Sinking Funds: How They Support Financial Stability

Did you know that according to a landmark U.S. Bank study, 82% of small businesses and online side hustles fail due to poor cash flow management, not a lack of sales? Many digital entrepreneurs focus entirely on generating revenue but completely ignore how to manage irregular expenses. If you want to achieve true financial stability, you cannot rely on a generic savings account or cross your fingers when tax season arrives.

To build lasting wealth and safely scale your work from home endeavors, you need a proactive cash management system. Enter the “sinking fund.” A sinking fund is a strategic pool of money set aside each month to pay for a known future expense. Whether you are generating digital income from a laptop or scaling a high-level agency, mastering sinking funds is the ultimate bridge between scraping by and achieving true financial freedom. In this guide, we will break down exactly how sinking funds support financial stability, protect your profit margins, and keep your business thriving year-round.

What You’ll Need to Get Started

Building a network of sinking funds doesn’t require complex software or a degree in finance. To secure your online earnings, you only need a few basic tools to get your system off the ground.

- A High-Yield Savings Account (HYSA): Essential for earning passive income on the cash you are setting aside. Look for accounts like Ally, SoFi, or Capital One that offer “buckets” or sub-accounts.

- A Reliable Income Source: Consistent cash flow from your side hustle, 9-to-5, or diverse revenue streams.

- A Budgeting Platform: Tools like YNAB (You Need A Budget), EveryDollar, or a simple Google Sheets template to track your goals.

- Initial Investment: $0 to set up the accounts. You can start funding them with as little as $5.

- Skill Requirements: Basic math and the discipline to automate your transfers.

Time Investment

One of the greatest advantages of sinking funds is that they run in the background, requiring minimal active management once established.

- Setup Time Required: 45 to 60 minutes to audit your upcoming expenses and open the necessary HYSA sub-accounts.

- Daily/Weekly Time Commitment: 5-10 minutes a week to categorize transfers when your digital income deposits hit.

- Timeline to First Results: Most beginners see tangible results in 60-90 days, often the moment their first major quarterly expense (like estimated business taxes or a software subscription) is fully covered without dipping into their main checking account.

- Compared to Traditional Methods: Unlike trying to aggressively hustle for emergency cash when a bill is due, sinking funds spread the pain out over months, making large expenses feel entirely painless.

Step-by-Step Implementation Guide

Step 1: Identify Your “Known” Future Expenses

Write down every large, non-monthly expense you expect over the next 12 months. For an online entrepreneur, this typically includes:

- Quarterly estimated self-employment taxes.

- Annual website hosting, domain renewals, and software subscriptions.

- Equipment upgrades (e.g., a new laptop or camera gear).

- Personal expenses like holiday gifts, car insurance, and vacations.

Step 2: Calculate Your Monthly Target

Take the total cost of each expected expense and divide it by the number of months until the bill is due.

- Example: If your annual web hosting and email marketing software costs $1,200 and is due in 12 months, you need to save $100 per month.

Step 3: Set Up Dedicated “Buckets”

Log into your high-yield savings account and create specific sub-folders or buckets for each category. Naming them specifically (e.g., “Tax Sinking Fund” or “Q4 Inventory Fund”) creates a psychological barrier that prevents you from spending the money on unrelated things.

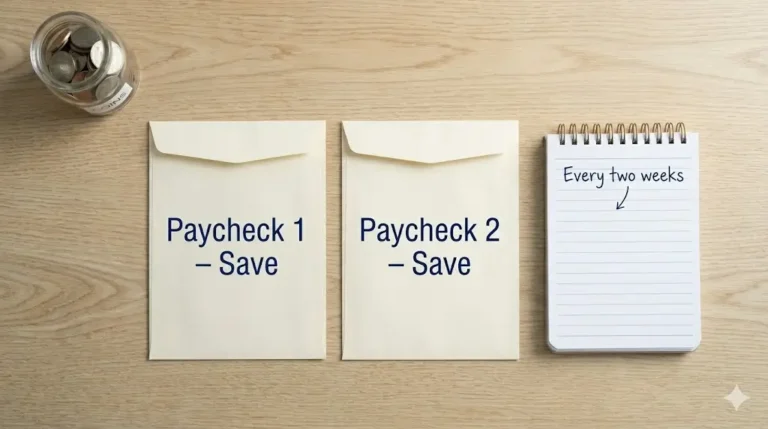

Step 4: Automate Your Revenue Allocation

Set up automatic transfers that align with your payment schedule. If you get paid on the 1st and 15th, schedule a $50 transfer to your software fund on the 2nd and 16th.

- Pro Tip: If your monetization strategies yield variable income, automate a percentage of your earnings (e.g., 25% of all freelance payouts go straight into your tax sinking fund).

Income Potential & Earnings Breakdown

While sinking funds are a defensive financial tool, they directly impact your overall income potential and bottom line. Here is how protecting your cash translates into real money:

- Interest Yields (Passive Income): By storing $5,000 to $10,000 of future expense money in an HYSA earning 4.5% to 5.0% APY, you can generate $200-$500 a year in completely passive interest.

- Avoiding Debt Costs: When a $2,000 equipment failure happens, pulling from a sinking fund saves you from putting it on a credit card at 24% APR—saving you roughly $480 in interest penalties over a year.

- Protecting Profit Margins: Knowing exactly what your future liabilities are allows you to accurately price your services, ensuring your actual profit margins remain intact and aren’t eaten up by “surprise” business expenses.

Alternative Methods & Variations

If managing multiple bank accounts feels overwhelming, there are alternative ways to achieve the same financial stability.

- The Digital Envelope System: Use budgeting software like YNAB to keep all your cash in one single checking/savings account, while the software logically separates the money into digital “envelopes” or sinking funds.

- The Cash Envelope Method: For personal expenses, some people withdraw cash and place it into physical envelopes (e.g., $50 a month into a “Christmas” envelope). Note: Not recommended for large online business expenses.

- Consolidated “Lump” Sinking Fund: Instead of 10 different buckets, group similar expenses into one broader category, such as a single “Digital Asset Maintenance” fund that covers all tech, software, and hosting.

Best Practices & Optimization Tips

To squeeze the maximum benefit out of your sinking funds and elevate your financial stability, implement these optimization strategies:

- Sweep Extra Cash: If a client pays a bonus or your affiliate revenue streams spike unexpectedly, sweep a portion of that windfall directly into your sinking funds to reach your goals faster.

- Regular Audits: Review your sinking funds every quarter. If your software costs increase, adjust your monthly contribution immediately so you aren’t caught off guard.

- Keep Them Liquid: Never invest sinking fund money in the stock market or volatile crypto assets. This cash is meant for short-term stability, not long-term risk. Use HYSAs or Money Market accounts exclusively.

- Combine with Cashback: When it’s time to actually spend the sinking fund money, route the purchase through a cashback credit card (and pay it off instantly with the sinking fund cash) to earn an extra 2-3% back.

Common Mistakes to Avoid

Even seasoned digital creators mess up their cash flow. Avoid these common sinking fund pitfalls:

- Treating It Like an Emergency Fund: A sinking fund is for known expenses (like Christmas or annual taxes). An emergency fund is for unknown disasters (like a medical emergency or sudden job loss). Mixing the two leaves you vulnerable.

- Underfunding Taxes: Over 40% of new freelancers fail to set aside enough for self-employment taxes. Always overestimate your tax sinking fund; if you have money left over after paying the IRS, consider it a bonus.

- “Borrowing” from the Fund: Raiding your “New Laptop” fund to pay for a spontaneous weekend trip destroys the system. Respect the boundaries of your buckets.

Long-Term Sustainability & Growth

Once your core sinking funds are fully operational, you will experience a profound level of financial stability. Here is how to leverage that peace of mind for long-term growth:

- Reinvestment Strategies: When you no longer have to panic about paying upcoming bills, you can confidently reinvest surplus cash back into your business—whether that means hiring a virtual assistant or increasing your ad spend.

- Diversification: Use the stability provided by your sinking funds to safely explore new monetization strategies. Knowing your baseline costs are covered allows you to take calculated risks on new niche sites or product launches.

- Automate and Elevate: As your digital income scales, increase your sinking fund caps to cover business insurance, legal retainers, and larger marketing campaigns, effectively future-proofing your enterprise.

Conclusion

Understanding how sinking funds support financial stability is the secret weapon of successful entrepreneurs. By predicting your expenses, breaking them down into manageable monthly chunks, and automating the savings process, you completely eliminate cash flow anxiety. This proactive approach protects your hard-earned digital income, preserves your profit margins, and gives you the mental clarity needed to focus on scaling your business.

Ready to start your journey to true financial freedom? Drop your questions in the comments below! Tell us which sinking fund you are setting up first. Don’t forget to subscribe for weekly money-making strategies, and share your progress in our community!

FAQs

How much money can I realistically make using this method?

Sinking funds are primarily for capital preservation, but by keeping these funds in a High-Yield Savings Account, beginners can easily generate $100 to $500+ a year in passive interest, while saving hundreds more by avoiding credit card debt.

Do I need prior experience to set up a sinking fund?

No prior experience is necessary. If you can do basic division and log into a bank account, you have all the skills needed to establish a highly effective sinking fund system.

What’s the initial investment?

There is zero initial investment required. You are simply reallocating money you already make into purposeful, segregated accounts.

How long until I see results?

You will feel the psychological relief almost instantly. Financially, the system proves its worth the very first time an annual bill or large expected expense arrives and you can pay it in full without stress (usually within 60-90 days).

Is this method still working in 2026?

Absolutely. In fact, with modern digital banking apps offering automated “bucket” savings features, managing sinking funds is more streamlined and effective than ever before.

What are the risks involved?

The financial risks are zero, provided you keep the funds in FDIC-insured savings accounts. The only risk is human error—specifically, losing discipline and spending the allocated money on impulse purchases rather than its intended purpose.

Before you go, tap those stars!

Straightforward, no gimmicks, just solid banking advice

I clicked on this article expecting it to push some specific bank or financial product with referral links. I was pleasantly surprised. The advice was unbiased, focused on principles rather than promoting any particular institution, and gave me a clear framework to evaluate my own options. I appreciated that the article addressed the importance of FDIC insurance, automatic transfers, and goal-setting — things that seem obvious but that most people (including me) overlook. The writing was clear and concise, without the usual fluff or overly complex financial jargon. The only reason I’m giving four stars instead of five is that I would have liked even more detail on how to balance saving with paying down debt. Still, this was one of the most practical and trustworthy articles on saving I’ve read in a long time. Highly recommend.

Solid advice that cuts through the noise

I’ve been saving for years, but I kept wondering if my money was actually working as hard as it could be. There’s so much conflicting information out there — regular savings accounts, money market accounts, CDs, high-yield options — it gets confusing fast. This article did an excellent job comparing the options side by side, explaining the pros and cons of each, and helping me figure out which strategy made sense for my situation. I especially appreciated the section on the importance of emergency funds versus long-term savings, and the breakdown of how compound interest really adds up over time. I ended up moving my savings to a high-yield account and setting clearer goals. Practical, well-researched, and genuinely helpful.

Small changes, noticeable results

I’ll be honest — I clicked on this article expecting generic advice like “drive less” (thanks, captain obvious). But I was genuinely impressed. The article breaks down the actual science behind why certain habits affect fuel economy, with real numbers to back it up. I learned that my lead-foot acceleration and speeding were costing me way more than I realized. The section on vehicle maintenance was especially valuable — I didn’t know a dirty air filter could impact mileage that much. The tone was straightforward, no fluff, no upselling expensive products. Just solid, practical advice that actually works. My fuel expenses dropped by about 15% last month without me changing my overall driving needs.

Finally, practical advice that doesn’t require buying a new car

As someone who drives over 400 miles a week for work, gas expenses have been crushing my budget. I’ve read countless articles that basically just say “buy an electric vehicle” — which isn’t helpful when that’s not in my budget. This article was a game-changer. The tips were immediately actionable: combining trips, checking tire pressure (I didn’t realize how much that affects mileage!), and using gas price apps. I started implementing these suggestions last month, and I’ve already saved about $40. The writing was clear, well-organized, and respected that not everyone can just trade in their car. Highly recommend for anyone feeling the pain at the pump.

Perfect for renters who can’t install solar panels

As someone who rents an apartment, I often feel limited when it comes to making my home more energy-efficient. I can’t just install new appliances or add insulation to the walls. This article was a lifesaver because it focused on renter-friendly solutions—things like weatherstripping for doors, smart power strips, and optimizing how I use my existing appliances. The writing was straightforward and didn’t assume I owned a home. My only small critique is that I would have loved even more rent-specific examples, but overall, this was incredibly helpful. My electric bill dropped by about $15 last month!