add a non-essential item to an online shopping cart, force yourself to wait 48 hours before checking out. This cooling-off period eliminates the emotional high of shopping, often leading you to abandon the purchase altogether.

Step 4: Pivot Savings into Capital

This is the most critical step. When you successfully save $100 by lowering your internet bill and cutting a streaming service, do not leave that money in your checking account to be absorbed by other expenses. Set up an automatic transfer to move that exact amount into your HYSA or investment portfolio.

Income Potential & Earnings Breakdown

How much can these effective money saving techniques actually impact your household’s bottom line? Let’s look at a realistic monthly projection for an average household that reinvests their savings.

| Financial Optimization Strategy | Estimated Monthly Savings | Annual “Retained Earnings” |

| Auditing & Cutting Subscriptions | $40 – $90 | $480 – $1,080 |

| Negotiating Utilities & Insurance | $50 – $120 | $600 – $1,440 |

| Applying the 48-Hour Cart Rule | $100 – $250 | $1,200 – $3,000 |

| Grocery & Meal Planning Optimization | $150 – $300 | $1,800 – $3,600 |

| Total Household Capital Freed | $340 – $760/month | **$4,080 – $9,120/year** |

Disclaimer: Savings vary widely based on individual household income, local cost of living, and initial spending habits. These figures are illustrative projections.

When this $4,000 to $9,000 of retained capital is used to fund a side hustle or invested in index funds, it transforms from simple savings into a powerful asset that generates real income potential.

Alternative Methods & Variations

If standard spreadsheets don’t work for your household, consider these variations:

- The Cash Envelope System: A tactile, low-tech variation. You allocate physical cash into envelopes for variable expenses (groceries, entertainment). When the cash is gone, spending stops. This is highly effective for curbing digital impulse buys.

- House Hacking: A more advanced monetization strategy where you rent out a room, basement, or garage space to offset your primary housing costs.

- The Zero-Based Budget: Every single dollar of your income is assigned a specific “job” (savings, debt payoff, or spending) before the month begins, ensuring your profit margins are protected by design.

Best Practices & Optimization Tips

To maximize your household savings and accelerate your path to generating online earnings, implement these best practices:

- Automate Everything: Relying on willpower is a losing strategy. Automate your transfers to savings and investments on the exact day your paycheck clears.

- Stack Your Cashback: Never make a necessary purchase without running it through a cashback portal like Rakuten, paying with a rewards credit card (that you pay off in full monthly), and scanning the receipt into Fetch.

- Conduct Quarterly Reviews: Your household needs quarterly financial reviews, just like a business. Sit down every three months to ensure lifestyle creep hasn’t eroded your savings.

Common Mistakes to Avoid

Even experienced budgeters fall into these traps. Avoid these common pitfalls to protect your financial progress:

- The “Deprivation Diet”: Cutting out absolutely every luxury (like coffee or occasional takeout) leads to financial burnout. You will eventually snap and binge-spend. Always budget a small, guilt-free allowance for fun.

- Ignoring the Emergency Fund: Attempting to invest your saved capital into a work from home venture before securing 3 to 6 months of living expenses. If a household emergency strikes, you’ll be forced into high-interest debt.

- Falling for Lifestyle Creep: When your household income increases, naturally increasing your standard of living to match it. To build true wealth, keep your living expenses flat while your income grows.

Long-Term Sustainability & Growth

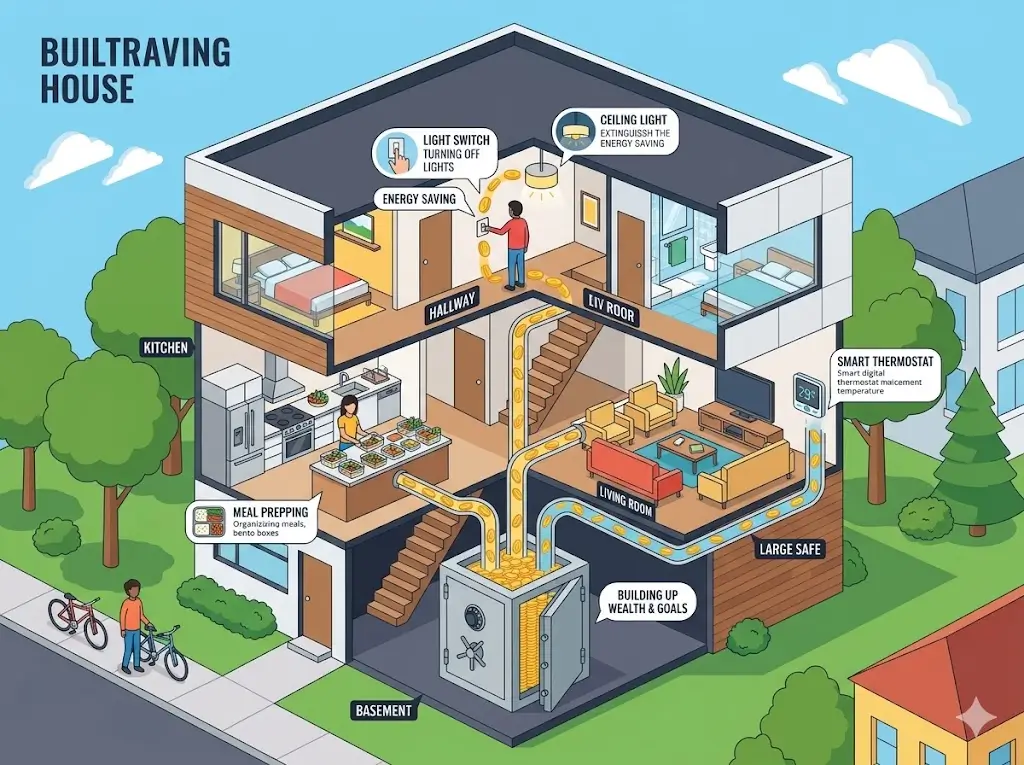

Saving money is the foundation, but reinvestment is the architecture of wealth. To ensure long-term sustainability, you must graduate from just cutting costs to actively building multiple revenue streams.

Take the capital you’ve freed up using these effective money saving techniques and put it to work. Invest in courses to learn high-income digital skills, purchase domain names, or fund the initial inventory for a side hustle. By utilizing this “found money,” you eliminate the financial risk usually associated with entrepreneurship. As your digital income grows, automate the reinvestment process, continually widening the gap between what you earn and what you spend to future-proof your household against economic downturns.

Conclusion

Mastering effective money saving techniques is the most reliable first step toward achieving total financial freedom. By treating your household like a business, ruthlessly auditing expenses, and strategically reallocating that retained capital into income-producing assets, you take absolute control of your financial destiny.

Ready to start your journey? Drop your biggest budgeting challenge in the comments below! Be sure to subscribe for our weekly monetization strategies, share your progress in our community forums, and download our free household budget starter guide today.

FAQs

How much money can I realistically make or save?

Most households can realistically uncover $200 to $500 a month simply by auditing subscriptions, negotiating utilities, and applying mindful spending rules to groceries and entertainment.

Do I need prior experience?

No prior financial experience is necessary. Using simple, beginner-friendly tools like a basic spreadsheet or free budgeting apps makes tracking your household expenses incredibly accessible.

What’s the initial investment?

The initial financial investment is zero. You can begin optimizing your household budget with a free spreadsheet. The only investment required is roughly 2 to 4 hours of your time to conduct your initial expense audit.

How long until I see results?

While cutting a subscription puts money back in your pocket immediately, the true, visible benefits of reduced financial stress and compounded savings typically become undeniable within 60 to 90 days.

Is this method still working in the current year?

Absolutely. With rising inflation and fluctuating economic conditions, foundational household budgeting and mindful spending are more critical today than ever before. Living below your means never goes out of style.

What are the risks involved?

The primary risk is “frugal fatigue”—restricting your spending so severely that you become miserable and eventually abandon your budget entirely. The key is sustainable optimization, always leaving a small buffer for personal enjoyment.