7 Useful Money Saving Apps to Better Manage Your Finances

Did you know that roughly 67% of online entrepreneurs and digital freelancers fail simply because they skip ONE crucial step? They spend all their energy focusing on generating online earnings, but entirely neglect how to manage, track, and retain that cash. You can scale your side hustle to six figures, but if your personal finances are a leaky bucket, true financial freedom will remain completely out of reach.

That is exactly why leveraging the right money saving apps is the foundational secret to building lasting wealth. Whether you are operating a successful work from home business or just starting to explore digital income, plugging financial leaks gives you the capital needed to invest, scale, and thrive. In this guide, we will break down the top tools to automate your wealth-building journey so you can focus on what matters: growing your revenue streams.

Quick Answer

To optimize your finances quickly, the best money saving apps on the market right now are Monarch Money (best overall dashboard), YNAB (best for zero-based budgeting), and Rocket Money (best for canceling forgotten subscriptions). By linking your accounts to one of these platforms, you can instantly identify wasteful spending and redirect that capital toward high-yield investments or your side hustle.

What You’ll Need to Get Started

Before you start downloading platforms and reorganizing your financial life, you need to gather a few essential items. Setting up a monetization strategy for your savings requires the right toolkit.

- A Smartphone or Desktop Computer: Most platforms are iOS/Android compatible, though some offer powerful web dashboards.

- Active Bank and Credit Card Accounts: You will need your secure login credentials to sync your accounts via secure aggregators like Plaid.

- Initial Investment: Ranging from $0 to around $100 per year. (Free alternatives like Goodbudget exist, while premium tools like YNAB cost ~$109/annually).

- Clear Financial Goals: Know what you are saving for—whether it’s funding a new e-commerce store, building an emergency fund, or investing for passive income.

- 15 Minutes of Undivided Attention: The initial setup requires focus to ensure your transaction categories are accurately tagged.

Time Investment

Building a system to track your profit margins and personal cash flow doesn’t have to be a full-time job. Here is a realistic breakdown of the time required:

- Initial Setup Time: 15 to 30 minutes to download your app of choice, sync your bank accounts, and set baseline budget limits.

- Daily/Weekly Commitment: 5 minutes per day, or roughly 20 minutes a week, to review and categorize new transactions.

- Timeline to First Results: Most beginners see a tangible difference in their bank accounts within 30 to 60 days. In fact, many users report saving their first $200-$500 in the first month just by identifying hidden subscriptions.

Step-by-Step Implementation Guide

Ready to take control of your income potential? Here are the top 7 applications to seamlessly manage your money, along with actionable steps on how to use them effectively.

1. Monarch Money: The All-in-One Wealth Dashboard

Monarch Money has emerged as the premier replacement for older budgeting tools. It offers a comprehensive view of your net worth, allowing you to track checking accounts, credit cards, investments, and even real estate.

- Step 1: Download Monarch and securely link your bank and investment accounts.

- Step 2: Invite your partner (if applicable). Monarch allows dual logins at no extra cost, making it perfect for household financial planning.

- Pro Tip: Use the app’s forecasting feature to project how scaling your side hustle’s revenue streams will impact your long-term net worth.

2. YNAB (You Need A Budget): The Debt Destroyer

YNAB isn’t just an app; it’s a financial philosophy. It relies on zero-based budgeting, meaning you give every single dollar a “job” before you spend it.

- Step 1: Connect your accounts and categorize your current available cash.

- Step 2: Allocate funds to immediate obligations, then to true expenses, and finally to your savings goals.

- Pro Tip: YNAB is strict. It requires active daily participation, making it the best tool for entrepreneurs trying to escape debt and maximize their profit margins.

3. Rocket Money: The Subscription Slayer

Formerly known as Truebill, Rocket Money excels at finding the passive expenses that are quietly draining your accounts.

- Step 1: Sync your primary spending accounts to the platform.

- Step 2: Navigate to the “Recurring” tab and let the app highlight subscriptions you forgot you were paying for.

- Pro Tip: Upgrade to the premium version to let Rocket Money’s team negotiate your internet or phone bills down on your behalf.

4. Piere: The AI-Powered Automator

Piere takes the heavy lifting out of budgeting by using artificial intelligence to analyze your spending and create a budget for you.

- Step 1: Install Piere and let the AI scan your last 90 days of transaction history.

- Step 2: Review the automated budget the AI generates and tweak it to fit your entrepreneurial goals.

- Pro Tip: Use Piere if you suffer from “spreadsheet fatigue.” It learns your habits over time, making it highly hands-off.

5. Cleo: The AI Financial Coach

Cleo caters specifically to Gen Z and Millennials who need a bit of tough love. It operates via a chat interface and will literally “roast” you for poor spending choices.

- Step 1: Connect your accounts and start chatting with the Cleo AI.

- Step 2: Ask Cleo, “Can I afford to buy this coffee?” or “How much have I spent on takeout this month?”

- Pro Tip: Turn on “Roast Mode” to deter impulse purchases, keeping more capital available for your digital income ventures.

6. PocketGuard: The Simplifier

If detailed budgeting overwhelms you, PocketGuard simplifies your finances down to one number: “In My Pocket.”

- Step 1: Input your estimated monthly income and fixed recurring bills.

- Step 2: Let the app calculate your daily, weekly, or monthly disposable cash.

- Pro Tip: Use your “In My Pocket” number as a strict daily limit. Any cash left over at the end of the week should be swept directly into an investment account.

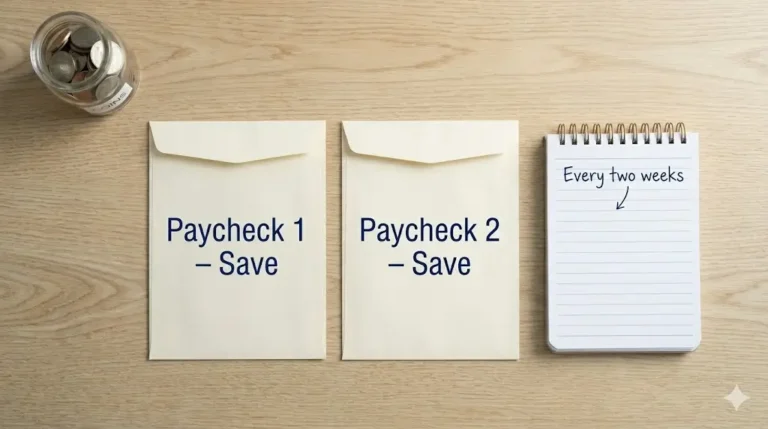

7. Goodbudget: The Digital Envelope System

For those who prefer not to link their bank accounts directly to an app due to security preferences, Goodbudget digitizes the classic “cash envelope” system.

- Step 1: Create virtual envelopes for different categories (Groceries, Tech Subscriptions, Marketing Budget).

- Step 2: Manually log your expenses as they happen to deduct from the virtual envelopes.

- Pro Tip: Manual entry builds incredible psychological awareness of your spending habits, significantly lowering impulse buys.

Income Potential & Earnings Breakdown

While managing your finances doesn’t technically generate new revenue, the savings potential directly mirrors an increase in your income. Remember, a dollar saved is worth more than a dollar earned because it isn’t taxed.

- Beginner Savings Range: $100 – $300 per month (mostly from cutting subscriptions and reducing dining out).

- Intermediate/Advanced Savings Range: $500 – $1,500+ per month (optimizing tax allocations, reducing high-interest debt, negotiating bills).

- The “Hidden Income”: Redirecting $300/month in saved cash into an index fund returning 8% annually creates massive passive income over time, projecting out to over $50,000 in just 10 years.

Disclaimer: Savings and income potential vary wildly based on your starting salary, current debt levels, and overall spending habits.

Alternative Methods & Variations

If you don’t want to rely on a third-party application, there are several alternative approaches to securing your financial foundation:

- The Classic Spreadsheet (Free): Build a custom Google Sheet. It requires more manual labor but offers 100% privacy and infinite customization.

- Bank-Native Tools (Free): Many modern neobanks (like Chime, Revolut, or Current) have built-in budgeting and automated “round-up” savings features that move spare change directly into high-yield accounts.

- The 50/30/20 Rule: Instead of micro-managing categories, simply automate your paycheck so 50% goes to needs, 30% to wants, and 20% to savings/investments.

Best Practices & Optimization Tips

To squeeze the absolute most value out of these tools, follow these advanced optimization strategies:

- Habit Stacking: Check your budgeting app every morning while your coffee is brewing. Tying the task to an existing habit ensures consistency.

- Automate the Savings: The moment you identify $100 in savings, set up an automatic recurring transfer to move that $100 into a brokerage account or separate high-yield savings account on payday.

- Treat Savings Like a Business: Run personal profit and loss (P&L) statements at the end of each month, just as you would for your online business.

Common Mistakes to Avoid

Many people download a money-saving app, use it for three days, and delete it. Here is how to avoid the most common pitfalls:

- Setting Unrealistic Budgets: Going from spending $800 a month on dining out to $50 is a recipe for failure. Trim your expenses gradually.

- Ignoring the “Annual Bills”: Forgetting about yearly subscriptions (like Amazon Prime or web hosting) will derail your monthly averages. Use apps that forecast upcoming annual fees.

- Aiming for Perfection: You will overspend some months. The goal is long-term awareness, not daily perfection. Don’t quit just because you went over budget on a weekend trip.

Long-Term Sustainability & Growth

Once you have plugged the leaks in your finances, the next step is future-proofing your wealth. The ultimate goal of saving money is to deploy that capital into income-producing assets.

- Reinvestment Strategies: Take the money you saved and reinvest it into your side hustle—buy better software, run ads, or hire a virtual assistant.

- Diversification: Do not keep all your saved cash in a standard checking account. Move emergency funds into High-Yield Savings Accounts (HYSAs) and long-term savings into ETFs or real estate.

- Automation: Set your apps to send you weekly progress reports. Automating your financial awareness ensures your digital income actually translates to lasting wealth.

Conclusion

Mastering your personal finances through money saving apps is the ultimate life hack for anyone looking to build true wealth. By utilizing tools like Monarch, YNAB, and Rocket Money, you transform chaotic spending into organized, investable capital. You can’t scale a side hustle or achieve financial freedom if you don’t know where your cash is going.

Ready to start your journey? Drop your questions in the comments below! Let us know which app you are downloading first, and subscribe to our newsletter for weekly strategies on maximizing your digital income.

FAQs

How much money can I realistically save using these apps?

Most beginners realistically save between $100 and $300 in their first month by identifying hidden subscriptions, negotiating bills, and curbing impulse purchases. Over a year, this can equate to thousands of dollars in retained capital.

Do I need prior experience with budgeting?

Not at all. Apps like Piere and Cleo are designed specifically for beginners and use AI to do the heavy lifting for you, categorizing your transactions automatically.

What is the initial investment for these money saving apps?

Many apps offer robust free versions, such as Goodbudget or the basic tier of Rocket Money. Premium apps like Monarch Money or YNAB typically cost between $80 to $110 annually, but usually offer free 7-to-34-day trials.

How long until I see financial results?

You will likely see immediate insights the moment you link your accounts. However, tangible changes to your net worth usually become evident after 60 to 90 days of consistent use.

Are money saving apps safe and secure to use in 2026?

Yes. Top-tier apps use bank-grade encryption and connect to your accounts via secure, read-only aggregators like Plaid or Finicity. They never store your actual bank login credentials on their servers.

Can I use these apps to manage my side hustle income?

Absolutely. Many entrepreneurs use these platforms to track their profit margins, manage estimated tax savings, and keep an eye on total revenue streams alongside their personal finances.

Before you go, tap those stars!

Straightforward, no gimmicks, just solid banking advice

I clicked on this article expecting it to push some specific bank or financial product with referral links. I was pleasantly surprised. The advice was unbiased, focused on principles rather than promoting any particular institution, and gave me a clear framework to evaluate my own options. I appreciated that the article addressed the importance of FDIC insurance, automatic transfers, and goal-setting — things that seem obvious but that most people (including me) overlook. The writing was clear and concise, without the usual fluff or overly complex financial jargon. The only reason I’m giving four stars instead of five is that I would have liked even more detail on how to balance saving with paying down debt. Still, this was one of the most practical and trustworthy articles on saving I’ve read in a long time. Highly recommend.

Solid advice that cuts through the noise

I’ve been saving for years, but I kept wondering if my money was actually working as hard as it could be. There’s so much conflicting information out there — regular savings accounts, money market accounts, CDs, high-yield options — it gets confusing fast. This article did an excellent job comparing the options side by side, explaining the pros and cons of each, and helping me figure out which strategy made sense for my situation. I especially appreciated the section on the importance of emergency funds versus long-term savings, and the breakdown of how compound interest really adds up over time. I ended up moving my savings to a high-yield account and setting clearer goals. Practical, well-researched, and genuinely helpful.

Small changes, noticeable results

I’ll be honest — I clicked on this article expecting generic advice like “drive less” (thanks, captain obvious). But I was genuinely impressed. The article breaks down the actual science behind why certain habits affect fuel economy, with real numbers to back it up. I learned that my lead-foot acceleration and speeding were costing me way more than I realized. The section on vehicle maintenance was especially valuable — I didn’t know a dirty air filter could impact mileage that much. The tone was straightforward, no fluff, no upselling expensive products. Just solid, practical advice that actually works. My fuel expenses dropped by about 15% last month without me changing my overall driving needs.

Finally, practical advice that doesn’t require buying a new car

As someone who drives over 400 miles a week for work, gas expenses have been crushing my budget. I’ve read countless articles that basically just say “buy an electric vehicle” — which isn’t helpful when that’s not in my budget. This article was a game-changer. The tips were immediately actionable: combining trips, checking tire pressure (I didn’t realize how much that affects mileage!), and using gas price apps. I started implementing these suggestions last month, and I’ve already saved about $40. The writing was clear, well-organized, and respected that not everyone can just trade in their car. Highly recommend for anyone feeling the pain at the pump.

Perfect for renters who can’t install solar panels

As someone who rents an apartment, I often feel limited when it comes to making my home more energy-efficient. I can’t just install new appliances or add insulation to the walls. This article was a lifesaver because it focused on renter-friendly solutions—things like weatherstripping for doors, smart power strips, and optimizing how I use my existing appliances. The writing was straightforward and didn’t assume I owned a home. My only small critique is that I would have loved even more rent-specific examples, but overall, this was incredibly helpful. My electric bill dropped by about $15 last month!