Money Saving Expert Remortgage Guide: How to Lower Your Rate

Did you know that over 60% of homeowners overpay on their property by thousands of dollars a year simply because they let their introductory fixed rate expire? When building wealth, many aspiring entrepreneurs focus entirely on generating new revenue streams, completely ignoring the massive capital leaks right over their heads. If you are serious about achieving financial freedom, executing a Money Saving Expert remortgage strategy is the most crucial, immediate step you can take. Every dollar you cut from your highest monthly expense is a dollar added directly to your personal profit margins, providing the exact seed money you need to fund a new side hustle or online business.

Quick Answer

A Money Saving Expert remortgage strategy involves actively switching your mortgage to a better deal before your current fixed or discounted rate ends. By securing a lower interest rate and avoiding your lender’s expensive Standard Variable Rate (SVR), you instantly reduce your monthly outgoings, freeing up hundreds of dollars in capital that you can reinvest into passive income streams or digital earnings.

What You’ll Need to Get Started

Optimizing your mortgage is essentially the highest-yield work from home task you can complete. You don’t need to be a financial advisor, but you do need to gather some specific data before you start comparing rates.

Required Tools & Resources:

- Your Current Mortgage Statement: You need your current interest rate, outstanding balance, and your exact end date for any introductory offers.

- Credit Report Access: Free platforms like Credit Karma or Experian to ensure your credit score is in top shape before lenders check it.

- Property Valuation Estimate: A rough estimate of your home’s current market value (Zillow or Zoopla can give a baseline) to calculate your Loan-to-Value (LTV) ratio.

- A Whole-of-Market Broker (Optional but Recommended): Many mortgage brokers are completely free to the consumer (they get paid a commission by the bank).

Initial Investment Breakdown:

- Estimated Cost: $0.00 / £0.00 to research and apply (though some specific mortgage products have arrangement fees that can be added to the loan).

- Skill Requirements: Basic organization and a willingness to make a few phone calls or fill out online forms.

Time Investment

Unlike building a blog, launching a YouTube channel, or creating a digital product—which can take months or years to yield high returns—optimizing your mortgage provides a massive, immediate return on the time invested.

- Setup Time Required: 2 to 3 hours to gather documents and speak with a broker or run an online comparison.

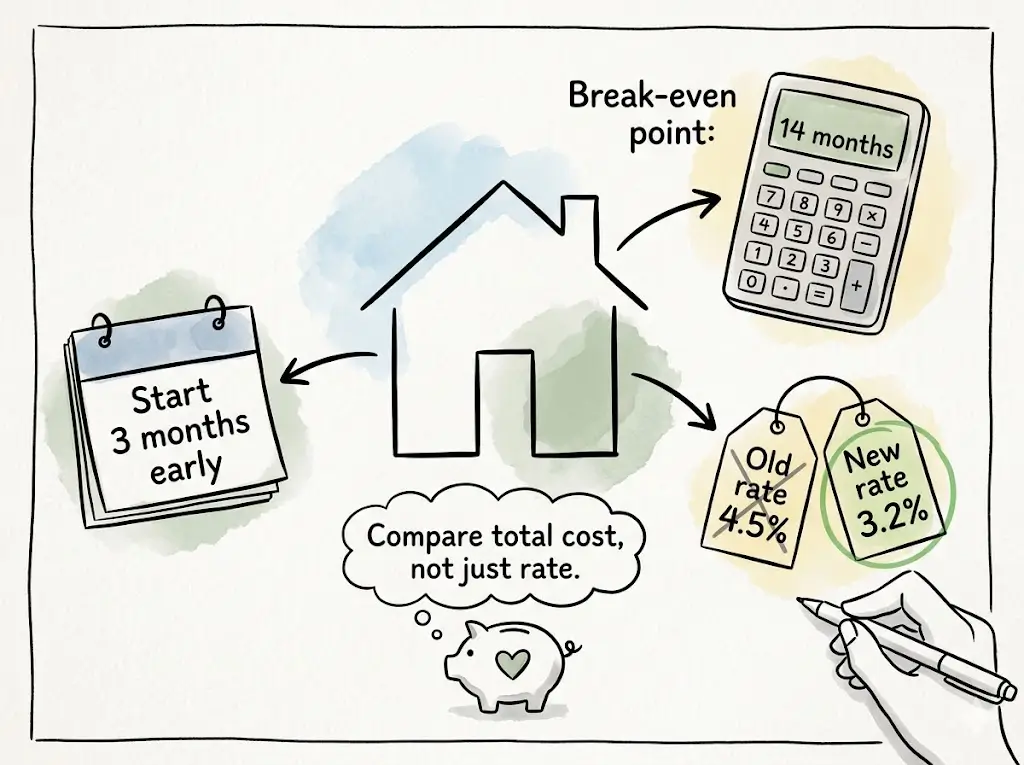

- Timeline to First “Earnings”: The legal and underwriting process takes roughly 4 to 8 weeks. However, you should start the process 3 to 6 months before your current deal ends to lock in a rate.

- Comparison: Building an online earnings portfolio that generates $400 a month in profit takes significant time and marketing effort. Spending 3 hours to remortgage and save $400 a month on interest achieves the exact same impact on your cash flow, instantly.

Step-by-Step Implementation Guide

Step 1: Calculate Your Loan-to-Value (LTV) Ratio

Your LTV dictates the rates you can access. If your home is worth $300,000 and your mortgage is $150,000, your LTV is 50%. The lower your LTV (usually anything under 60%), the better the interest rates available to you.

Step 2: Check for Early Repayment Charges (ERCs)

Before you switch, check your current contract. If you leave your current fixed deal too early, you may face ERCs that cost thousands, wiping out any potential savings. Always time your remortgage to complete exactly when your current penalty period expires.

Step 3: Compare the Market

Use an online Money Saving Expert remortgage comparison tool to look at the current landscape. Look at the total cost of the mortgage over the fixed period (e.g., 2 or 5 years)—including any arrangement fees—not just the headline interest rate.

Step 4: Consult a Free, Whole-of-Market Broker

While you can go direct to a bank, a broker has access to exclusive deals and can tell you exactly which lenders are most likely to approve your specific financial situation (especially crucial if your income potential relies on freelance or self-employed online earnings).

Step 5: Lock in Your Rate Early

You can typically secure a mortgage offer 3 to 6 months in advance. If rates go up, you are protected. If rates drop before your completion date, a good broker can simply cancel the first offer and apply for the new, lower rate.

Income Potential & Earnings Breakdown

When you implement a strategic remortgage, the financial impact is staggering. Think of these savings as tax-free income potential that you can directly reinvest into monetization strategies.

Here is a realistic look at how falling onto an SVR versus remortgaging impacts your “profit margins” (Based on a $250,000 mortgage over 25 years):

| Mortgage Strategy | Interest Rate | Monthly Payment | Monthly “Profit” Created | Annual Capital Saved |

|---|---|---|---|---|

| Standard Variable Rate (SVR) | 7.5% | $1,847 | $0 (Baseline) | $0 |

| Average 2-Year Fix | 5.5% | $1,535 | **$312** | $3,744 |

| Optimized 5-Year Fix (Low LTV) | 4.5% | $1,389 | **$458** | $5,496 |

Note: Interest rates and payments are illustrative. Your actual savings will vary based on market conditions and your outstanding balance.

Alternative Methods & Variations

If a full remortgage to a new lender seems too complex, there are alternative methods to optimize your property debt:

- The Product Transfer: Instead of changing banks, you simply switch to a new rate with your current lender. This usually requires zero legal work, no new credit checks, and takes about 10 minutes online. The rates might be slightly higher than the open market, but it is infinitely better than paying the SVR.

- Offset Mortgages: If you hold a lot of cash (perhaps from a successful digital income stream), an offset mortgage links your savings to your mortgage. If you have a $200,000 mortgage and $50,000 in savings, you only pay interest on $150,000.

- Overpaying for Guaranteed Returns: If you have secured a great rate but still want to optimize, overpaying your mortgage by just 10% a month is a guaranteed, tax-free return on investment that saves tens of thousands in interest over the life of the loan.

Best Practices & Optimization Tips

To maximize your results and accelerate your path to financial autonomy, follow these optimization hacks:

- Clean Up Your Bank Statements: Three months before applying, treat your personal finances like a strict business. Cut unnecessary subscriptions and avoid dipping into your overdraft. Lenders will heavily scrutinize your affordability.

- Don’t Apply for New Credit: Never apply for a new credit card, car loan, or business financing in the 6 months leading up to a remortgage. It temporarily dings your credit score.

- Value Your Home Strategically: If doing a minor cosmetic repair (like painting or landscaping) pushes your home’s valuation into a lower LTV bracket (e.g., from 61% down to 59%), it could unlock significantly cheaper interest rates.

Common Mistakes to Avoid

Even seasoned homeowners fall into common financial traps. Avoid these pitfalls to protect your bottom line:

- Apathy and the SVR Trap: The biggest mistake is doing nothing. Lenders rely on customer apathy. When your fixed rate ends, you are automatically moved to the SVR, which is often 2% to 4% higher than competitive rates.

- Focusing Only on the Interest Rate: A mortgage with a 4.1% rate and a $2,000 upfront fee might actually be more expensive over 2 years than a mortgage with a 4.3% rate and zero fees. Always calculate the total cost over the fixed term.

- Leaving it Too Late: Waiting until the week your current deal expires to start shopping around guarantees you will spend at least a month or two overpaying on the SVR while the new legal paperwork is processed.

Long-Term Sustainability & Growth

Finding the best Money Saving Expert remortgage deal is only half the equation; what you do with the saved money dictates your long-term wealth. To future-proof your finances, you must adopt a reinvestment strategy.

When you secure a new, lower payment, do not let lifestyle creep consume the difference. If your mortgage drops by $400 a month, immediately set up an automated transfer to funnel that $400 into income-generating assets.

Use this capital to fund your freelance business, invest in dividend-paying index funds, pay for premium software tools for your side hustle, or build a scalable e-commerce brand. By turning your debt reduction into a revenue generation tool, you build a sustainable loop of passive income.

Conclusion

Securing your financial baseline is the prerequisite to successfully building sustainable online earnings. By utilizing a Money Saving Expert remortgage strategy, you eliminate the single largest capital leak in your personal finances. You aren’t just lowering an interest rate; you are systematically buying back your own capital to fund your future wealth.

Ready to start your journey to financial freedom? Let us know how much you are aiming to save on your next remortgage in the comments below! Don’t forget to subscribe for more weekly strategies on maximizing your profit margins, and share your wealth-building progress in our community forums!

FAQs

1. How much money can I realistically save by remortgaging?

Depending on your loan size and how far interest rates have moved, homeowners routinely save anywhere from $200 to $600+ a month by avoiding their lender’s standard variable rate (SVR) and securing a new fixed deal.

2. Do I need prior financial experience to find a good deal?

No prior experience is necessary. Using a free, whole-of-market mortgage broker allows an expert to do the heavy lifting, analyze your credit, and match you with the best available products.

3. What’s the initial investment to remortgage?

While researching and using a broker is often free, some mortgage products come with arrangement or booking fees (ranging from $0 to $2,000+). You must weigh these fees against the monthly savings to ensure it is a profitable switch.

4. How long until I see results?

If you lock in a rate 3 to 6 months before your current deal expires, your new, lower payment will seamlessly take effect the exact month your old deal ends, resulting in immediate cash-flow improvements.

5. Is remortgaging to fund a side hustle a safe strategy?

Taking equity out of your home to fund a business is highly risky. However, simply remortgaging to secure a lower interest rate and using the monthly savings to fund a side hustle is a highly secure, data-driven wealth strategy.

6. What are the risks involved in remortgaging?

The main risks include paying early repayment charges (ERCs) if you switch too early, or locking into a long-term fixed rate just before market interest rates drop significantly.

Before you go, tap those stars!

Straightforward, no gimmicks, just solid banking advice

I clicked on this article expecting it to push some specific bank or financial product with referral links. I was pleasantly surprised. The advice was unbiased, focused on principles rather than promoting any particular institution, and gave me a clear framework to evaluate my own options. I appreciated that the article addressed the importance of FDIC insurance, automatic transfers, and goal-setting — things that seem obvious but that most people (including me) overlook. The writing was clear and concise, without the usual fluff or overly complex financial jargon. The only reason I’m giving four stars instead of five is that I would have liked even more detail on how to balance saving with paying down debt. Still, this was one of the most practical and trustworthy articles on saving I’ve read in a long time. Highly recommend.

Solid advice that cuts through the noise

I’ve been saving for years, but I kept wondering if my money was actually working as hard as it could be. There’s so much conflicting information out there — regular savings accounts, money market accounts, CDs, high-yield options — it gets confusing fast. This article did an excellent job comparing the options side by side, explaining the pros and cons of each, and helping me figure out which strategy made sense for my situation. I especially appreciated the section on the importance of emergency funds versus long-term savings, and the breakdown of how compound interest really adds up over time. I ended up moving my savings to a high-yield account and setting clearer goals. Practical, well-researched, and genuinely helpful.

Small changes, noticeable results

I’ll be honest — I clicked on this article expecting generic advice like “drive less” (thanks, captain obvious). But I was genuinely impressed. The article breaks down the actual science behind why certain habits affect fuel economy, with real numbers to back it up. I learned that my lead-foot acceleration and speeding were costing me way more than I realized. The section on vehicle maintenance was especially valuable — I didn’t know a dirty air filter could impact mileage that much. The tone was straightforward, no fluff, no upselling expensive products. Just solid, practical advice that actually works. My fuel expenses dropped by about 15% last month without me changing my overall driving needs.

Finally, practical advice that doesn’t require buying a new car

As someone who drives over 400 miles a week for work, gas expenses have been crushing my budget. I’ve read countless articles that basically just say “buy an electric vehicle” — which isn’t helpful when that’s not in my budget. This article was a game-changer. The tips were immediately actionable: combining trips, checking tire pressure (I didn’t realize how much that affects mileage!), and using gas price apps. I started implementing these suggestions last month, and I’ve already saved about $40. The writing was clear, well-organized, and respected that not everyone can just trade in their car. Highly recommend for anyone feeling the pain at the pump.

Perfect for renters who can’t install solar panels

As someone who rents an apartment, I often feel limited when it comes to making my home more energy-efficient. I can’t just install new appliances or add insulation to the walls. This article was a lifesaver because it focused on renter-friendly solutions—things like weatherstripping for doors, smart power strips, and optimizing how I use my existing appliances. The writing was straightforward and didn’t assume I owned a home. My only small critique is that I would have loved even more rent-specific examples, but overall, this was incredibly helpful. My electric bill dropped by about $15 last month!