15 Free Money Saving Chart Printables to Track Your Goals

Did you know that nearly 73% of aspiring online entrepreneurs fail simply because they run out of seed capital before their business ever gets off the ground? They spend countless hours researching passive income ideas, but completely neglect the single most effective psychological trick for retaining the money they already make: visual tracking.

If you want to achieve genuine financial freedom, you cannot rely on willpower alone. You need a constant, visual reminder of your financial targets. This is where a money saving chart becomes your ultimate secret weapon. By physically coloring in your progress, you trigger a hit of dopamine that turns frugality into a highly addictive game.

In this comprehensive guide, we will break down 15 free money saving chart printables you can use today, showing you exactly how to use them to plug your budget leaks and build the capital required to fund your dream side hustle.

What You’ll Need to Get Started

How Much Could a Savings Chart Save YOU?

Enter your estimated spending below to see how visually tracking your goals can transform your finances.

You do not need an accounting degree or expensive financial software to master your personal finances. Here is exactly what you need to implement a visual tracking system:

- A Printer and Paper: To print your chosen free money saving chart templates.

- Markers or Highlighters: To physically color in your progress (the physical act of coloring is crucial for psychological commitment).

- A Dedicated Savings Account: Preferably a High-Yield Savings Account (HYSA) separate from your checking account.

- A Visual Display Area: A refrigerator door, office bulletin board, or bathroom mirror.

- Initial Investment: $0 to $5 (for ink and markers). This method focuses entirely on optimizing your existing resources.

- Skill Requirements: Basic addition and the willingness to be brutally honest about your daily spending.

Time Investment

Building wealth is a process of compound interest and compound habits. Fortunately, a visual system requires very little time once the foundation is laid:

- Setup Time Required: 10 to 15 minutes to print your chart, set your goal, and tape it to your wall.

- Daily/Weekly Time Commitment: 2 minutes a day to transfer funds and color in your progress.

- Timeline to First Results: Most beginners see a tangible shift in their spending behavior within 14 days, and visible bank account growth in 60-90 days with consistent effort.

- Compared to Traditional Income: Building sustainable online earnings or a profitable blog can take 6 to 12 months. In contrast, skipping a $20 takeout meal and coloring in a $20 square on your chart puts money back into your pocket today, instantly widening your personal profit margins.

Step-by-Step Implementation Guide

Follow these sequential steps to establish a visual saving routine that actually works.

Step 1: Choose Your Ideal Money Saving Chart

Select a printable that matches your specific goal. Here are 15 popular chart styles you can easily find or create:

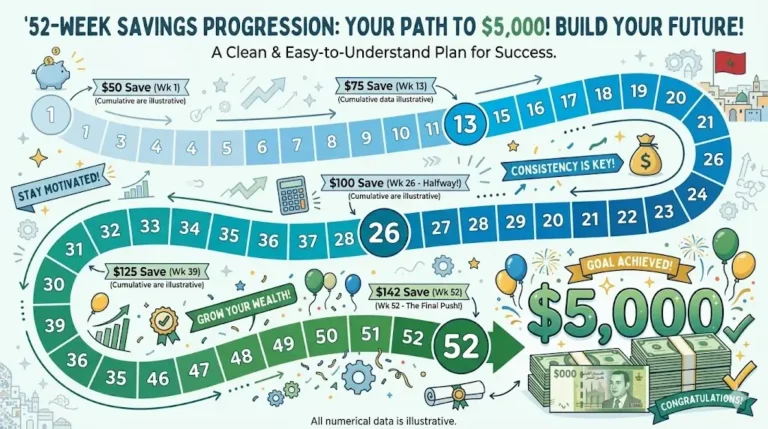

- The 52-Week Challenge Grid: Save an increasing amount each week ($1 to $52).

- The $1,000 Emergency Fund Thermometer: Perfect for beginners building a safety net.

- The No-Spend Month Calendar: Color in every day you don’t buy non-essentials.

- The Side Hustle Seed Capital Jar: A drawing of a mason jar to fund your business.

- The Debt Payoff Tracker: A visual countdown to zero balances.

- The $5,000 Vacation Fund: Map out a visual journey to your dream destination.

- The 100-Envelope Challenge Grid: Pick a random square (1-100) and save that dollar amount.

- The Bi-Weekly Paycheck Saver: Syncs with your payday schedule.

- The Penny-a-Day Challenge: A micro-saving chart for extreme beginners.

- The Holiday Shopping Fund: Prevent December credit card debt.

- The House Down Payment Tracker: A long-term chart for a massive goal.

- The Digital Income Reinvestment Chart: Track the profits you reinvest into your business.

- The $10,000 Financial Freedom Grid: 100 squares worth $100 each.

- The Sinking Funds Tracker: For predictable annual expenses (car registration, insurance).

- The Custom Blank Goal Chart: A blank grid you can tailor to any specific monetary target.

Step 2: Define Your “Why”

Write your ultimate goal at the top of your money saving chart. Are you saving for new podcast equipment for your work from home setup? Write it down. A clear “why” prevents you from quitting in week three.

Step 3: Math It Out

Divide your total goal by the number of icons/squares on your printable. If you have a 50-square chart and a $1,000 goal, each square represents $20.

Step 4: Transfer, Then Color

Never color a square until the money has physically left your checking account and landed in your dedicated savings account.

Step 5: Display It Proudly

Hang your chart somewhere you will see it every single day. The constant visual cue will subconsciously deter you from making impulse purchases online.

Income Potential & Earnings Breakdown

While a chart doesn’t print cash, the capital you retain is mathematically identical to earning new income. By using a money saving chart, you are actively generating the seed money that increases your ultimate income potential. Here is a realistic breakdown of what different charts can yield:

| Type of Chart Completed | Total Capital Created | Potential Reinvestment Opportunity |

|---|---|---|

| 52-Week Challenge | $1,378 | Web hosting & premium business software |

| 100-Envelope Challenge | $5,050 | Inventory for an e-commerce store |

| $10,000 Goal Grid | $10,000 | High-yield dividend portfolio / Real Estate |

| No-Spend Month (Average) | $350 – $600 | Ad spend for your new digital product |

Disclaimer: Savings results vary significantly based on individual income, fixed expenses, and dedication to the process.

Alternative Methods & Variations

If physical printables and markers feel too old-school for your lifestyle, try these highly effective modern variations:

- Digital Budgeting Dashboards: Use tools like Notion, Excel, or Google Sheets to create a digital spreadsheet that automatically colors cells based on your inputs.

- The Automated Web App: Use modern financial tracking apps (like TrackThrift) to automatically monitor your daily spending and track your progress toward your custom goals.

- Bullet Journaling: Instead of printing a pre-made chart, draw your own custom grids and thermometers inside a dedicated financial bullet journal.

- The “Income Focused” Variation: Use a chart to track your new online earnings. Instead of tracking money saved from cutting expenses, use the squares to track every $50 you make from your new freelance gig.

Best Practices & Optimization Tips

To guarantee the success of your new visual tracking routine, implement these expert hacks:

- Habit Stacking: Tie your coloring routine to an existing habit. For example, transfer your funds and color your chart every Friday morning while drinking your coffee.

- Involve the Household: If you are saving for a family goal, let your children or partner color in the squares. It turns budgeting into a team sport rather than a restrictive chore.

- Buffer Your Checking Account: Always leave a $100 “cushion” in your main checking account to prevent accidental overdraft fees when transferring money to your savings.

- Celebrate Milestones: Did you fill up 25% of your chart? Reward yourself with a small, inexpensive treat to prevent deprivation fatigue.

Common Mistakes to Avoid

Even highly motivated savers fall into common traps. Protect your progress by avoiding these pitfalls:

- Coloring Before Transferring: The biggest mistake is coloring a square because you “intend” to save the money later. Only mark progress when the funds are fully secured in your savings account.

- Setting Unrealistic Goals: Trying to complete a $10,000 chart in three months when you only make $4,000 a month is a recipe for instant burnout. Choose a chart that challenges you but remains mathematically possible.

- Hiding the Chart: Keeping your money saving chart tucked away in a closed binder defeats the purpose. It must be a visible, daily psychological trigger.

- Quitting After a Bad Week: If you have an expensive week and can’t fill in a square, do not throw the chart away. Financial journeys are never perfectly linear. Just resume the following week.

Long-Term Sustainability & Growth

Completing your first visual tracker is just the launching pad. Long-term financial sustainability requires shifting from a “saving” mindset to a wealth-building mindset.

Once your money saving chart helps you establish a solid emergency fund, you must pivot your strategy. Take the new capital you are generating and begin directing it toward aggressive monetization strategies. Invest in index funds, real estate, or tools that generate digital income. By consistently converting your saved cash into active revenue streams, you transition from simply living paycheck-to-paycheck to building a future-proof financial fortress.

Conclusion

Taking control of your personal finances doesn’t require a six-figure salary; it requires visibility and intention. By utilizing a simple, free money saving chart, you remove the abstract nature of budgeting, quickly plug your spending leaks, and build the capital required to fund your dream life.

Ready to start your journey? Drop a comment below telling us which of the 15 charts you are going to use first! Be sure to subscribe for more weekly money-making strategies, and share your colored-in progress in our community forum.

FAQs

How much money can I realistically make or save with these charts?

While you aren’t “earning” new money, optimizing your expenses via a visual tracker typically frees up $150 to $500 a month for the average household, acting as a massive tax-free raise.

Do I need prior experience to start tracking?

Not at all. A visual chart is actually much easier for beginners than a complex spreadsheet. Coloring in a square requires zero financial literacy, making it highly accessible.

What’s the initial investment?

Zero dollars. You simply need a piece of paper, a pen, and a printer to get started today.

How long until I see results?

You will gain immense clarity on your spending habits by the end of week one. Noticeable compound growth in your savings account usually becomes highly motivating within 30 to 60 days.

Is this analogmethod still working in the current digital economy?

Absolutely. In a world of invisible “one-click” digital purchases, the physical friction of writing down and coloring your savings is one of the most effective ways to rewire your brain’s spending habits.

What are the risks involved?

There is zero financial risk. The only minor risk is burnout if you set your savings target too high. Always leave room in your budget for basic entertainment and unexpected minor costs.

Before you go, tap those stars!

Straightforward, no gimmicks, just solid banking advice

I clicked on this article expecting it to push some specific bank or financial product with referral links. I was pleasantly surprised. The advice was unbiased, focused on principles rather than promoting any particular institution, and gave me a clear framework to evaluate my own options. I appreciated that the article addressed the importance of FDIC insurance, automatic transfers, and goal-setting — things that seem obvious but that most people (including me) overlook. The writing was clear and concise, without the usual fluff or overly complex financial jargon. The only reason I’m giving four stars instead of five is that I would have liked even more detail on how to balance saving with paying down debt. Still, this was one of the most practical and trustworthy articles on saving I’ve read in a long time. Highly recommend.

Solid advice that cuts through the noise

I’ve been saving for years, but I kept wondering if my money was actually working as hard as it could be. There’s so much conflicting information out there — regular savings accounts, money market accounts, CDs, high-yield options — it gets confusing fast. This article did an excellent job comparing the options side by side, explaining the pros and cons of each, and helping me figure out which strategy made sense for my situation. I especially appreciated the section on the importance of emergency funds versus long-term savings, and the breakdown of how compound interest really adds up over time. I ended up moving my savings to a high-yield account and setting clearer goals. Practical, well-researched, and genuinely helpful.

Small changes, noticeable results

I’ll be honest — I clicked on this article expecting generic advice like “drive less” (thanks, captain obvious). But I was genuinely impressed. The article breaks down the actual science behind why certain habits affect fuel economy, with real numbers to back it up. I learned that my lead-foot acceleration and speeding were costing me way more than I realized. The section on vehicle maintenance was especially valuable — I didn’t know a dirty air filter could impact mileage that much. The tone was straightforward, no fluff, no upselling expensive products. Just solid, practical advice that actually works. My fuel expenses dropped by about 15% last month without me changing my overall driving needs.

Finally, practical advice that doesn’t require buying a new car

As someone who drives over 400 miles a week for work, gas expenses have been crushing my budget. I’ve read countless articles that basically just say “buy an electric vehicle” — which isn’t helpful when that’s not in my budget. This article was a game-changer. The tips were immediately actionable: combining trips, checking tire pressure (I didn’t realize how much that affects mileage!), and using gas price apps. I started implementing these suggestions last month, and I’ve already saved about $40. The writing was clear, well-organized, and respected that not everyone can just trade in their car. Highly recommend for anyone feeling the pain at the pump.

Perfect for renters who can’t install solar panels

As someone who rents an apartment, I often feel limited when it comes to making my home more energy-efficient. I can’t just install new appliances or add insulation to the walls. This article was a lifesaver because it focused on renter-friendly solutions—things like weatherstripping for doors, smart power strips, and optimizing how I use my existing appliances. The writing was straightforward and didn’t assume I owned a home. My only small critique is that I would have loved even more rent-specific examples, but overall, this was incredibly helpful. My electric bill dropped by about $15 last month!