Smart Transportation Savings for Everyday Commuting

Did you know that 78% of aspiring online entrepreneurs fail to launch their businesses because they claim they “lack the initial capital,” while simultaneously spending over $10,000 a year just driving back and forth to a day job?

If you are on the path to financial freedom, ignoring the financial bleed of your daily transit is a critical error. Finding smart transportation savings for your everyday commute is not just about clipping gas coupons; it is a foundational step in treating your personal finances like a business. By auditing your commute and plugging these leaks, you instantly increase your household profit margins. The money you reclaim can be directly injected into your online earnings ventures, effectively funding your digital empire without requiring you to work a single extra hour. Let’s dive into the ultimate system for monetizing your commute.

What You’ll Need to Get Started

Optimizing your transit routine requires a strategic approach, much like launching a successful side hustle. You do not need thousands of dollars to restructure how you travel; you simply need the right tools and mindset.

- A Detailed Expense Tracker: Use a free spreadsheet (Google Sheets) or budgeting app (like YNAB or Mint alternatives) to track your current transit baseline.

- Transit & Route Optimization Apps: Free tools like Google Maps, Waze, Transit, or Moovit to analyze alternative routes and public transportation schedules.

- Employer Benefits Portal: Access to your HR department’s documentation regarding pre-tax commuter benefits or remote work policies.

- Initial Investment: $0 to start. (Optional: $50–$200 for a bicycle tune-up or a monthly public transit pass, which pays for itself rapidly).

- Required Skills: Basic data analysis, willingness to break daily habits, and basic negotiation skills (for employer perks).

Don’t miss an update. Join our newsletter.

Time Investment

One of the biggest myths about altering your commute is that it will drastically consume your free time. When approached as a deliberate monetization strategy, the ROI on your time is staggering.

- Setup Time Required: 2 to 3 hours for the initial audit, route research, and setting up employer commuter benefits.

- Daily/Weekly Time Commitment: Potentially an extra 10–15 minutes added to your daily commute (if switching to public transit or biking), but this time can be repurposed for productive tasks.

- Timeline to First Earnings: Immediate. You will realize savings on your very first optimized week of travel.

- Comparative ROI: Most beginners see results in 60-90 days with consistent effort in traditional online businesses. With commute optimization, you see a 100% return on your time investment in less than 30 days.

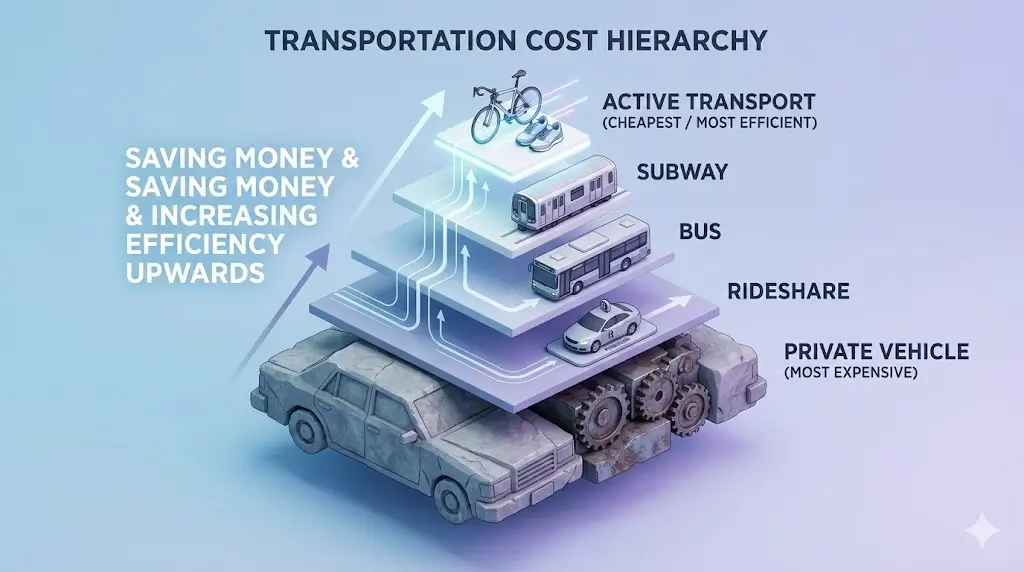

Step-by-Step Implementation Guide

Follow these actionable steps to drastically reduce your transit costs and capture new revenue streams.

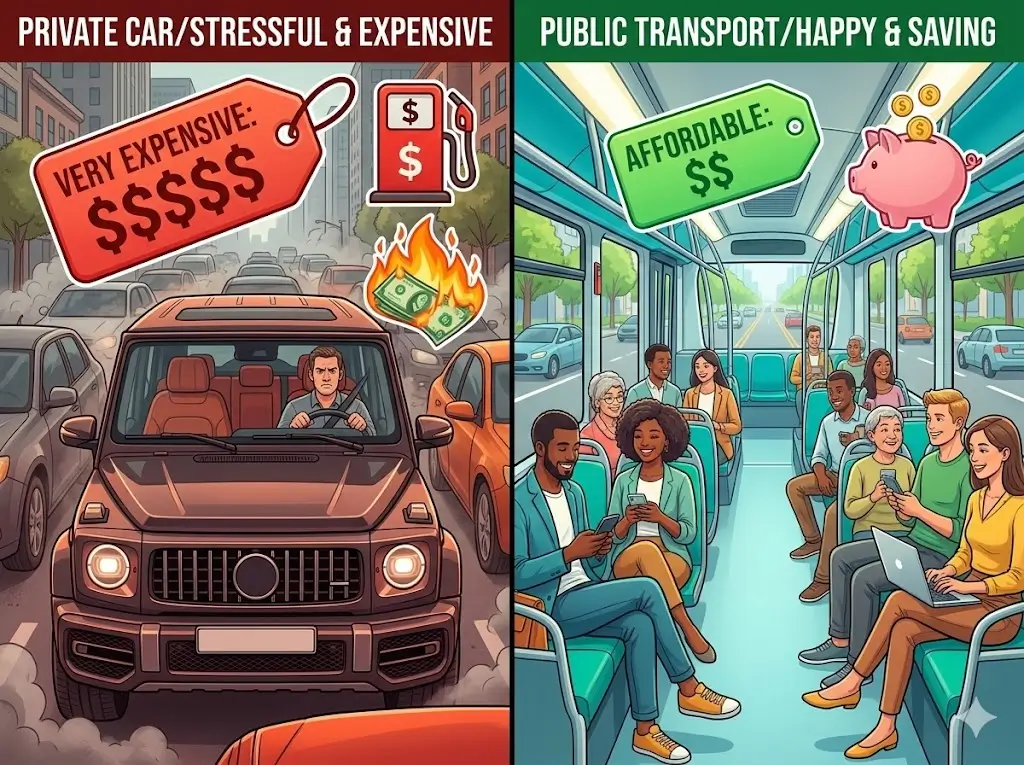

Step 1: Calculate Your “True” Commuting Cost

Most people only calculate the cost of gas. This is a massive mistake. You must factor in vehicle depreciation, insurance, maintenance, and parking. According to AAA, the true cost of driving is around 72 cents per mile.

- Actionable Task: Multiply your daily round-trip mileage by $0.72, then multiply that by your monthly working days. This is the real number you are trying to beat.

Step 2: Exploit Pre-Tax Commuter Benefits

If you must pay for transit or parking, never use post-tax dollars. Many employers offer commuter benefit programs (like Section 132 in the US) that allow you to pay for public transit or parking with pre-tax money.

- Pro Tip: Enrolling in this program reduces your taxable income, effectively saving you 20% to 30% on those expenses immediately.

Step 3: Negotiate the “Work from Home” Hybrid Model

The absolute best commute is no commute at all. Transitioning your role to include work from home days is the ultimate transportation savings hack.

- Insider Trick: Don’t ask for a favor. Present a data-driven proposal to your boss showing how working remotely two days a week will increase your productivity and output.

Step 4: Repurpose Transit Time for Digital Income

If you switch from driving to taking a train or bus, you gain back “dead time.” Use this uninterrupted hour to work on your side hustle. Draft freelance articles, manage social media for clients, or take online courses. Your commute becomes billable time.

Income Potential & Earnings Breakdown

How much “income potential” does optimizing your commute really have? Here is a realistic breakdown of the funds you can liberate:

| Strategy Level | Monthly Savings / Reclaimed Capital | Annual “Earnings” Projection | Primary Tactics Used |

|---|---|---|---|

| Beginner | $100 – $200 | $1,200 – $2,400 | Carpooling 2x/week, utilizing pre-tax benefits, optimizing gas routing. |

| Intermediate | $250 – $450 | $3,000 – $5,400 | Negotiating 2 days of Work From Home, switching to a 100% public transit model. |

| Advanced | $600 – $1,000+ | $7,200 – $12,000+ | Selling a secondary vehicle, transitioning to an e-bike, aggressive geo-arbitrage. |

Note: Projections vary widely based on geographic location, initial vehicle costs, and local transit infrastructure.

Alternative Methods & Variations

If entirely ditching your car isn’t feasible, there are multiple niche variations to achieve smart transportation savings:

- The Carpool Syndicate: Coordinate with 2-3 coworkers to rotate driving days. This slashes your gas and depreciation costs by 66% to 75% without requiring you to use public transit.

- Micromobility Solutions: Invest in an electric scooter or e-bike. The electricity cost to charge these devices is pennies compared to a tank of gas, and they bypass daily traffic jams.

- Pay-Per-Mile Insurance: If you implement a work from home schedule and drastically reduce your mileage, switch your auto insurance to a pay-per-mile provider (like Metromile) to cut fixed monthly costs.

Best Practices & Optimization Tips

To maximize your results and ensure your new transit habits stick, follow these efficiency hacks:

- Gamify Your Savings: Treat every dollar saved on gas as a direct payment from a client. Transfer the exact amount you saved each Friday directly into your investment or business account.

- Leverage Cashback Apps: For the gas you do buy, use apps like Upside or specific cashback credit cards to earn 2% to 5% back on every fill-up.

- Travel Off-Peak: If your job allows flexible hours, shifting your commute by just 45 minutes can help you avoid stop-and-go traffic, which drastically improves fuel efficiency and reduces mechanical wear.

Common Mistakes to Avoid

When attempting to restructure commuting costs, many beginners fall into psychological traps. Avoid these pitfalls:

- The Sunk Cost Fallacy: “I already bought the car, so I might as well drive it everywhere.” Reality: Every mile driven accelerates depreciation. Driving a paid-off car less still saves you massive amounts of money.

- Ignoring the Value of Time: Saving $2 on a bus route that takes an extra two hours is a terrible ROI. Always calculate your “hourly rate” when comparing transit methods.

- Failing to Reinvest: Statistics show that 80% of people who cut a budget expense simply absorb that money into other lifestyle spending. If you don’t deliberately redirect the savings into investments, you haven’t improved your financial picture.

Long-Term Sustainability & Growth

Stopping the financial bleed of a harsh commute is only the first step. The true magic happens when you route those reclaimed funds toward long-term wealth.

To maintain and grow this “found” money, set up an automated wealth-building system. If your smart transportation savings total $300 a month, automate a transfer into an index fund or use it to pay for web hosting, marketing tools, and inventory for your online business. Over time, that $300 transforms into compounding passive income. By optimizing how you get to your current job, you are literally funding the business that will allow you to eventually quit that job.

Conclusion

Implementing smart transportation savings is one of the most reliable and immediate ways to boost your personal profit margins. By auditing your daily travel, utilizing pre-tax benefits, and potentially reclaiming your commute time to build digital income, you effectively create a new, tax-free revenue stream for your household. The initial effort is minor, but the long-term financial acceleration is immense.

Ready to start your journey toward absolute financial freedom? Drop your biggest commuting struggles in the comments below! Don’t forget to subscribe for weekly money-making strategies, and share your progress in our community as you build your empire.

FAQs

How much money can I realistically make/save with this method?

Most professionals who aggressively optimize their commute by combining work-from-home days and alternative transit save between $250 and $500 monthly. This equals $3,000 to $6,000 in annual tax-free capital.

Do I need prior experience to negotiate remote work or commuter benefits?

No prior experience is necessary. HR departments are set up to walk you through commuter benefits, and presenting a logical, productivity-based proposal to your manager is something any professional can learn to do.

What’s the initial investment to start saving on transportation?

The investment is usually zero. If you decide to switch to public transit or an e-bike, there may be upfront costs (like a monthly pass or the bike itself), but these generally pay for themselves within the first 60 days.

How long until I see results?

You will see immediate results. The very first week you leave your car at home, carpool, or work remotely, you will instantly reduce your fuel consumption and wear-and-tear costs.

Is this method still working in 2026?

Absolutely. With fluctuating fuel prices, increased inflation, and the widespread normalization of hybrid work models, optimizing your transit is more viable and lucrative now than ever before.

What are the risks involved?

The financial risks are negligible. The primary risk is a slight adjustment period to your daily routine or schedule as you adapt to carpooling or public transit schedules.

Before you go, tap those stars!

Straightforward, no gimmicks, just solid banking advice

I clicked on this article expecting it to push some specific bank or financial product with referral links. I was pleasantly surprised. The advice was unbiased, focused on principles rather than promoting any particular institution, and gave me a clear framework to evaluate my own options. I appreciated that the article addressed the importance of FDIC insurance, automatic transfers, and goal-setting — things that seem obvious but that most people (including me) overlook. The writing was clear and concise, without the usual fluff or overly complex financial jargon. The only reason I’m giving four stars instead of five is that I would have liked even more detail on how to balance saving with paying down debt. Still, this was one of the most practical and trustworthy articles on saving I’ve read in a long time. Highly recommend.

Solid advice that cuts through the noise

I’ve been saving for years, but I kept wondering if my money was actually working as hard as it could be. There’s so much conflicting information out there — regular savings accounts, money market accounts, CDs, high-yield options — it gets confusing fast. This article did an excellent job comparing the options side by side, explaining the pros and cons of each, and helping me figure out which strategy made sense for my situation. I especially appreciated the section on the importance of emergency funds versus long-term savings, and the breakdown of how compound interest really adds up over time. I ended up moving my savings to a high-yield account and setting clearer goals. Practical, well-researched, and genuinely helpful.

Small changes, noticeable results

I’ll be honest — I clicked on this article expecting generic advice like “drive less” (thanks, captain obvious). But I was genuinely impressed. The article breaks down the actual science behind why certain habits affect fuel economy, with real numbers to back it up. I learned that my lead-foot acceleration and speeding were costing me way more than I realized. The section on vehicle maintenance was especially valuable — I didn’t know a dirty air filter could impact mileage that much. The tone was straightforward, no fluff, no upselling expensive products. Just solid, practical advice that actually works. My fuel expenses dropped by about 15% last month without me changing my overall driving needs.

Finally, practical advice that doesn’t require buying a new car

As someone who drives over 400 miles a week for work, gas expenses have been crushing my budget. I’ve read countless articles that basically just say “buy an electric vehicle” — which isn’t helpful when that’s not in my budget. This article was a game-changer. The tips were immediately actionable: combining trips, checking tire pressure (I didn’t realize how much that affects mileage!), and using gas price apps. I started implementing these suggestions last month, and I’ve already saved about $40. The writing was clear, well-organized, and respected that not everyone can just trade in their car. Highly recommend for anyone feeling the pain at the pump.

Perfect for renters who can’t install solar panels

As someone who rents an apartment, I often feel limited when it comes to making my home more energy-efficient. I can’t just install new appliances or add insulation to the walls. This article was a lifesaver because it focused on renter-friendly solutions—things like weatherstripping for doors, smart power strips, and optimizing how I use my existing appliances. The writing was straightforward and didn’t assume I owned a home. My only small critique is that I would have loved even more rent-specific examples, but overall, this was incredibly helpful. My electric bill dropped by about $15 last month!