How to Use the Envelope Budget System to Manage Your Money

Did you know that 67% of aspiring online entrepreneurs fail—not because they lack a good idea, but because they completely mismanage their personal cash flow?

When you are trying to build wealth, whether through a traditional 9-to-5 or exciting new online earnings, controlling where your money goes is step one. Enter the envelope budget system. This time-tested cash management strategy forces you to be intentional with every dollar, preventing the mindless spending that drains your bank account. By mastering the envelope budget system, you don’t just pay your bills; you actively free up capital to fund your side hustle, boost your profit margins, and accelerate your journey toward true financial freedom.

Quick Answer

The envelope budget system is a cash-based financial strategy where you allocate your monthly income into specific categories (envelopes) like groceries, gas, and entertainment. Once the cash in a specific envelope is gone, you cannot spend any more in that category for the month, forcing strict financial discipline and freeing up money for savings or investments.

Discover Your Envelope Savings Potential

Studies show that using physical cash envelopes saves the average person 20% on their variable expenses by eliminating mindless tapping. Let’s calculate your potential!

What You’ll Need to Get Started

Implementing this system requires minimal upfront investment. In fact, the goal is to keep your costs as close to zero as possible so you can maximize your revenue streams. Here is what you need to get started:

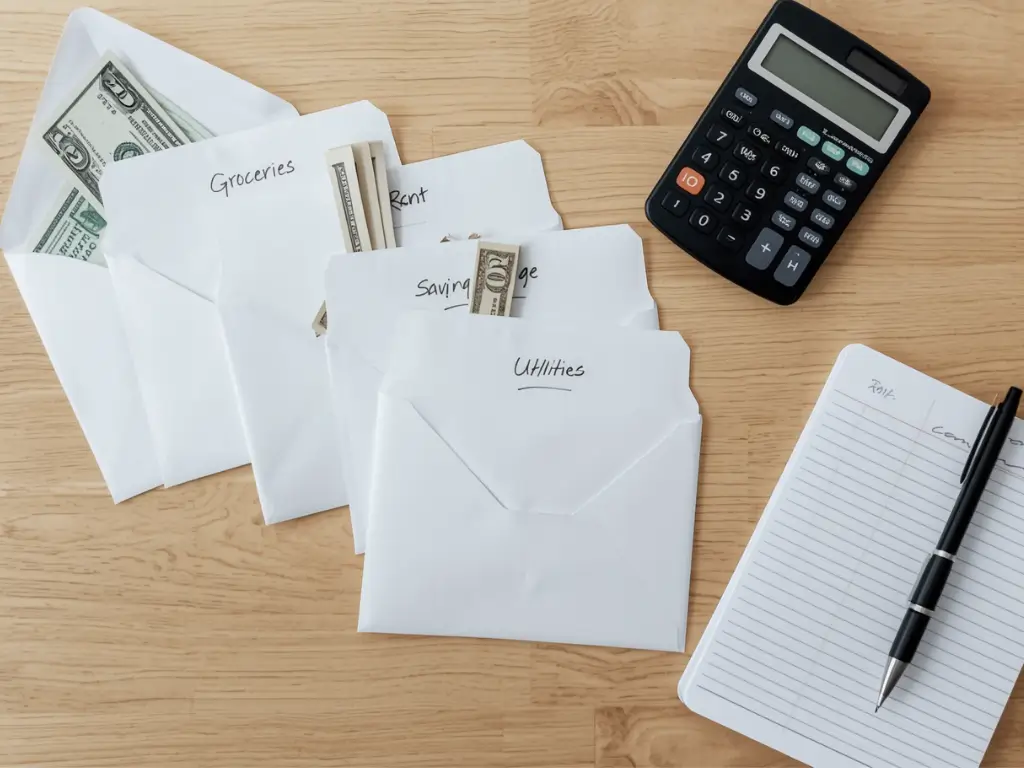

- Physical Envelopes: A basic box of paper envelopes or a reusable cash binder wallet. (Estimated Cost: $2 – $15)

- A Budgeting Dashboard: A notebook, an Excel spreadsheet, or a free budgeting template to track your initial categories. (Estimated Cost: Free)

- A Clear Income Baseline: You must know exactly what your monthly take-home pay is. If you rely on work from home freelance gigs, calculate your average baseline income.

- Discipline and Commitment: The most crucial “tool.” The system only works if you stick to the boundaries you set. (Skill requirement: Beginner-friendly)

Time Investment

Unlike complex accounting software, the envelope budget system is straightforward, though it requires a brief setup phase.

- Setup Time Required: 2 to 3 hours to review your past bank statements, categorize your spending, and label your envelopes.

- Daily/Weekly Time Commitment: 10 to 15 minutes a week to withdraw cash, divide it among your envelopes, and record your spending.

- Timeline to First Results: You will feel a sense of control immediately. However, most beginners see results in 60-90 days with consistent effort, usually noticing a significant surplus of cash by month three.

- Comparison: Traditional passive tracking (just looking at your bank app) takes less time but often leads to overspending. The envelope system’s slight time investment yields exponentially higher savings.

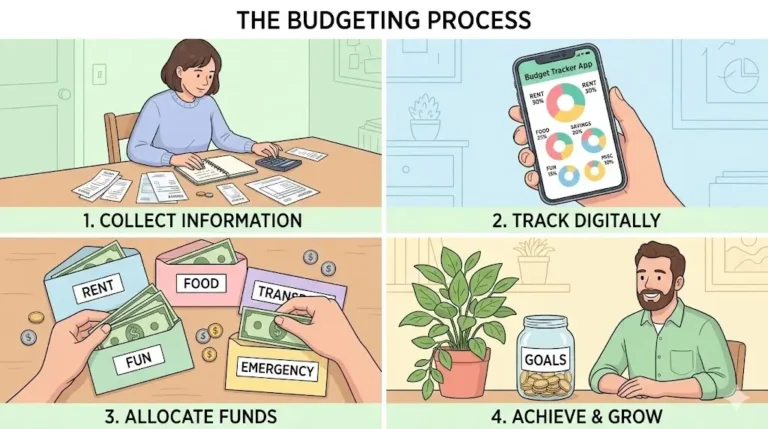

Step-by-Step Implementation Guide

Step 1: Calculate Your Total Take-Home Income

Before you can fill any envelopes, you need to know exactly how much money is coming in. Write down your primary salary, and add any secondary digital income or side hustle earnings. Use your net income (after taxes).

- Pro Tip: If your income fluctuates due to freelance work, base your budget on your lowest-earning month to play it safe.

Step 2: Define Your Core Categories

Review your past 30 days of expenses. Separate your fixed expenses (rent, utilities, debt payments) from your variable expenses (groceries, dining out, entertainment). The envelope system is designed specifically for variable expenses where you tend to overspend.

Step 3: Create and Label Your Envelopes

Take your physical envelopes and label them with your variable categories. Common labels include:

- Groceries

- Gas/Transportation

- Dining Out

- Entertainment

- Personal Care

- Side Hustle Investment (Use this to save up for new monetization strategies!)

Step 4: Stuff Your Envelopes

When you get paid, go to the bank and withdraw the exact cash amount you budgeted for your variable expenses. Distribute the cash into the corresponding envelopes.

- Insider Trick: Ask the bank teller for smaller denominations ($10s and $20s) so it’s easier to make exact purchases without breaking $100 bills everywhere.

Step 5: Stop Spending When the Envelope is Empty

This is the golden rule of the envelope budget system. If your “Dining Out” envelope is empty by the 20th of the month, you cannot eat at a restaurant until the next month. You must cook at home using the groceries you already bought.

Income Potential & Savings Breakdown

While budgeting isn’t a direct income generator, the capital it frees up has massive income potential when reinvested correctly. By stopping financial leaks, you effectively give yourself a raise.

- Beginner Level (First 3 Months): Most users discover they were wasting 15-20% of their income on impulse buys. Savings Potential: $200 – $500/month.

- Intermediate Level (Months 3-6): As you optimize, you can funnel this saved cash into building digital assets. Savings Potential: $500 – $1,000/month.

- Advanced Level (Year 1+): By strictly managing your money, you can invest your surplus into high-yield passive income streams (like dividend stocks or starting a niche website).

- Case Study: Mark, a freelance graphic designer, used the envelope method to cap his lifestyle spending. He saved an extra $400 a month, which he used to run paid ads for his services, effectively turning his saved cash into a $2,000/month revenue boost.

Alternative Methods & Variations

Carrying physical cash isn’t for everyone, especially if you manage most of your business online. Here are some modern variations:

- The Digital Envelope System: Use budgeting apps like YNAB (You Need A Budget) or Goodbudget. These apps simulate digital envelopes, syncing directly with your debit cards to track category balances in real-time.

- The Multiple Bank Account Method: Open several free checking accounts (one for bills, one for fun, one for emergencies) and set up automatic transfers. This creates “digital envelopes” without needing an app.

- The Hybrid Approach: Use digital systems for fixed expenses and large bills, but use physical cash exclusively for your “danger zones” (like eating out or hobbies) where you are most likely to overspend.

Best Practices & Optimization Tips

To maximize your savings and successfully maintain this system, follow these proven strategies:

- The Rollover Strategy: If you have $30 left in your Grocery envelope at the end of the month, don’t spend it! Roll it over to next month, or better yet, sweep it into a high-yield savings account to build financial freedom.

- Always Carry a “Buffer”: Keep a $50 miscellaneous envelope in your car for genuine, minor emergencies so you aren’t tempted to break out the credit card.

- Track Your Side Hustle Separately: Never mix your personal envelopes with your business expenses. Keep your digital income and operating costs in a completely separate ecosystem to maintain clear profit margins.

Common Mistakes to Avoid

Even with the best intentions, the envelope budget system can fail if you fall into these common traps:

- Borrowing from Other Envelopes: Taking $20 from “Groceries” to fund “Entertainment” defeats the entire purpose of the system. Once the money is assigned, respect the boundary.

- Making Categories Too Specific: Having an envelope for “Coffee,” another for “Snacks,” and another for “Fast Food” is exhausting. Combine these into one “Dining Out” envelope.

- Giving Up After Month One: Statistic: 45% of people quit budgeting after the first 30 days because they miscalculated their initial needs. Month one is a trial run. Expect to adjust your envelope amounts in month two.

- Forgetting Sinking Funds: Don’t forget to create envelopes for irregular expenses like car maintenance, annual subscriptions, or holiday gifts.

Long-Term Sustainability & Growth

The ultimate goal of the envelope budget system is not to restrict your life forever, but to build disciplined habits that allow you to grow your wealth.

Once you have mastered your cash flow, you can start automating your finances. You will eventually transition from physical cash to a fully automated digital system because you will have built the internal discipline to stop overspending.

Furthermore, the money you save using this system is the exact seed capital you need to fund your future. Whether you want to buy real estate, start a dropshipping business, or invest in courses to increase your earning potential, your envelopes provide the financial foundation for long-term growth.

Conclusion

The envelope budget system is a powerful, low-tech solution to the modern problem of mindless spending. By giving every dollar a physical home, you force yourself to align your spending with your actual priorities. This discipline is the cornerstone of generating wealth, funding your side hustles, and achieving ultimate financial freedom.

Ready to start your journey to financial control? Grab a box of envelopes today and set up your first three categories! Drop your questions in the comments below, subscribe for weekly money-making strategies, and share your budgeting progress in our community.

FAQs

How much money can I realistically save using this method?

While results vary based on your income, the average person saves between 15% and 20% of their variable income simply by cutting out impulse purchases and sticking to their physical cash limits.

Do I need prior experience with budgeting to use the envelope system?

No prior experience is necessary. In fact, this system is highly recommended for beginners because it relies on physical, tangible cash rather than complex spreadsheets or confusing financial jargon.

What’s the initial investment to start an envelope budget?

The initial investment is practically zero. All you need are standard paper envelopes and a pen to label them. You are simply reorganizing the money you already have.

How long until I see results?

You will feel a heightened awareness of your spending immediately. However, it typically takes 60 to 90 days to fine-tune your category amounts and see a substantial increase in your retained savings.

Is this method still working in today’s digital economy?

Yes! The psychological friction of handing over physical cash is actually more effective today precisely because it breaks the habit of mindless “tap-to-pay” digital transactions. For digital purists, modern apps successfully replicate the envelope philosophy.

What are the risks involved in carrying physical cash?

The primary risk is the potential for loss or theft. To mitigate this, only withdraw the cash you need for one to two weeks at a time, rather than carrying an entire month’s worth of expenses on your person. Keep the rest safely in your bank account until needed.

Before you go, tap those stars!

Straightforward, no gimmicks, just solid banking advice

I clicked on this article expecting it to push some specific bank or financial product with referral links. I was pleasantly surprised. The advice was unbiased, focused on principles rather than promoting any particular institution, and gave me a clear framework to evaluate my own options. I appreciated that the article addressed the importance of FDIC insurance, automatic transfers, and goal-setting — things that seem obvious but that most people (including me) overlook. The writing was clear and concise, without the usual fluff or overly complex financial jargon. The only reason I’m giving four stars instead of five is that I would have liked even more detail on how to balance saving with paying down debt. Still, this was one of the most practical and trustworthy articles on saving I’ve read in a long time. Highly recommend.

Solid advice that cuts through the noise

I’ve been saving for years, but I kept wondering if my money was actually working as hard as it could be. There’s so much conflicting information out there — regular savings accounts, money market accounts, CDs, high-yield options — it gets confusing fast. This article did an excellent job comparing the options side by side, explaining the pros and cons of each, and helping me figure out which strategy made sense for my situation. I especially appreciated the section on the importance of emergency funds versus long-term savings, and the breakdown of how compound interest really adds up over time. I ended up moving my savings to a high-yield account and setting clearer goals. Practical, well-researched, and genuinely helpful.

Small changes, noticeable results

I’ll be honest — I clicked on this article expecting generic advice like “drive less” (thanks, captain obvious). But I was genuinely impressed. The article breaks down the actual science behind why certain habits affect fuel economy, with real numbers to back it up. I learned that my lead-foot acceleration and speeding were costing me way more than I realized. The section on vehicle maintenance was especially valuable — I didn’t know a dirty air filter could impact mileage that much. The tone was straightforward, no fluff, no upselling expensive products. Just solid, practical advice that actually works. My fuel expenses dropped by about 15% last month without me changing my overall driving needs.

Finally, practical advice that doesn’t require buying a new car

As someone who drives over 400 miles a week for work, gas expenses have been crushing my budget. I’ve read countless articles that basically just say “buy an electric vehicle” — which isn’t helpful when that’s not in my budget. This article was a game-changer. The tips were immediately actionable: combining trips, checking tire pressure (I didn’t realize how much that affects mileage!), and using gas price apps. I started implementing these suggestions last month, and I’ve already saved about $40. The writing was clear, well-organized, and respected that not everyone can just trade in their car. Highly recommend for anyone feeling the pain at the pump.

Perfect for renters who can’t install solar panels

As someone who rents an apartment, I often feel limited when it comes to making my home more energy-efficient. I can’t just install new appliances or add insulation to the walls. This article was a lifesaver because it focused on renter-friendly solutions—things like weatherstripping for doors, smart power strips, and optimizing how I use my existing appliances. The writing was straightforward and didn’t assume I owned a home. My only small critique is that I would have loved even more rent-specific examples, but overall, this was incredibly helpful. My electric bill dropped by about $15 last month!