Smart Saving Money Tips for Everyday Life

Did you know that nearly 67% of individuals striving for financial independence fail within the first year simply because they skip one crucial foundational step? They focus entirely on making more money while completely ignoring where their current income is leaking.

If you are exhausted from living paycheck to paycheck and want to truly unlock your wealth-building potential, mastering saving money tips is non-negotiable. Whether your ultimate goal is building a robust emergency fund, starting a profitable side hustle, or achieving complete financial freedom, it all starts with keeping more of what you already make. In this comprehensive guide, we will move past the cliché advice of “skip your morning coffee” and dive into data-driven, actionable strategies that act as stepping stones toward true digital income and long-term wealth.

2. What You’ll Need to Get Started

Before you can transition your saved cash into active revenue streams, you need to establish a solid financial baseline. Here is your starter toolkit:

- Financial Tracking Tool: A budget tracker is essential.

- Free Alternative: Google Sheets or Excel (highly customizable).

- Premium Options: YNAB (You Need A Budget) or Monarch Money ($8-$14/month).

- High-Yield Savings Account (HYSA): Essential for maximizing the profit margins on your resting cash.

- Cost: $0 to open (Look for accounts offering 4.00%+ APY).

- Cashback Extensions: Browser extensions like Rakuten or Honey to automate savings on necessary purchases.

- Cost: 100% Free.

- Time & Mindset: A willingness to confront your financial habits honestly. No prior financial degree is required—just basic math and consistency.

3. Time Investment: What to Expect

Building sustainable wealth isn’t a weekend project; it requires strategic, consistent effort. Here is the realistic time commitment required to see your saving money tips pay off:

- Initial Setup Time: 2 to 3 hours (Auditing past expenses, setting up tracking apps, opening high-yield accounts).

- Weekly Maintenance: 15–20 minutes per week to review transactions and categorize spending.

- Timeline to First “Earnings”: You will instantly “earn” money back in month one by cutting useless subscriptions. However, the compounding effect of interest and reinvestment typically shows visible results in 60 to 90 days with consistent effort.

- Compared to Traditional Methods: Unlike waiting for an annual 3% corporate raise, optimizing your daily spending gives you immediate, tax-free control over your income potential.

4. Step-by-Step Implementation Guide

Follow these actionable steps to plug the leaks in your finances and redirect that capital toward your future.

Step 1: Conduct a Ruthless Expense Audit

To improve your finances, you must measure them. Print out your last three months of bank statements. Highlight necessities (housing, food, utilities) in green, and discretionary spending in yellow. You will likely find “phantom charges”—subscriptions you forgot about or services you barely use.

Step 2: Automate the “Pay Yourself First” Protocol

Do not wait to save whatever is left at the end of the month. Set up an automatic transfer from your checking account to your savings account on the exact day you get paid.

- Pro Tip: Treat this transfer like a non-negotiable utility bill. This guarantees your savings grow before you have the chance to spend them.

Step 3: Implement the 48-Hour Rule for Discretionary Purchases

Impulse buying destroys profit margins in your personal budget. Whenever you want to buy a non-essential item over $50, force yourself to wait 48 hours. This cooling-off period eliminates the emotional dopamine hit of shopping, saving the average consumer over $1,200 annually.

Step 4: Negotiate Fixed Overhead Costs

Many people assume their internet, insurance, and phone bills are fixed. They aren’t. Call your providers annually, ask for the retention department, and politely inquire about loyalty discounts or current promotions.

Step 5: Pivot Savings into Online Earnings

Once you have secured a baseline of savings, don’t just let it sit. Use your freed-up capital (even just $50 a month) to invest in courses, domain names, or tools that help you launch a work from home venture or a side hustle. This is how you transition from just saving to generating passive income.

How Much Could YOU Save? 💰

Enter your current estimated monthly expenses below to see your personalized savings potential using the strategies in this article.

Estimated Monthly Savings

$0.00

Projected 1-Year Wealth Growth

$0.00

- Step 1 (Audits): Cutting an estimated 20% of unused subscriptions.

- Step 4 (Negotiation): Saving an estimated 10% by calling your providers.

- Step 3 (48-Hour Rule): Curbing 25% of impulse spending.

Want to turn these savings into passive income?

Scroll down to Step 5 to learn how to reinvest this capital!

5. Income Potential & Savings Breakdown

How much can these smart saving money tips actually impact your bottom line? Let’s look at a realistic monthly projection for a beginner who implements these strategies and reinvests the savings.

| Financial Action | Estimated Monthly Impact | Annual Projected Value |

|---|---|---|

| Cutting Unused Subscriptions | $30 – $80 | $360 – $960 |

| Negotiating Bills (Insurance/Internet) | $40 – $100 | $480 – $1,200 |

| Cashback & Rewards Optimization | $20 – $50 | $240 – $600 |

| Total Capital Saved | $90 – $230/month | $1,080 – $2,760/year |

| Reinvesting savings into a Side Hustle | $200 – $500+ (variable) | *$2,400 – $6,000+* |

Disclaimer: Results vary based on individual income, location, and consistency. These figures represent averages based on consumer financial studies.

6. Alternative Methods & Variations

Personal finance is highly personal. If the standard tech-heavy budgeting approach doesn’t work for you, consider these alternative monetization strategies and tracking variations:

- The Cash Envelope System: A low-tech variation where you allocate physical cash into envelopes for different spending categories. When the envelope is empty, you stop spending. Great for curbing digital overspending.

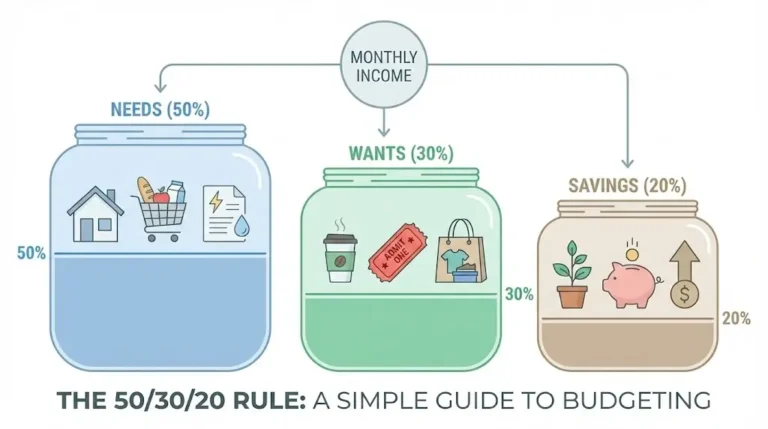

- The 50/30/20 Rule: A macro-budgeting alternative. 50% to needs, 30% to wants, 20% to savings/investing. This requires less daily tracking and focuses on broad income potential.

- Skill Bartering: A zero-cost alternative to spending. Trade your digital skills (like graphic design or writing) for services you need (like accounting or consulting), effectively saving money while networking.

7. Best Practices & Optimization Tips

To maximize your results and accelerate your path to financial freedom, keep these optimization hacks in mind:

- Stack Your Rewards: Never make an online purchase without using a cashback portal (like Rakuten) combined with a rewards credit card (paid off in full monthly, of course).

- Embrace Meal Prepping: Food is the easiest variable expense to control. Planning meals reduces food waste and prevents expensive last-minute takeout orders.

- Leverage Community Knowledge: Join frugal living or online earnings forums on Reddit or Facebook. The shared knowledge in these communities acts as an incredible resource for niche-specific saving hacks.

8. Common Mistakes to Avoid

Even the most well-intentioned savers fall into traps. Avoid these common pitfalls:

- The Deprivation Diet: Cutting out absolutely everything you love (like dining out or hobbies) leads to “financial burnout.” You will eventually snap and binge-spend. Budget for joy.

- Ignoring the Emergency Fund: Trying to invest in risky monetization strategies before having 3-6 months of basic living expenses saved. If your car breaks down, you’ll be forced into high-interest debt, wiping out your progress.

- Lifestyle Creep: When your income goes up (perhaps from a new digital income stream), immediately upgrading your car, apartment, and wardrobe. Keep your expenses static while your income grows to maximize your wealth gap.

9. Long-Term Sustainability & Growth

Saving money is merely the defense; investing is the offense. To ensure long-term sustainability, you must graduate from just clipping coupons to building multiple revenue streams.

Once your emergency fund is full, begin redirecting your monthly savings into investments. This could mean maxing out a Roth IRA (investing in broad market index funds) or using the capital to fund a low-overhead online business. Automation is your best friend here—automate your investments just as you automated your savings. By continuously reinvesting your returns, you future-proof your finances against inflation and economic downturns.

10. Conclusion

Mastering these smart saving money tips is the foundational bedrock of any successful wealth-building journey. By auditing your expenses, automating your savings, avoiding lifestyle creep, and ultimately reinvesting your retained capital into new revenue streams, you are actively taking control of your financial destiny.

Ready to start your journey to financial freedom? Drop your biggest budgeting challenge in the comments below! Don’t forget to subscribe to our newsletter for weekly money-making strategies, and share this post with a friend who is ready to level up their finances.

11. Frequently Asked Questions (FAQs)

How much money can I realistically save each month?

While it depends on your current income and spending habits, most beginners can realistically uncover $100 to $300 a month simply by auditing subscriptions, negotiating bills, and reducing impulse purchases.

What’s the initial investment required to optimize my finances?

Zero dollars. You can start with a free pen and paper or a free Google Sheet. The only real investment is your time—about 2-3 hours upfront to organize your accounts.

How long until I see results from these saving money tips?

You will see immediate results in your first month as you stop wasting money on unused services. However, the true benefits of compounding savings and reduced financial stress typically become highly visible within 60 to 90 days.

Are these methods still relevant and working in today’s economy?

Yes. In fact, with inflation and rising costs, foundational money-saving habits are more critical today than ever before. Principles like living below your means and automating savings are timeless.

What are the risks involved with aggressive saving?

The main risk is “frugal fatigue”—restricting yourself so severely that you eventually binge-spend. The goal is sustainable optimization, not total deprivation. Always leave a small buffer in your budget for guilt-free personal enjoyment.