The 50/30/20 Rule Explained for Smart Saving

Did you know that 67% of online entrepreneurs fail because they skip this ONE crucial step? Before you can successfully build a lucrative side hustle or scale your online earnings, you need a rock-solid financial foundation. This is where smart saving comes into play. Most beginners rush into creating digital income without learning how to manage the money they already have.

If you want to achieve true financial freedom, you need a system that balances your current lifestyle with your future goals. The 50/30/20 rule is that system. It is a simple, intuitive, and highly effective budgeting method that helps you allocate your funds without feeling restricted. Whether you are working a traditional 9-to-5 or building a work from home empire, mastering smart saving through this framework is the ultimate prerequisite for long-term wealth. Let’s dive into how this rule works and how it can fund your next big venture.

What You’ll Need to Get Started

Implementing the 50/30/20 rule doesn’t require a degree in finance. To begin your smart saving journey and lay the groundwork for future passive income, you only need a few basic resources:

- Financial Tracking Tool: A spreadsheet (Google Sheets or Excel) or a budgeting app (like YNAB, EveryDollar, or Rocket Money). Cost: Free to $15/month.

- Recent Bank Statements: Last 30 to 90 days of income and expenses to establish your baseline.

- A Dedicated “Wealth” Account: A High-Yield Savings Account (HYSA) or a low-cost brokerage account to park your 20% savings. Cost: Free (often requires a minimum deposit of $1 to $100).

- Clear Income Visibility: An exact calculation of your net (after-tax) monthly income, including any existing revenue streams.

- Discipline and Consistency: The most critical (and completely free) requirement for success.

Don’t miss an update. Join our newsletter.

Time Investment

One of the best things about the 50/30/20 method is that it requires very little active management once established.

- Setup Time Required: 1 to 2 hours. This involves reviewing your past statements, categorizing your expenses, and setting up automated transfers.

- Daily/Weekly Time Commitment: 15 to 30 minutes a week. You only need to check in on your categories to ensure you aren’t overspending.

- Timeline to First Results: Most beginners see a complete transformation in their financial clarity within 60-90 days with consistent effort.

- Comparison: Unlike building complex monetization strategies from scratch which can take months to yield a profit, the financial relief and capital generation from smart saving begins the very first month you implement it.

Step-by-Step Implementation Guide

Step 1: Calculate Your After-Tax Income

Before you can divide your money, you need to know exactly how much you have. Look at your paychecks and tally up your net income. If you already have online earnings or a side hustle, calculate your average monthly profit after setting aside estimated taxes.

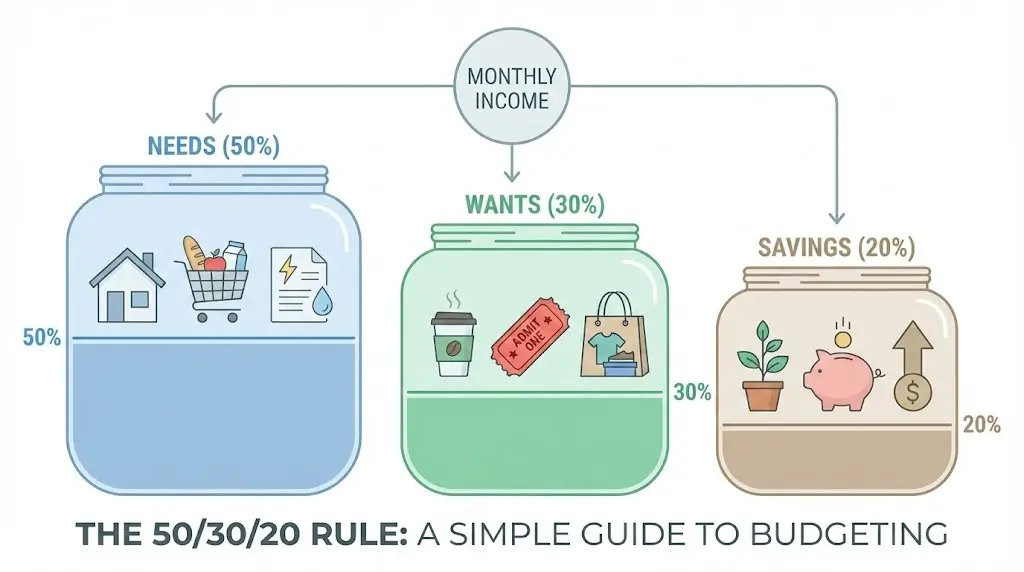

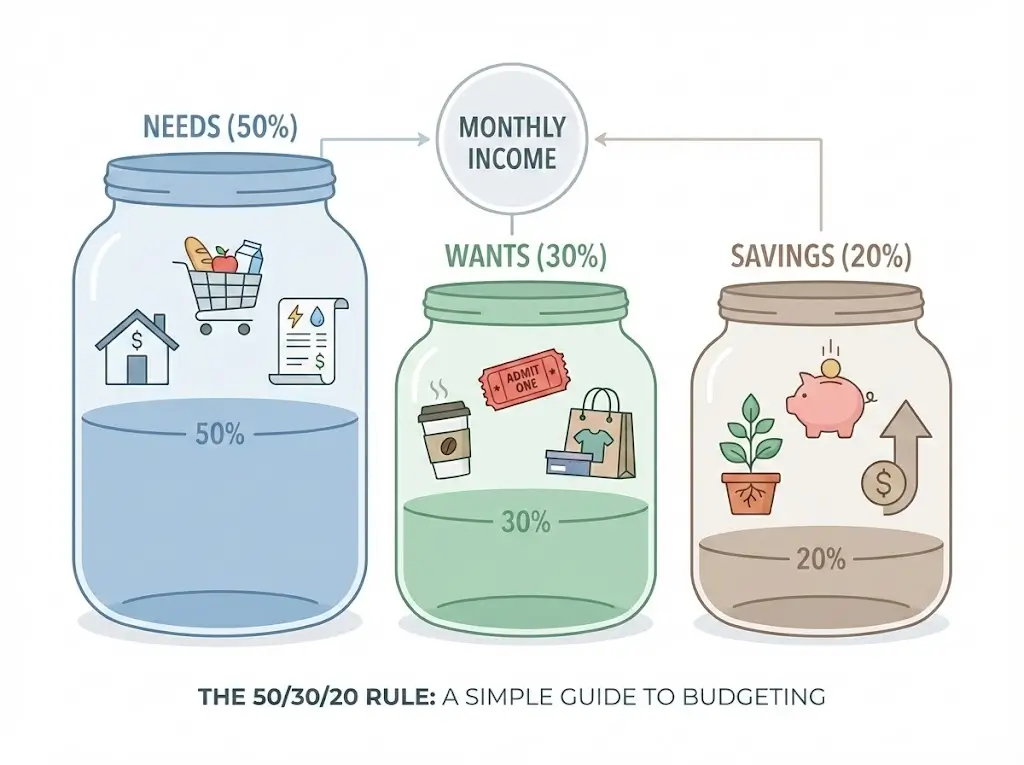

Step 2: Limit Your “Needs” to 50%

Half of your income should go toward essential living expenses. These are the bills you absolutely must pay to survive and keep your job.

- Includes: Rent/mortgage, groceries, basic utilities, minimum debt payments, and healthcare.

- Pro Tip: If your needs exceed 50%, you may need to look into downsizing, negotiating bills, or accelerating your digital income to increase the overall pie.

Step 3: Restrict Your “Wants” to 30%

This is the category that makes the 50/30/20 rule sustainable. You get to enjoy your life!

- Includes: Dining out, entertainment, subscriptions, hobbies, and vacations.

- Insider Trick: To maximize this category, look for free or low-cost alternatives to your usual entertainment. This keeps your quality of life high while keeping costs low.

Step 4: Commit 20% to Smart Saving and Investments

This is the engine of your financial freedom. Exactly 20% of your net income must be funneled into wealth-building vehicles.

- Includes: Emergency funds, retirement accounts, aggressive debt payoff (beyond the minimums), and seed capital for your online business.

- Actionable Advice: Treat this 20% as a non-negotiable bill. Pay your “future self” first before spending on wants.

Step 5: Automate for Financial Freedom

Human willpower is finite. To ensure your smart saving strategy doesn’t fail, set up automatic transfers. On the day you get paid, automatically route 20% of your funds directly into your savings or investment accounts so you never even see it in your checking account.

Income Potential & Earnings Breakdown

You might be wondering, “How does saving money relate to my income potential?” In the world of making money online, capital equals speed. Here is a realistic breakdown of how your 20% smart saving bucket can translate into larger earnings:

- The Beginner Phase ($100 – $500 saved/month): Use this capital to buy a domain, hosting, and basic marketing tools. This minimal investment can start generating your first $50-$200/month in digital income within 3-6 months.

- The Growth Phase ($500 – $1,500 saved/month): You now have the funds to run targeted ads, hire freelance writers, or invest in premium SEO tools. Your profit margins begin to widen as you buy back your time.

- The Scaling Phase ($1,500+ saved/month): At this level, your savings can be funneled into dividend-paying index funds or acquiring existing, cash-flowing websites—the ultimate form of passive income.

Disclaimer: Earnings vary widely based on work ethic, market conditions, and business models. Smart saving provides the safety net; your execution provides the profit.

Alternative Methods & Variations

The 50/30/20 rule is a fantastic benchmark, but it is not a rigid law. Depending on your current financial situation and your revenue streams, you might need to adjust the ratios:

- The 70/20/10 Rule: Best for lower-income earners or those living in high-cost-of-living areas. You allocate 70% to needs, 20% to debt/savings, and 10% to wants.

- The 40/10/50 Rule: Best for aggressive entrepreneurs living a minimalist lifestyle. You live on 40% (needs), spend 10% (wants), and aggressively funnel 50% into smart saving and business investments.

- The Side Hustle Variation: Keep your 9-to-5 income on a strict 50/30/20 budget, but take 100% of your work from home or side hustle profits and funnel them directly into your 20% savings/investment category.

Best Practices & Optimization Tips

To truly master smart saving and maximize your capital for online ventures, consider these efficiency hacks:

- High-Yield Environments: Never leave your 20% savings in a standard checking account earning 0.01%. Move it to a High-Yield Savings Account (HYSA) to combat inflation.

- Audit Subscriptions Quarterly: Every 90 days, review your 30% “Wants” category. Cancel software, streaming services, and memberships you haven’t used in the last month.

- Use Cash-Back Strategically: Route your “Needs” and “Wants” spending through cash-back credit cards (paid in full monthly) to generate an extra 1-3% return on everyday purchases.

- Community Accountability: Join financial independence forums or online business communities. Surrounding yourself with people focused on financial freedom accelerates your own results.

Common Mistakes to Avoid

Even with a simple framework, beginners often stumble. Avoid these common pitfalls to ensure your smart saving plan doesn’t derail:

- Confusing Wants with Needs: Upgraded high-speed internet is a “Need” if you work from home, but the premium cable package bundled with it is a “Want.” Be ruthless in your categorization.

- Ignoring the “Latte Factor” entirely: While you shouldn’t obsess over $4 coffees, completely ignoring small daily expenses can quickly blow up your 30% wants budget. Track everything.

- Raiding the 20% for Emergencies that Aren’t Emergencies: A website redesign or a new premium WordPress theme is a business expense, not a personal financial emergency. Don’t drain your safety net for non-essential upgrades.

- Failing to Adjust for Income Spikes: When you hit a great month with your online earnings, don’t just increase your “Wants.” Recalculate the 50/30/20 ratio so your savings rate scales with your income potential.

Long-Term Sustainability & Growth

Smart saving is not a 30-day challenge; it is a lifelong operating system. As your digital income grows, your strategy must evolve:

- Reinvestment Strategies: Once your 3-6 month emergency fund is full, shift the focus of your 20% bucket. Start using it to acquire assets (stocks, real estate, or digital properties) that create new revenue streams.

- Protecting Profit Margins: As a freelancer or creator, lifestyle creep is your biggest enemy. If you start making an extra $2,000 a month, avoid upgrading your car or apartment immediately. Maintain your old “Needs” baseline while supercharging your savings.

- Future-Proofing: Automate your taxes. When earning money online, you are responsible for self-employment tax. Set aside 25-30% of your gross online income into a separate tax bucket before you apply the 50/30/20 rule to your net pay.

Conclusion

Mastering the 50/30/20 rule is the foundation of smart saving and the launching pad for your online business. By clearly categorizing your needs, capping your wants, and ruthlessly protecting your 20% savings, you build the capital necessary to invest in passive income streams and achieve true financial freedom. Remember, it’s not just about how much money you make online, but how much of it you keep and grow.

Ready to start your journey? Drop your biggest budgeting questions in the comments below! Don’t forget to subscribe for weekly money-making strategies, and share your progress in our community.

FAQs

How much money can I realistically save using this method?

If you earn $4,000 a month after taxes and strictly follow the rule, you will save $800 a month. Over a year, that equates to $9,600 in smart saving capital to invest or pay down debt.

Do I need prior budgeting experience to use the 50/30/20 rule?

No prior experience is necessary. This framework is designed specifically for beginners because of its broad, forgiving categories rather than micro-managing every single penny.

What’s the initial investment to start this budgeting method?

Zero dollars. You can start today using a pen and paper or a free spreadsheet. The only investment required is your time to review your past expenses.

How long until I see financial results?

Most people experience significant stress relief within the first 30 days of organizing their money. Meaningful wealth accumulation and debt reduction usually become highly visible within 60 to 90 days of consistent application.

Is this method still working in today’s economy?

Yes. While inflation can make the 50% “Needs” category challenging to maintain, the core philosophy of limiting discretionary spending to ensure you are saving 20% remains one of the most reliable paths to financial stability.

What are the risks involved with this saving strategy?

The strategy itself carries no financial risk. The only risk is behavioral: failing to accurately track expenses or lacking the discipline to stick to the 30% limit for “Wants.”

Before you go, tap those stars!

Straightforward, no gimmicks, just solid banking advice

I clicked on this article expecting it to push some specific bank or financial product with referral links. I was pleasantly surprised. The advice was unbiased, focused on principles rather than promoting any particular institution, and gave me a clear framework to evaluate my own options. I appreciated that the article addressed the importance of FDIC insurance, automatic transfers, and goal-setting — things that seem obvious but that most people (including me) overlook. The writing was clear and concise, without the usual fluff or overly complex financial jargon. The only reason I’m giving four stars instead of five is that I would have liked even more detail on how to balance saving with paying down debt. Still, this was one of the most practical and trustworthy articles on saving I’ve read in a long time. Highly recommend.

Solid advice that cuts through the noise

I’ve been saving for years, but I kept wondering if my money was actually working as hard as it could be. There’s so much conflicting information out there — regular savings accounts, money market accounts, CDs, high-yield options — it gets confusing fast. This article did an excellent job comparing the options side by side, explaining the pros and cons of each, and helping me figure out which strategy made sense for my situation. I especially appreciated the section on the importance of emergency funds versus long-term savings, and the breakdown of how compound interest really adds up over time. I ended up moving my savings to a high-yield account and setting clearer goals. Practical, well-researched, and genuinely helpful.

Small changes, noticeable results

I’ll be honest — I clicked on this article expecting generic advice like “drive less” (thanks, captain obvious). But I was genuinely impressed. The article breaks down the actual science behind why certain habits affect fuel economy, with real numbers to back it up. I learned that my lead-foot acceleration and speeding were costing me way more than I realized. The section on vehicle maintenance was especially valuable — I didn’t know a dirty air filter could impact mileage that much. The tone was straightforward, no fluff, no upselling expensive products. Just solid, practical advice that actually works. My fuel expenses dropped by about 15% last month without me changing my overall driving needs.

Finally, practical advice that doesn’t require buying a new car

As someone who drives over 400 miles a week for work, gas expenses have been crushing my budget. I’ve read countless articles that basically just say “buy an electric vehicle” — which isn’t helpful when that’s not in my budget. This article was a game-changer. The tips were immediately actionable: combining trips, checking tire pressure (I didn’t realize how much that affects mileage!), and using gas price apps. I started implementing these suggestions last month, and I’ve already saved about $40. The writing was clear, well-organized, and respected that not everyone can just trade in their car. Highly recommend for anyone feeling the pain at the pump.

Perfect for renters who can’t install solar panels

As someone who rents an apartment, I often feel limited when it comes to making my home more energy-efficient. I can’t just install new appliances or add insulation to the walls. This article was a lifesaver because it focused on renter-friendly solutions—things like weatherstripping for doors, smart power strips, and optimizing how I use my existing appliances. The writing was straightforward and didn’t assume I owned a home. My only small critique is that I would have loved even more rent-specific examples, but overall, this was incredibly helpful. My electric bill dropped by about $15 last month!