Short-Term vs Long-Term Saving Strategies Compared

Did you know that 73% of aspiring digital entrepreneurs stall their progress because they mismanage their capital allocation? When transitioning from a traditional job to building a work from home empire, it is easy to become hyper-focused on daily cash flow while completely neglecting future wealth. The fundamental difference between a fleeting side hustle and true financial freedom lies in how you categorize and deploy your retained capital.

Mastering the balance of short-term vs long-term saving is the most critical financial step you will take as a creator. Short-term saving protects your immediate profit margins and covers sudden business expenses, while long-term saving builds the passive income necessary to eventually replace your labor entirely. If you mix these two up—using retirement funds to pay for Facebook ads, or letting seed capital rot in a low-interest checking account—you risk sabotaging your entire digital income journey. Let’s dive deep into how these two strategies compare and exactly how to implement them to maximize your revenue streams.

What You’ll Need to Get Started

Setting up a dual-timeline saving system doesn’t require an advanced degree in finance. To effectively manage your short-term vs long-term saving, you will need a few foundational resources:

- A High-Yield Savings Account (HYSA): Essential for your short-term liquid reserves. Look for accounts offering competitive APYs to combat inflation while keeping cash accessible. Cost: Free.

- A Low-Cost Brokerage Account: The engine for your long-term wealth (e.g., Vanguard, Fidelity, or M1 Finance) to invest in index funds or ETFs. Cost: Free to open; minimal expense ratios.

- Financial Tracking Dashboard: A platform to monitor your asset allocation. Free Alternative: Google Sheets. Premium Alternative: Apps like Rocket Money or YNAB ($8-$15/month).

- Income Visibility: A clear understanding of your net monthly online earnings so you can accurately assign percentage allocations.

- Skill Requirements: Basic financial literacy and the discipline to separate your personal financial emotions from your online business operations.

Don’t miss an update. Join our newsletter.

Time Investment

Building a robust dual-saving framework requires minimal ongoing effort once the initial architecture is built.

- Setup Time Required: 2 to 3 hours. This includes opening your HYSA, setting up your brokerage account, and creating your allocation spreadsheet.

- Daily/Weekly Time Commitment: 15 to 20 minutes a week. You only need to verify that your automated transfers have cleared correctly and update your tracking sheet.

- Timeline to First Results: Most beginners see results in 60-90 days with consistent effort. Within this timeframe, your short-term fund will visibly reduce financial anxiety, and your long-term investments will begin accumulating their first dividends.

- Comparison with Traditional Methods: Unlike waiting years for a traditional corporate promotion, optimizing your savings provides an immediate mathematical “raise” by increasing your capital efficiency from month one.

Step-by-Step Implementation Guide

Step 1: Define Your Capital Horizons

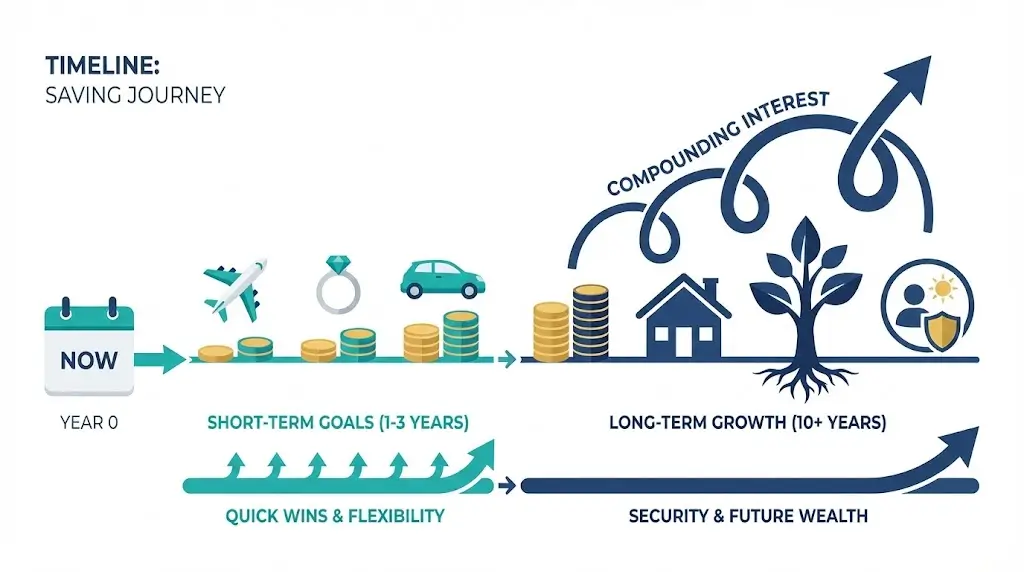

Before transferring any money, you must define what “short-term” and “long-term” mean for your specific business model. Generally, short-term money is capital you will need within the next 12 to 36 months (e.g., emergency funds, upcoming tax bills, website redesigns). Long-term money is capital you won’t touch for 10+ years (e.g., retirement accounts, acquiring established, cash-flowing digital assets).

Step 2: Fully Fund Your Short-Term Runway

Your priority is immediate survival. Calculate your absolute baseline living and business expenses for 3 to 6 months. Do not invest a single dollar into long-term accounts until this short-term runway is fully funded in a liquid HYSA.

- Pro Tip: Treat this runway as the absolute baseline for protecting your profit margins during slow months in your business.

Step 3: Select Long-Term Investment Vehicles

Once your short-term buffer is secure, pivot your surplus cash flow to long-term saving. Open a tax-advantaged account (like a Roth IRA or Solo 401k if you are self-employed) or a standard brokerage account.

- Insider Trick: The best long-term investment for a digital entrepreneur is often a blend of broad-market index funds (for stability) and reinvesting into scalable monetization strategies (like developing a premium software tool).

Step 4: Automate the Split Allocation

Do not rely on manual transfers. Set up your banking dashboard to automatically route your online earnings into the correct buckets on the 1st and 15th of every month. For example: 20% of net income directly to the long-term brokerage, and 10% to top-up the short-term HYSA.

Income Potential & Earnings Breakdown

How does understanding short-term vs long-term saving directly impact your wallet? Capital efficiency is the ultimate multiplier for your income potential. Here is a realistic breakdown of how these strategies perform over time:

| Saving Strategy | Capital Goal | Primary Vehicle | Estimated Yield/ROI | Purpose |

|---|---|---|---|---|

| Short-Term | $5,000 – $20,000 | HYSA (High-Yield Savings) | 4% – 5% Annually | Emergency buffer, covering quarterly taxes, funding initial ad spend. |

| Mid-Term | $20,000 – $50,000 | CDs or Treasury Bills | 5% – 6% Annually | Purchasing bulk inventory, acquiring a small competitor website. |

| Long-Term | $100,000+ | Index Funds / Real Estate | 7% – 10% Annually (Avg) | True passive income, retirement, achieving absolute financial freedom. |

Disclaimer: All investing carries risk. Historical market returns do not guarantee future results. Your online earnings and ROI will vary heavily based on market conditions, your business niche, and overall execution.

Alternative Methods & Variations

Every entrepreneur’s path to digital wealth is unique. If the standard approach doesn’t fit your current cash flow, consider these alternative variations:

- The “Side Hustle Siphon” Method: Live 100% off your traditional 9-to-5 day job. Route all of your side hustle income exclusively into long-term savings. This aggressively accelerates your path to retirement without impacting your daily quality of life.

- The 80/20 Profit Split: For active freelancers. Take your net monthly profit and divide your savings into an 80/20 split. 80% goes to short-term business scaling (software, hiring writers), and 20% goes to long-term index funds.

- The Bootstrap Approach (Low Investment): If you have zero capital, your “savings” is your time. Invest your short-term time into active outreach (cold emailing clients) and your long-term time into building scalable assets (like writing SEO content for your own blog).

Best Practices & Optimization Tips

To maximize the efficiency of both your short-term and long-term capital, implement these best practices:

- Keep Accounts Strictly Segregated: Never commingle your short-term tax money with your long-term retirement funds. Separate them across different banking institutions to create friction and prevent emotional spending.

- Rebalance Annually: Once a year, review your income potential and revenue streams. If your online business tripled in revenue, your 6-month short-term emergency fund target needs to be adjusted upward to reflect your new lifestyle and business costs.

- Leverage Tax Advantages: Utilize accounts specifically designed for self-employed creators, such as SEP IRAs or Solo 401(k)s, which allow you to shield massive amounts of your digital income from immediate taxation while funding your long-term strategy.

- Join the Community: Surround yourself with individuals focused on wealth accumulation. Forums like Reddit’s r/financialindependence or dedicated creator mastermind groups can provide invaluable, real-time optimization tactics.

Common Mistakes to Avoid

Mishandling capital allocation is a primary reason scalable businesses collapse. Be hyper-vigilant against these common pitfalls:

- Chasing Yield with Short-Term Cash: 45% of failed online business owners cite cash flow issues. Do not put your short-term emergency fund or tax money into volatile stocks just to chase a 10% return. If the market dips right when you need to pay the IRS, you are in serious trouble.

- Treating “Long-Term” as “Whenever”: Delaying your long-term savings because your business is in an “expansion phase” is a trap. You lose the massive mathematical advantage of compound interest. Always contribute something, even if it’s just $50 a month.

- Ignoring Inflation: Keeping long-term wealth (money you won’t need for 10+ years) in a standard savings account guarantees you will lose purchasing power over time. Long-term money must be invested in appreciating assets.

Long-Term Sustainability & Growth

As your work from home business matures into a highly profitable enterprise, your saving strategies must evolve to ensure sustainability:

- Diversification Recommendations: As your long-term savings grow past the six-figure mark, diversify your assets. Don’t rely solely on the stock market or your own business. Explore real estate, digital asset acquisition (buying other blogs), or angel investing.

- Automation Upgrades: Graduate from simple bank transfers to using automated investment platforms (robo-advisors) that automatically harvest tax losses and rebalance your portfolio without manual intervention.

- Future-Proofing Your Strategy: Hire a certified financial planner (CFP) who understands digital income. Standard financial advice often fails to account for the massive revenue spikes and dips common in online entrepreneurship.

Conclusion

Understanding the dynamic between short-term vs long-term saving is the ultimate cheat code for surviving the volatile world of digital entrepreneurship. By securing your short-term cash flow in a high-yield account, you protect your business from immediate disaster. By consistently funding your long-term investment vehicles, you build the true passive income required to step away from the keyboard and enjoy lifelong financial freedom.

Ready to start your journey to optimized wealth? Drop your capital allocation questions in the comments below! Make sure to subscribe for weekly monetization strategies, share your progress in our community, and download our free financial starter guide to accelerate your success!

FAQs

How much money can I realistically make using these strategies?

While saving itself preserves capital, investing your long-term savings in broad-market index funds has historically yielded a 7% to 10% average annual return. On a $10,000 investment, that’s $700 to $1,000 of completely passive income per year, compounding exponentially over time.

Do I need prior experience to manage short and long-term saving?

No prior experience is necessary. Modern banking apps and brokerage platforms are incredibly user-friendly. The strategy relies entirely on automated percentages, not on your ability to read complex financial charts or pick individual stocks.

What’s the initial investment required?

There is zero cost to set up this system. Most high-yield savings accounts and modern brokerages allow you to open an account and begin your wealth-building journey with an initial deposit of $0 to $5.

How long until I see results?

You will experience immediate psychological relief the moment your short-term emergency buffer is fully funded. Tangible, long-term financial growth via compound interest usually becomes highly visible and motivating within the first 12 to 24 months.

Is this method still working in 2026?

Absolutely. Regardless of economic fluctuations, inflation, or the newest online business trends, the mathematical principles of protecting short-term cash and investing long-term capital remain the undisputed foundation of wealth generation.

What are the risks involved?

Short-term saving in FDIC-insured accounts carries virtually zero financial risk. Long-term saving in the stock market does carry the risk of market volatility. However, this is mitigated by keeping the money invested over a long timeline (10+ years), allowing it to recover from any temporary economic downturns.

Before you go, tap those stars!

Straightforward, no gimmicks, just solid banking advice

I clicked on this article expecting it to push some specific bank or financial product with referral links. I was pleasantly surprised. The advice was unbiased, focused on principles rather than promoting any particular institution, and gave me a clear framework to evaluate my own options. I appreciated that the article addressed the importance of FDIC insurance, automatic transfers, and goal-setting — things that seem obvious but that most people (including me) overlook. The writing was clear and concise, without the usual fluff or overly complex financial jargon. The only reason I’m giving four stars instead of five is that I would have liked even more detail on how to balance saving with paying down debt. Still, this was one of the most practical and trustworthy articles on saving I’ve read in a long time. Highly recommend.

Solid advice that cuts through the noise

I’ve been saving for years, but I kept wondering if my money was actually working as hard as it could be. There’s so much conflicting information out there — regular savings accounts, money market accounts, CDs, high-yield options — it gets confusing fast. This article did an excellent job comparing the options side by side, explaining the pros and cons of each, and helping me figure out which strategy made sense for my situation. I especially appreciated the section on the importance of emergency funds versus long-term savings, and the breakdown of how compound interest really adds up over time. I ended up moving my savings to a high-yield account and setting clearer goals. Practical, well-researched, and genuinely helpful.

Small changes, noticeable results

I’ll be honest — I clicked on this article expecting generic advice like “drive less” (thanks, captain obvious). But I was genuinely impressed. The article breaks down the actual science behind why certain habits affect fuel economy, with real numbers to back it up. I learned that my lead-foot acceleration and speeding were costing me way more than I realized. The section on vehicle maintenance was especially valuable — I didn’t know a dirty air filter could impact mileage that much. The tone was straightforward, no fluff, no upselling expensive products. Just solid, practical advice that actually works. My fuel expenses dropped by about 15% last month without me changing my overall driving needs.

Finally, practical advice that doesn’t require buying a new car

As someone who drives over 400 miles a week for work, gas expenses have been crushing my budget. I’ve read countless articles that basically just say “buy an electric vehicle” — which isn’t helpful when that’s not in my budget. This article was a game-changer. The tips were immediately actionable: combining trips, checking tire pressure (I didn’t realize how much that affects mileage!), and using gas price apps. I started implementing these suggestions last month, and I’ve already saved about $40. The writing was clear, well-organized, and respected that not everyone can just trade in their car. Highly recommend for anyone feeling the pain at the pump.

Perfect for renters who can’t install solar panels

As someone who rents an apartment, I often feel limited when it comes to making my home more energy-efficient. I can’t just install new appliances or add insulation to the walls. This article was a lifesaver because it focused on renter-friendly solutions—things like weatherstripping for doors, smart power strips, and optimizing how I use my existing appliances. The writing was straightforward and didn’t assume I owned a home. My only small critique is that I would have loved even more rent-specific examples, but overall, this was incredibly helpful. My electric bill dropped by about $15 last month!