The Fastest Way to Save Money: A Practical Step-by-Step Guide

Did you know that 69% of aspiring entrepreneurs fail because they bleed capital before they even make their first dollar? We live in a culture obsessed with building the perfect side hustle and generating rapid online earnings. But focusing solely on making more money while ignoring your spending habits is like pouring water into a bucket with a massive hole in the bottom.

If you are looking for the fastest way to save money, you have already taken the most important step toward true financial freedom. Before you can invest or scale a business, you must master the art of retaining the money you already make. In this comprehensive guide, we will walk you through exactly how to stop cash leaks, maximize your current capital, and build a foundation for lasting wealth.

⚡ Quick Answer

The fastest way to save money is to immediately initiate a “spending freeze” on all non-essential items, ruthlessly cancel recurring “vampire” subscriptions, and negotiate your fixed monthly bills. By automatically redirecting this freed-up cash into a high-yield account, you can see massive financial results within your first 30 days.

Don’t let these numbers stay a fantasy!

The fastest way to guarantee you hit these savings goals is to track your money in real-time. Stop guessing where your cash goes and start commanding it. Use TrackThrift to monitor your spending and savings every month.

Start Tracking on TrackThriftWhat You’ll Need to Get Started

You do not need a degree in finance or a massive salary to start retaining more of your cash. Implementing these strategies requires zero initial investment and relies entirely on free, accessible tools.

- Your Last 90 Days of Bank Statements: Crucial for identifying your actual spending baseline.

- A High-Yield Savings Account (HYSA): Stop using traditional banks that pay 0.01%. You need an account that pays 4% to 5% APY.

- An Expense Tracking Tool: Free apps like TrackThrift, EveryDollar, or a simple Google Sheet to monitor your cash flow.

- Initial Capital Required: $0. (In fact, this process generates capital).

- Skill Requirements: Basic addition/subtraction and the discipline to say “no” to impulse purchases.

Time Investment

Managing your money is not a full-time job. Once you put a system in place, it runs almost entirely on autopilot, acting as a reliable, hands-off mechanism for wealth building.

- Setup Time Required: 2 to 3 hours (Downloading statements, canceling subscriptions, opening your HYSA).

- Daily/Weekly Time Commitment: 3 to 5 minutes a day to log your expenses.

- Timeline to First Results: Most beginners see results in 60-90 days with consistent effort. However, with the aggressive strategies outlined below, you will see a noticeable cash surplus by your very next paycheck.

Step-by-Step Implementation Guide

Step 1: Execute a 48-Hour “Spending Freeze”

The absolute fastest way to save money is to simply stop spending it. For the next 48 hours, commit to a zero-spend challenge. You are only allowed to spend money on absolute survival necessities (basic groceries and gas to get to work).

- Pro Tip: Unlink your credit cards from Amazon, Apple Pay, and Google Pay. Adding friction to the checkout process reduces impulse buying by up to 40%.

Step 2: Slay the “Vampire” Subscriptions

Pull up your bank statements. Highlight every recurring charge. Streaming services, premium app features, unused gym memberships, and subscription boxes drain your accounts silently. Cancel anything you haven’t actively used in the last 14 days.

Step 3: Negotiate Your Fixed Overhead

You can drastically improve your profit margins simply by making a few phone calls. Call your internet provider, car insurance company, and cell phone carrier. Ask for the “customer retention department” and tell them you are considering switching to a competitor. In many cases, they will offer you a lower promotional rate just to keep your business.

Step 4: Automate Your Wealth

If you wait until the end of the month to save what is left, you will save nothing. Set up an automatic transfer from your checking account to your savings account the exact day you get paid. Treating your savings like a non-negotiable bill is one of the most effective monetization strategies for your personal budget.

Income Potential & Earnings Breakdown

When you cut expenses, every dollar saved is a dollar earned—and better yet, it is completely tax-free. Let’s look at how optimizing your lifestyle directly boosts your income potential:

| Savings Strategy | Estimated Monthly Savings | Annual “Income” Equivalent |

|---|---|---|

| Canceling 3 unused subscriptions | $35.00 | $420.00 |

| Negotiating car & internet bills | $60.00 | $720.00 |

| Meal prepping lunches (4x/week) | $160.00 | $1,920.00 |

| Brewing coffee at home | $90.00 | $1,080.00 |

| Total Freed-Up Capital | **$345.00** | $4,140.00 |

Note: These figures represent realistic averages. By treating these cutbacks as immediate “earnings,” you essentially give yourself a $4,000+ raise this year without working a single extra hour.

Alternative Methods & Variations

If traditional budgeting doesn’t work for your psychology, try these proven alternatives to accelerate your savings:

- The Cash Envelope System: Withdraw your monthly allowance for discretionary spending in physical cash. When the envelope is empty, spending stops. This method makes the pain of parting with money feel “real.”

- Leveraging a Work From Home Setup: If your job allows remote work, eliminate your daily commute. The savings on gas, car maintenance, and professional clothing are astronomical.

- The 30-Day Rule: For any non-essential purchase over $100, force yourself to wait 30 days. Write it down. If you still want it 30 days later, you can buy it. (Hint: 90% of the time, the urge vanishes).

Best Practices & Optimization Tips

To squeeze every ounce of efficiency out of your budget and maximize your digital income, implement these optimization hacks:

- Use Cash-Back Portals: Never buy anything online without using a portal like Rakuten, Honey, or Capital One Shopping. You can earn 2% to 10% back on purchases you were going to make anyway.

- Embrace the “Used” Economy: Buy refurbished tech, shop for gently used furniture, and browse thrift stores.

- Optimize Your Grocery Runs: Utilize online grocery pickup. By avoiding the physical aisles, you completely eliminate the temptation to buy impulse snacks, easily saving $30 to $50 per trip.

Common Mistakes to Avoid

Even smart people lose momentum when saving money because they fall into predictable psychological traps. Watch out for these pitfalls:

- Deprivation Burnout: The fastest way to fail is to cut everything you love. If you love lattes, keep the lattes! But cut ruthlessly on things you don’t care about (like name-brand paper towels or cable TV).

- Skipping the Emergency Fund: Never aggressively pay off low-interest debt or invest in stocks until you have $1,000 to $2,000 in cash. A single unexpected car repair will send you spiraling back into credit card debt if you lack a safety net.

- Succumbing to Lifestyle Creep: When you start generating online earnings or get a raise at your job, it is incredibly tempting to upgrade your lifestyle. To build wealth, lock in your current living expenses and save 100% of your new income.

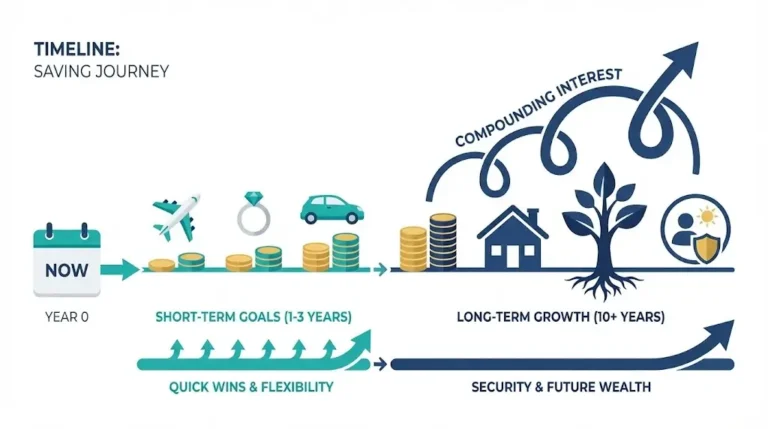

Long-Term Sustainability & Growth

Saving money rapidly is thrilling, but you cannot shrink your way to massive wealth. The ultimate goal is to transition from simply saving money to creating multiple revenue streams.

Once you have established a 3 to 6-month emergency fund, you must put that money to work. Start funneling your excess cash into low-cost index funds, dividend stocks, or use it as seed capital for an online business that generates passive income. By keeping your expenses low and continually reinvesting your savings, you create a snowball effect that practically guarantees long-term financial security.

Conclusion

Finding the fastest way to save money doesn’t require a miracle; it requires immediate action, deep awareness of your spending habits, and an automated system. By executing a spending freeze, negotiating your bills, and paying yourself first, you take absolute control of your financial destiny. The capital you rescue today is the seed money for your wealthy future.

Ready to start your journey? Drop your biggest budgeting question in the comments below! Be sure to subscribe for our weekly money-making strategies, and share your 30-day savings progress in our community!

FAQs

How much money can I realistically make or save using these methods?

Your savings potential is directly linked to your current income and spending habits. While beginners typically save between $200 and $500 in their first month by cutting “vampire” expenses and meal prepping, high earners with inflated lifestyles can often save thousands.

Do I need prior experience in finance?

Absolutely not. Personal finance is 80% behavior and 20% head knowledge. If you can do basic subtraction and commit to tracking your expenses, you have all the skills required.

What’s the initial investment?

There is zero initial investment required. You can utilize free budgeting apps, your current bank statements, and free high-yield savings accounts to execute every step in this guide.

How long until I see results?

You will see immediate cash flow improvements by your very next paycheck if you cancel unused subscriptions today. For compounding, long-term wealth, most beginners see a total financial transformation within 12 to 18 months.

Is this method still working in 2026?

Yes. While the economy, inflation, and technology change, the fundamental mathematics of spending less than you earn, negotiating overhead, and automating your investments is a timeless strategy.

What are the risks involved?

The only risk in saving money is keeping it in a standard bank account where inflation slowly erodes its purchasing power. To mitigate this, ensure your cash is in a High-Yield Savings Account (HYSA) or properly invested in the market once your emergency fund is full.

Before you go, tap those stars!

Straightforward, no gimmicks, just solid banking advice

I clicked on this article expecting it to push some specific bank or financial product with referral links. I was pleasantly surprised. The advice was unbiased, focused on principles rather than promoting any particular institution, and gave me a clear framework to evaluate my own options. I appreciated that the article addressed the importance of FDIC insurance, automatic transfers, and goal-setting — things that seem obvious but that most people (including me) overlook. The writing was clear and concise, without the usual fluff or overly complex financial jargon. The only reason I’m giving four stars instead of five is that I would have liked even more detail on how to balance saving with paying down debt. Still, this was one of the most practical and trustworthy articles on saving I’ve read in a long time. Highly recommend.

Solid advice that cuts through the noise

I’ve been saving for years, but I kept wondering if my money was actually working as hard as it could be. There’s so much conflicting information out there — regular savings accounts, money market accounts, CDs, high-yield options — it gets confusing fast. This article did an excellent job comparing the options side by side, explaining the pros and cons of each, and helping me figure out which strategy made sense for my situation. I especially appreciated the section on the importance of emergency funds versus long-term savings, and the breakdown of how compound interest really adds up over time. I ended up moving my savings to a high-yield account and setting clearer goals. Practical, well-researched, and genuinely helpful.

Small changes, noticeable results

I’ll be honest — I clicked on this article expecting generic advice like “drive less” (thanks, captain obvious). But I was genuinely impressed. The article breaks down the actual science behind why certain habits affect fuel economy, with real numbers to back it up. I learned that my lead-foot acceleration and speeding were costing me way more than I realized. The section on vehicle maintenance was especially valuable — I didn’t know a dirty air filter could impact mileage that much. The tone was straightforward, no fluff, no upselling expensive products. Just solid, practical advice that actually works. My fuel expenses dropped by about 15% last month without me changing my overall driving needs.

Finally, practical advice that doesn’t require buying a new car

As someone who drives over 400 miles a week for work, gas expenses have been crushing my budget. I’ve read countless articles that basically just say “buy an electric vehicle” — which isn’t helpful when that’s not in my budget. This article was a game-changer. The tips were immediately actionable: combining trips, checking tire pressure (I didn’t realize how much that affects mileage!), and using gas price apps. I started implementing these suggestions last month, and I’ve already saved about $40. The writing was clear, well-organized, and respected that not everyone can just trade in their car. Highly recommend for anyone feeling the pain at the pump.

Perfect for renters who can’t install solar panels

As someone who rents an apartment, I often feel limited when it comes to making my home more energy-efficient. I can’t just install new appliances or add insulation to the walls. This article was a lifesaver because it focused on renter-friendly solutions—things like weatherstripping for doors, smart power strips, and optimizing how I use my existing appliances. The writing was straightforward and didn’t assume I owned a home. My only small critique is that I would have loved even more rent-specific examples, but overall, this was incredibly helpful. My electric bill dropped by about $15 last month!