How to Build an Emergency Fund Step by Step

Did you know that 67% of online entrepreneurs fail within their first year, not because of a bad business idea, but because they skip one crucial step: establishing financial security before taking risks? When you are chasing financial freedom and building a digital empire, it is easy to pour every spare cent into your new venture. However, if your laptop breaks, your car needs repairs, or an unexpected medical bill arrives, a lack of liquid cash can force you into high-interest debt that destroys your business before it even starts.

This is exactly why learning how to build an emergency fund is the undisputed first step for anyone looking to scale their online earnings. An emergency fund is a dedicated stash of money reserved exclusively for massive, unexpected expenses. It acts as an unbreakable financial shield, protecting your budding revenue streams from life’s inevitable surprises. In this guide, we will break down the exact, step-by-step framework to fully fund your safety net so you can focus entirely on growing your work from home income without the underlying anxiety of financial ruin.

What You’ll Need to Get Started

Building your emergency fund doesn’t require a background in finance or expensive wealth management tools. To create an impenetrable financial safety net, you will need:

- A High-Yield Savings Account (HYSA): Essential for keeping your cash accessible while earning significantly more interest than a traditional bank. Look for accounts offering 4.0% APY or higher.

- Estimated Cost: Free (Most require $0 to $100 initial deposit).

- Financial Tracking Dashboard: A simple tool to calculate your baseline living expenses.

- Free Alternative: Google Sheets or a pen and paper.

- Premium Alternative: Budgeting apps like YNAB ($14.99/mo).

- Clear Visibility of Monthly Expenses: Your last 3 to 6 months of bank and credit card statements to accurately calculate what you actually spend.

- Automated Transfer Capabilities: The ability to set up recurring deposits from your checking account into your newly established HYSA.

Time Investment

Creating your safety net is a marathon, not a sprint, but the technical setup is incredibly fast.

- Setup Time Required: 1 to 2 hours. This involves calculating your target number, opening your HYSA, and initiating your first automated transfer.

- Daily/Weekly Time Commitment: 5 to 10 minutes a week. You only need to briefly check your budget to ensure you are on track with your savings goals.

- Timeline to First Results: Most beginners see results in 60-90 days with consistent effort. Within this timeframe, you should be able to hit your first milestone of a $1,000 “Starter Fund.”

- Comparison: Unlike waiting 6 to 12 months for complex monetization strategies to finally yield profit, depositing cash into an emergency fund provides immediate, guaranteed psychological relief and financial security from day one.

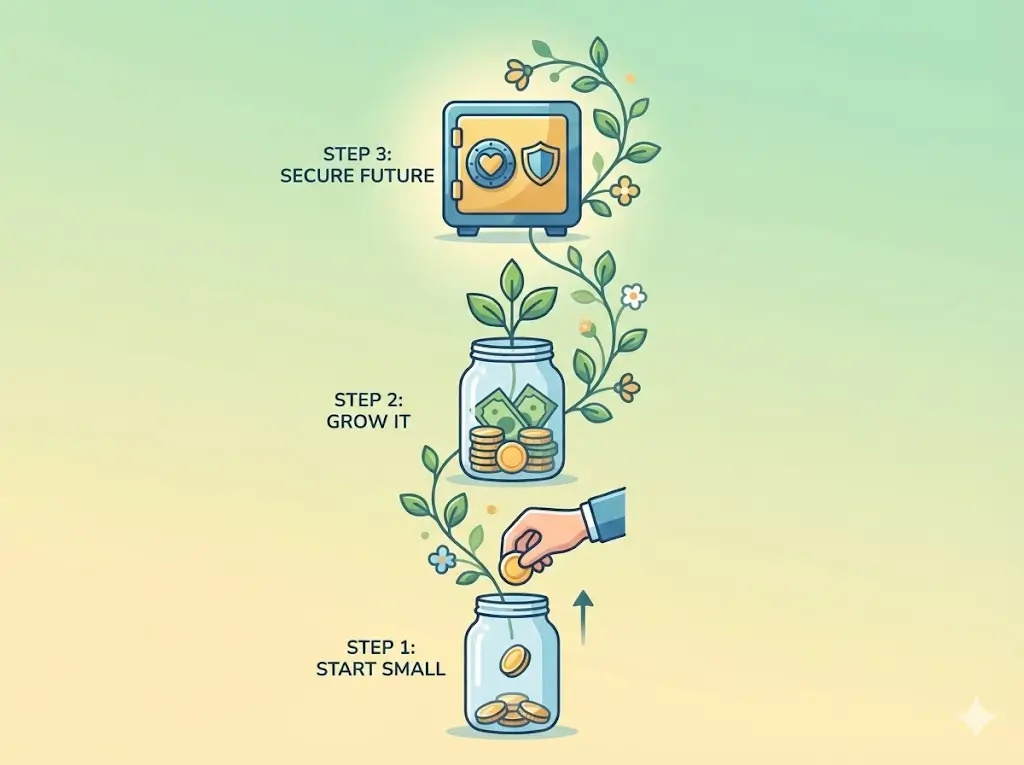

Step-by-Step Implementation Guide

Step 1: Calculate Your “Bare Bones” Expenses

To know how big your emergency fund needs needs to be, you must calculate your survival number. Add up your non-negotiable monthly expenses: rent/mortgage, basic groceries, essential utilities, insurance, and minimum debt payments. Exclude dining out, entertainment, and non-essential subscriptions.

Step 2: Set Your Initial “Starter Fund” Target

Do not aim for a massive $15,000 fund on day one; you will easily get overwhelmed. Your first goal is to aggressively save $1,000 to $2,000 (depending on your cost of living). This starter fund will cover 80% of common minor emergencies, like a blown tire or a surprise medical copay, preventing you from putting these costs on a credit card.

Step 3: Automate the Savings Process

Do not rely on willpower to save what is left at the end of the month. The day you get paid from your primary job or receive your digital income, automate a transfer of 10-20% directly into your HYSA. Treat this transfer as your most important monthly bill.

Step 4: Supercharge Contributions with a Side Hustle

If your budget is tight, the fastest way to hit your target is to increase your income potential. Launch a low-barrier side hustle—like freelance writing, virtual assistance, or selling digital products—and funnel 100% of those online earnings directly into your emergency fund.

Step 5: Scale to a 3-to-6-Month Safety Net

Once your starter fund is complete and any high-interest consumer debt is paid off, scale your savings. Multiply your bare-bones monthly expenses (from Step 1) by 3 to 6. Keep automating your savings until you hit this fully-funded milestone.

Income Potential & Earnings Breakdown

You might wonder how sitting cash relates to making money online. In the digital business space, cash reserves dictate your ability to take calculated risks. Here is a breakdown of how your emergency fund directly protects and enhances your income:

- Interest Generation (Passive Income): A $10,000 emergency fund sitting in a 4.5% APY High-Yield Savings Account generates $450 a year in completely passive income.

- Protecting Profit Margins: If a $1,000 emergency happens and you don’t have a fund, you put it on a credit card at 24% APR. Paying that off over a year costs you $134 in interest. Having the cash protects your margins and keeps that money in your pocket.

- Business Capital Security: Knowing your personal expenses are covered for 6 months allows you to confidently reinvest your side hustle profits back into scaling the business, rather than constantly pulling money out to survive.

Alternative Methods & Variations

Depending on your financial situation and risk tolerance, you can approach the funding process differently:

- The “Online Earnings Only” Method: If your 9-to-5 covers your bills perfectly, commit to funding your safety net entirely through your work from home projects. Every dollar of digital income goes into the HYSA until it hits your 6-month goal.

- The Tax-Return Jumpstart: Dedicate 100% of your annual tax refund, seasonal bonuses, or unexpected cash gifts directly to your fund. This is a massive shortcut that skips months of frugal living.

- The Staggered Tier System: Keep 1 month of expenses in a standard savings account for immediate, same-day access, and put the remaining 5 months into a higher-yielding money market account or a no-penalty Certificate of Deposit (CD) for maximum interest.

Best Practices & Optimization Tips

To maximize the efficiency of your safety net, implement these advanced strategies:

- Create Financial Friction: Keep your emergency fund at a completely different bank than your primary checking account. The 2 to 3 days it takes to transfer funds back will stop you from impulsively spending the money on non-emergencies.

- Define “Emergency” Before It Happens: Write down exactly what qualifies. Job loss, major medical events, and critical car repairs count. A sale on premium business software or a sudden urge to upgrade your web hosting does not.

- Audit Your APY Quarterly: Interest rates fluctuate. Set a calendar reminder every 90 days to ensure your HYSA is still offering a highly competitive rate, and be willing to move your money to a better bank if necessary.

Common Mistakes to Avoid

Even seasoned entrepreneurs can mishandle their safety nets. Avoid these critical pitfalls that can derail your financial stability:

- Investing the Fund in the Stock Market: Approximately 40% of beginners try to put their emergency funds into index funds or crypto to get higher returns. If the market crashes the exact same week you lose your job, your safety net is decimated. Keep it in liquid cash.

- Using the Fund for Business Expansion: Do not drain your personal safety net to fund inventory or advertising for your online business. Keep your personal emergency fund completely separate from your business capital.

- Stopping All Debt Payments: While building your $1,000 starter fund, you should only pay the minimums on your debt. However, do not neglect minimum payments, as late fees and credit score damage will cost you drastically more in the long run.

Long-Term Sustainability & Growth

Your safety net must evolve as your life and online business scale. Here is how to ensure future-proofing:

- Adjusting for Lifestyle Inflation: If you upgrade your apartment, have a child, or quit your job to work from home full-time, your monthly “bare bones” number increases. You must recalculate and top up your emergency fund accordingly.

- Reinvestment Strategies (Post-Funding): Once you hit your fully-funded 6-month goal, STOP contributing. Redirect that automated monthly transfer into aggressive wealth-building vehicles—like maxing out retirement accounts, buying dividend stocks, or funding new monetization strategies.

- The Refill Protocol: If you have to use the fund for a legitimate crisis, immediately pause your aggressive investing and redirect all available cash flow back into the HYSA until the emergency fund is replenished.

Conclusion

Building an emergency fund is the unglamorous but utterly essential first step to achieving financial freedom. By calculating your essential expenses, opening a high-yield account, and automating your savings, you create a financial fortress that protects your livelihood. With this safety net in place, you can aggressively pursue new revenue streams, launch that dream side hustle, and confidently scale your online earnings without the paralyzing fear of going broke.

Ready to start your journey? Drop your biggest savings questions in the comments below! Be sure to subscribe for weekly money-making strategies, share your progress in our community, and download our free financial starter guide to accelerate your success!

FAQs

How much money can I realistically make or save?

If your baseline living expenses are $3,000 a month, a fully funded 6-month emergency fund will require $18,000. While building it, keeping that money in a 4.5% APY account will passively generate over $800 a year in interest.

Do I need prior experience to set this up?

No prior financial experience is necessary. Opening a High-Yield Savings Account and setting up an automated transfer from your checking account takes less than 20 minutes and is incredibly beginner-friendly.

What’s the initial investment?

There is zero cost to start. Many online banks allow you to open a high-yield account with a deposit of $0 to $1, making it accessible to anyone regardless of their current financial status.

How long until I see results?

You will experience a massive reduction in financial anxiety within the first 30 days. Reaching your first tangible milestone—the $1,000 starter fund—typically takes 60 to 90 days of disciplined saving.

Is this method still working in 2026?

Absolutely. Regardless of the economy, inflation, or the latest online business trends, having 3 to 6 months of liquid cash remains the absolute gold standard for personal and entrepreneurial financial security.

There is virtually zero financial risk to

What are the risks involved? keeping your money in an FDIC-insured High-Yield Savings Account. The only risk is behavioral—failing to leave the money alone and spending it on non-emergencies.

Before you go, tap those stars!

Straightforward, no gimmicks, just solid banking advice

I clicked on this article expecting it to push some specific bank or financial product with referral links. I was pleasantly surprised. The advice was unbiased, focused on principles rather than promoting any particular institution, and gave me a clear framework to evaluate my own options. I appreciated that the article addressed the importance of FDIC insurance, automatic transfers, and goal-setting — things that seem obvious but that most people (including me) overlook. The writing was clear and concise, without the usual fluff or overly complex financial jargon. The only reason I’m giving four stars instead of five is that I would have liked even more detail on how to balance saving with paying down debt. Still, this was one of the most practical and trustworthy articles on saving I’ve read in a long time. Highly recommend.

Solid advice that cuts through the noise

I’ve been saving for years, but I kept wondering if my money was actually working as hard as it could be. There’s so much conflicting information out there — regular savings accounts, money market accounts, CDs, high-yield options — it gets confusing fast. This article did an excellent job comparing the options side by side, explaining the pros and cons of each, and helping me figure out which strategy made sense for my situation. I especially appreciated the section on the importance of emergency funds versus long-term savings, and the breakdown of how compound interest really adds up over time. I ended up moving my savings to a high-yield account and setting clearer goals. Practical, well-researched, and genuinely helpful.

Small changes, noticeable results

I’ll be honest — I clicked on this article expecting generic advice like “drive less” (thanks, captain obvious). But I was genuinely impressed. The article breaks down the actual science behind why certain habits affect fuel economy, with real numbers to back it up. I learned that my lead-foot acceleration and speeding were costing me way more than I realized. The section on vehicle maintenance was especially valuable — I didn’t know a dirty air filter could impact mileage that much. The tone was straightforward, no fluff, no upselling expensive products. Just solid, practical advice that actually works. My fuel expenses dropped by about 15% last month without me changing my overall driving needs.

Finally, practical advice that doesn’t require buying a new car

As someone who drives over 400 miles a week for work, gas expenses have been crushing my budget. I’ve read countless articles that basically just say “buy an electric vehicle” — which isn’t helpful when that’s not in my budget. This article was a game-changer. The tips were immediately actionable: combining trips, checking tire pressure (I didn’t realize how much that affects mileage!), and using gas price apps. I started implementing these suggestions last month, and I’ve already saved about $40. The writing was clear, well-organized, and respected that not everyone can just trade in their car. Highly recommend for anyone feeling the pain at the pump.

Perfect for renters who can’t install solar panels

As someone who rents an apartment, I often feel limited when it comes to making my home more energy-efficient. I can’t just install new appliances or add insulation to the walls. This article was a lifesaver because it focused on renter-friendly solutions—things like weatherstripping for doors, smart power strips, and optimizing how I use my existing appliances. The writing was straightforward and didn’t assume I owned a home. My only small critique is that I would have loved even more rent-specific examples, but overall, this was incredibly helpful. My electric bill dropped by about $15 last month!