Budget Categories That Simplify Money Management

Did you know that 67% of online entrepreneurs fail because they skip this ONE crucial step? While they focus intensely on monetization strategies and traffic generation, they often ignore the “back end” of their business: their personal cash flow. Without clear budget categories, your online earnings can vanish into a black hole of untracked spending, leaving you with zero capital to reinvest in your growth.

Mastering your budget categories is not just about restriction; it is about strategic allocation. It is the process of creating a financial map that ensures every dollar you earn—whether from a 9-to-5 or a side hustle—is working toward your financial freedom. In this guide, we will break down the essential categories that simplify money management and show you how to widen your profit margins to fund your digital empire.

What You’ll Need to Get Started

To build a system of budget categories that actually works, you need to move beyond mental math and into a data-driven environment.

- Tracking Platform: A dedicated app like YNAB (You Need A Budget) or a customized Google Sheets template.

- Historical Data: Access to your last 60–90 days of bank and credit card statements.

- Categorization Legend: A simple list of “Needs,” “Wants,” and “Growth” categories.

- Initial Investment: $0 (Free). While premium apps have costs, you can launch a world-class budgeting system using free tools and spreadsheets.

- Skill Requirements: Basic spreadsheet navigation and the discipline to categorize transactions weekly.

Time Investment

Correctly setting up your budget categories is a high-leverage activity that pays dividends in reclaimed time and money.

- Setup Phase: 2–3 hours. This involves auditing your past spending to see which budget categories currently dominate your life.

- Weekly Maintenance: 15 minutes. A “Sunday Review” to ensure your digital income is allocated correctly.

- Monthly Optimization: 30 minutes. Adjusting your categories based on your income potential for the coming month.

- Timeline to Results: Most beginners feel a sense of “financial clarity” within 30 days and see a tangible increase in investable capital within 60 to 90 days.

- Comparison: Unlike traditional income methods that require 40+ hours a week, 15 minutes of weekly budgeting can effectively “earn” you hundreds of dollars by eliminating waste.

Step-by-Step Implementation Guide

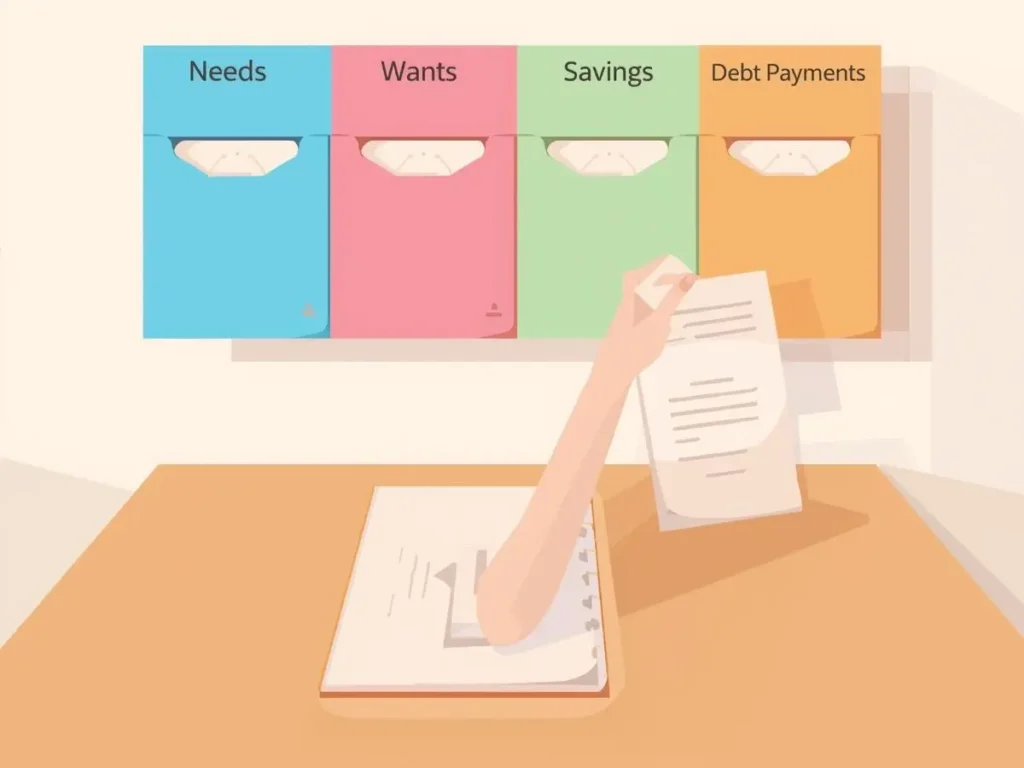

1. Define Your “Core Four” Fixed Categories

Your budget should start with the non-negotiables. These are the fixed costs that stay consistent.

- Housing: Rent/Mortgage, taxes, and insurance.

- Utilities: Electricity, water, and internet (essential for your work from home setup).

- Transportation: Car payments, fuel, and maintenance.

- Basic Food: Your baseline grocery budget.

2. Isolate Your “Side Hustle Operating Costs”

If you are pursuing online earnings, you must treat your business expenses as a separate category. This simplifies tax season and protects your profit margins.

- Subscriptions: Web hosting, email marketing tools, and professional software.

- Marketing: Ad spend or social media management tools.

- Education: Books, courses, and coaching to increase your income potential.

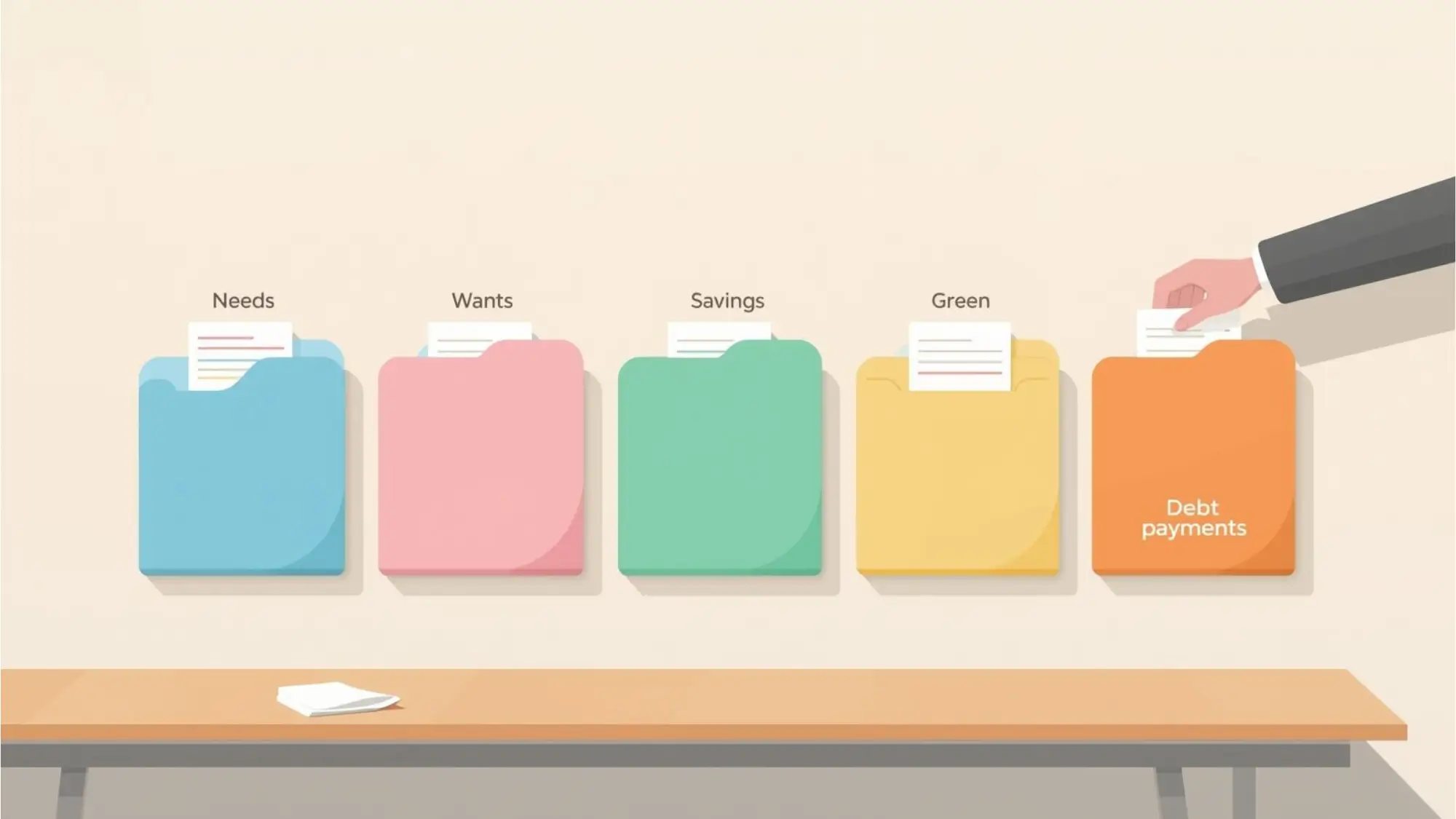

3. Establish the “Flex” Categories (Variable Spending)

These are the budget categories where most people lose their monetization strategies funding.

- Dining Out: Anything above basic groceries.

- Entertainment: Movies, streaming services, and hobbies.

- Shopping: Clothing and household non-essentials.

- Pro Tip: Give yourself a “Guilt-Free Spending” category. If you try to cut “fun” to zero, you will eventually burn out and quit.

4. Create a “Wealth Acceleration” Category

This is the most important section for those seeking financial freedom. Instead of “Savings,” call this your “Wealth Fund.”

- Emergency Fund: 3–6 months of fixed costs.

- Investment Capital: Money for dividend stocks, index funds, or digital assets.

- Passive Income Seed: Capital specifically set aside to launch new revenue streams.

5. The “Buffer” and Irregular Category

Avoid the mistake of a “Miscellaneous” catch-all.

- Sinking Funds: Small monthly contributions for annual costs like car registration, holiday gifts, and quarterly taxes.

- Buffer: A small $50–$100 amount to handle rounding errors and minor price fluctuations.

Income Potential & Earnings Breakdown

How do budget categories lead to higher income? By identifying “Leakage” and turning it into “Leverage.”

| Category Strategy | Estimated Monthly Recovery | 1-Year Impact | 5-Year Growth (at 7%) |

|---|---|---|---|

| Basic Cleanup | $200 | $2,400 | $14,350 |

| Moderate Optimization | $500 | $6,000 | $35,880 |

| Aggressive Scaling | $1,200+ | $14,400+ | $86,110+ |

Data Example: A digital marketer audited their budget categories and found $300/month in unused “Ghost” subscriptions. By redirecting that $3,600/year into a side hustle (Content outsourcing), they grew their passive income from $0 to $2,000/month within two years.

Alternative Methods & Variations

Standard budget categories can be adapted based on your specific financial stage:

- The 50/30/20 Rule: 50% Needs, 30% Wants, 20% Financial Goals. Simple and effective for beginners.

- Zero-Based Budgeting: Giving every dollar a “job” until your income minus expenses equals exactly zero. Best for those scaling a side hustle.

- The Anti-Budget: Focus only on your “Wealth Acceleration” category. If you hit that goal first, the rest is free to spend.

- Niche Variations: The “Digital Nomad” budget (focusing on travel/connectivity) or the “Frugal Startup” budget (minimizing all personal costs to maximize business reinvestment).

Best Practices & Optimization Tips

- Automate Your Categories: Use bank rules to automatically sort transactions. This ensures you spend more time on monetization strategies and less on data entry.

- Audit Your Tech Stack: For those who work from home, review your software budget categories quarterly. Are there free alternatives?

- The 48-Hour Rule: For variable categories, wait 48 hours before buying. This protects your profit margins from impulse buys.

- Reinvest the Surplus: The moment a category comes in under budget, move that surplus into your “Investment Capital” category immediately.

Common Mistakes to Avoid

- The “Miscellaneous” Trap: Having a large uncategorized section is a sign of poor management. Statistic: People with a large “Misc” category spend 15% more on average than those with defined categories.

- Ignoring Irregular Costs: Failing to use “Sinking Funds” for annual bills is the #1 reason budgets fail.

- Being Too Granular: Having 50 budget categories leads to “analysis paralysis.” Stick to 10–12 high-level buckets.

- Treating Wants as Needs: Your Netflix subscription is a “Want,” even if it feels like a “Need” during a long work from home week. Be honest with your data.

Long-Term Sustainability & Growth

Budgeting is a marathon that leads to financial freedom. To maintain this system:

- Reinvestment Strategy: As your online earnings grow, don’t inflate your lifestyle categories. Instead, increase the percentage allocated to your “Wealth Acceleration” fund.

- Automation: Use tools like Zapier or built-in bank automations to move money between categories the moment you get paid.

- Diversification: Once your core budget categories are stable, use your surplus to build multiple revenue streams across different asset classes.

Conclusion

Simplifying your budget categories is the ultimate “force multiplier” for your finances. It provides the visibility needed to protect your profit margins and the capital required to fund your monetization strategies. By moving from a chaotic “one-pile” approach to a structured, categorical system, you turn your personal finances into a launchpad for digital income and long-term financial freedom.

Ready to start your journey? Drop your questions in the comments below! Subscribe for weekly money-making strategies, and download our free starter guide to begin tracking your progress today.

FAQs

How much money can I realistically make/save?

Most people find an extra $300–$600 per month by simply defining their budget categories and eliminating invisible leaks. This can grow into a $40,000+ asset over five years if reinvested.

Do I need prior experience?

No. Most modern budgeting tools are designed for beginners. You only need to be able to read your bank statements and follow the “Core Four” structure.

What’s the initial investment?

The initial investment is $0. You can use free spreadsheets or pen and paper. The real value is your time and consistency.

How long until I see results?

You will see “found money” in your first 30-day audit. The compounding effect of reinvesting that money into your online earnings usually becomes significant within 6 to 12 months.

Is this method still working in 2026?

Absolutely. With high inflation and the rise of the subscription economy, having clear budget categories is more vital for financial freedom than ever before.

What are the risks involved?

The primary risk is “over-restriction.” If you don’t allow for a “Fun” category, you may experience budget burnout. Balance is key to long-term sustainability.