Building Strong Money Habits That Support Financial Security

Did you know that nearly 70% of high-earning online entrepreneurs end up living paycheck-to-paycheck because they skip this ONE crucial step? We are constantly bombarded with the latest tactics for boosting online earnings and securing the perfect work from home lifestyle. However, before you can successfully manage multiple revenue streams, you must build the invisible foundation of wealth: your Money Habits.

Your daily financial behaviors dictate your future. If you possess poor Money Habits, generating more cash will only lead to larger expenses, not lasting wealth. True financial freedom isn’t just about how much you make; it’s about how much you keep and systematically multiply. In this comprehensive guide, we will break down exactly how to rewire your behavioral psychology, treat your household like a business, and develop the disciplined routines required to fund your entrepreneurial dreams.

What You’ll Need to Get Started

Building rock-solid Money Habits doesn’t require a degree in finance, but it does require setting up an environment designed for success. Treat this preparation like gathering the tools for a new business launch.

Here is what you’ll need to establish your foundation:

- Automated Tracking Software: Cost: $0 – $12/month. Apps like Monarch Money, YNAB, or a free Google Sheets ledger to monitor your daily cash flow.

- A Dedicated “Seed Capital” Account: Cost: Free. A separate high-yield savings account (HYSA) specifically designated to hold the cash you save, preparing it for future monetization strategies.

- Financial Clarity / A “Why”: Cost: Mental Energy. You need a tangible goal. Are you building these habits to fund a side hustle? To quit your 9-to-5? Define it clearly.

- 15 Minutes of Uninterrupted Daily Time: Cost: Free. The commitment to review your financial dashboard daily without distractions.

Time Investment

Unlike building a complex software company or scaling an agency, optimizing your financial habits provides immediate clarity and quick wins.

- Setup Time Required: 2 to 3 hours to gather your accounts, connect them to a tracking app, and define your baseline budget.

- Daily/Weekly Time Commitment: 5 to 10 minutes a day for a quick ledger check-in, plus a 30-minute deep dive every Sunday.

- Timeline to First Results: Most beginners see a complete psychological shift and measurable results in 60-90 days with consistent effort. By month three, the neural pathways in your brain adapt, making saving money feel more rewarding than spending it.

Step-by-Step Implementation Guide

Step 1: Institute the “Daily Micro-Audit”

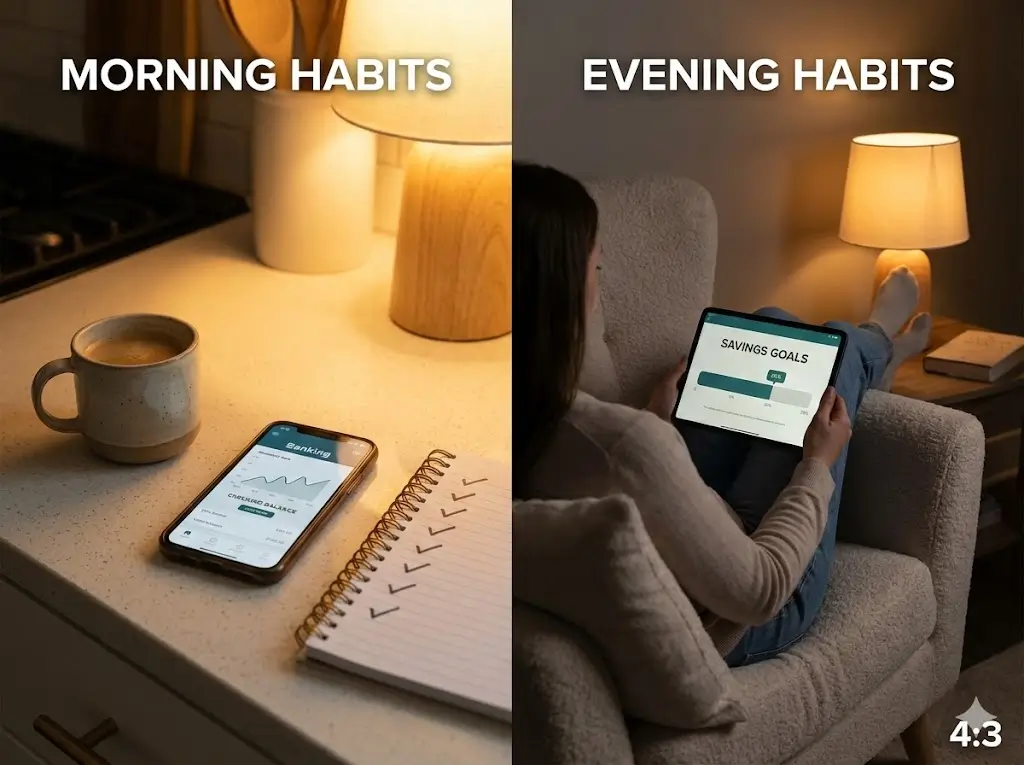

Waiting until the end of the month to check your bank account is a recipe for failure. Instead, build the habit of the Daily Micro-Audit. Every morning while drinking your coffee, spend exactly 3 minutes looking at your transactions from the day before. This keeps your household profit margins top of mind and instantly curbs impulsive spending.

- Pro Tip: Do not judge your spending during the daily audit; simply categorize it. Awareness is the first step to behavioral change.

Step 2: Automate the “Pay Yourself First” Principle

Willpower is a finite resource. The strongest Money Habits rely on zero willpower. Set up an automatic transfer with your bank so that the moment your paycheck (or digital income) hits your account, a strict percentage (e.g., 15-20%) is instantly routed to your investment or side-hustle funding accounts.

- Insider Trick: If your income fluctuates as a freelancer, automate a percentage rather than a fixed dollar amount to avoid overdrafts.

Step 3: Enforce the 72-Hour Cooling-Off Period

Online shopping algorithms are designed to break your willpower. Combat this by implementing a 72-hour rule for any non-essential purchase over $100. Add the item to your cart, but close the tab. If you still genuinely need it three days later, buy it. 90% of the time, the emotional urge will fade, protecting your capital.

Step 4: Reallocate “Wasted” Capital into Income-Producing Assets

The goal of good Money Habits isn’t just to hoard cash. Once you’ve identified and eliminated subscriptions or daily expenses you don’t need, immediately give that money a new job. Redirect it into assets that generate passive income, like dividend-paying index funds or seed capital for your next digital venture.

Income Potential & Earnings Breakdown

How do simple daily habits translate into actual earnings? By optimizing your personal retention rate, you create the capital required to invest. Here is a realistic look at the income potential of mastering your financial behaviors:

| Habit Level | Capital Retained Monthly | Primary Deployment Strategy | 10-Year Projected Growth (at 8% ROI) |

|---|---|---|---|

| Beginner | $300 | Emergency fund & basic index investing | ~$54,000 |

| Intermediate | $800 | Funding a scalable side hustle or e-commerce | ~$146,000 |

| Advanced | $2,000+ | Aggressive passive income & business acquisitions | ~$365,000+ |

Disclaimer: Earnings, returns, and specific income amounts are highly variable and depend on market conditions. Investing and business creation involve risk.

Alternative Methods & Variations

Personal finance is highly personal. If the strict tracking method doesn’t align with your psychology, try these alternative habit frameworks:

- The Cash Envelope System (Digital or Physical): Best for chronic over-spenders. Allocate specific funds for variable expenses. When the envelope is empty, spending stops completely.

- The “One Metric” Focus: If tracking everything is overwhelming, track only your biggest problem area (e.g., dining out or online shopping) and ignore the rest until that single habit is fixed.

- The Revenue-First Approach: For entrepreneurs, instead of focusing purely on cutting expenses, build the habit of allocating specific time blocks daily to activities that directly increase your revenue streams, ensuring income outpaces lifestyle costs.

Best Practices & Optimization Tips

To maximize the efficiency of your new habits, lean into these advanced optimization strategies:

- Habit Stacking: Connect your new money habit to an existing one. (e.g., “After I brush my teeth, I will check my bank balance.”)

- Optimize Your Yields: Don’t let your retained capital sit idle. Move it to high-yield savings accounts or Treasury bills while you decide how to deploy it into your online earnings ventures.

- Quarterly Deep Cleans: Every 90 days, perform a ruthless audit of your recurring subscriptions. Companies rely on “status quo bias”—your habit of forgetting you’re paying them.

Common Mistakes to Avoid

Even seasoned digital entrepreneurs stumble when building these routines. Avoid these highly common pitfalls:

- Attempting a “Financial Crash Diet”: Cutting all your discretionary spending to zero overnight will lead to burnout and a massive spending binge. Prevention: Allow a small, structured budget for guilt-free fun.

- Allowing Lifestyle Creep: As your monetization strategies pay off and your income rises, the biggest mistake is upgrading your car or house immediately. Prevention: Lock in your living expenses and let the extra income compound in investments.

- Confusing Motion with Action: Spending three hours organizing a colorful budgeting spreadsheet but never actually saying “no” to a purchase is fake progress. Focus on the actual behavior of not swiping the card.

Long-Term Sustainability & Growth

Building strong Money Habits is not a 30-day challenge; it is the operating system for your entire life.

To future-proof your financial security, you must practice aggressive diversification. As your initial habits bear fruit and your capital grows, start automating your investments into varied asset classes (equities, real estate, digital assets). Continuously educate yourself by reading books like Atomic Habits and The Psychology of Money to ensure your mindset grows alongside your portfolio. When the habits run on autopilot, your wealth scales without your direct daily input.

Conclusion

Establishing strong Money Habits is the quiet, unglamorous secret behind every successful entrepreneur’s financial security. By taking control of your daily micro-decisions, automating your savings, and treating your personal finances with the respect of a thriving business, you unlock the capital needed to build your ideal life.

Ready to start your journey? Drop your biggest financial habit struggle in the comments below! Subscribe for our weekly money-making strategies, download our free starter guide, and share your progress in our community!

FAQs

How much money can I realistically make by changing my money habits?

While habits themselves preserve capital rather than generating it directly, the average person recovers $300 to $500 monthly by optimizing their spending. Reinvesting $500 a month at an 8% return can generate over $146,000 in a decade.

Do I need prior experience to start building these habits?

No prior financial experience is necessary. Building money habits is about managing human behavior and psychology, not complex mathematics. Anyone can begin by simply logging their daily expenses.

What’s the initial investment to get started?

The monetary investment is absolutely zero. You can use free tools like Google Sheets or your bank’s native app. The only requirement is a time investment of about 15 minutes a day.

How long until I see results?

You will gain profound clarity within the first week of tracking your expenses. However, most individuals see a significant increase in retained capital and a decrease in financial stress within 60 to 90 days.

Is this method still working in 2026?

Yes. Regardless of economic conditions, inflation, or the year, the psychological principles of delaying gratification, curbing impulse buys, and living below your means remain the absolute foundation of wealth building in 2026 and beyond.

What are the risks involved?

The primary psychological risk is “frugality fatigue”—depriving yourself too strictly, leading to burnout. The financial risk occurs if you successfully save the money but leave it in cash where inflation degrades its purchasing power, rather than investing it into income-producing assets.

Before you go, tap those stars!

Straightforward, no gimmicks, just solid banking advice

I clicked on this article expecting it to push some specific bank or financial product with referral links. I was pleasantly surprised. The advice was unbiased, focused on principles rather than promoting any particular institution, and gave me a clear framework to evaluate my own options. I appreciated that the article addressed the importance of FDIC insurance, automatic transfers, and goal-setting — things that seem obvious but that most people (including me) overlook. The writing was clear and concise, without the usual fluff or overly complex financial jargon. The only reason I’m giving four stars instead of five is that I would have liked even more detail on how to balance saving with paying down debt. Still, this was one of the most practical and trustworthy articles on saving I’ve read in a long time. Highly recommend.

Solid advice that cuts through the noise

I’ve been saving for years, but I kept wondering if my money was actually working as hard as it could be. There’s so much conflicting information out there — regular savings accounts, money market accounts, CDs, high-yield options — it gets confusing fast. This article did an excellent job comparing the options side by side, explaining the pros and cons of each, and helping me figure out which strategy made sense for my situation. I especially appreciated the section on the importance of emergency funds versus long-term savings, and the breakdown of how compound interest really adds up over time. I ended up moving my savings to a high-yield account and setting clearer goals. Practical, well-researched, and genuinely helpful.

Small changes, noticeable results

I’ll be honest — I clicked on this article expecting generic advice like “drive less” (thanks, captain obvious). But I was genuinely impressed. The article breaks down the actual science behind why certain habits affect fuel economy, with real numbers to back it up. I learned that my lead-foot acceleration and speeding were costing me way more than I realized. The section on vehicle maintenance was especially valuable — I didn’t know a dirty air filter could impact mileage that much. The tone was straightforward, no fluff, no upselling expensive products. Just solid, practical advice that actually works. My fuel expenses dropped by about 15% last month without me changing my overall driving needs.

Finally, practical advice that doesn’t require buying a new car

As someone who drives over 400 miles a week for work, gas expenses have been crushing my budget. I’ve read countless articles that basically just say “buy an electric vehicle” — which isn’t helpful when that’s not in my budget. This article was a game-changer. The tips were immediately actionable: combining trips, checking tire pressure (I didn’t realize how much that affects mileage!), and using gas price apps. I started implementing these suggestions last month, and I’ve already saved about $40. The writing was clear, well-organized, and respected that not everyone can just trade in their car. Highly recommend for anyone feeling the pain at the pump.

Perfect for renters who can’t install solar panels

As someone who rents an apartment, I often feel limited when it comes to making my home more energy-efficient. I can’t just install new appliances or add insulation to the walls. This article was a lifesaver because it focused on renter-friendly solutions—things like weatherstripping for doors, smart power strips, and optimizing how I use my existing appliances. The writing was straightforward and didn’t assume I owned a home. My only small critique is that I would have loved even more rent-specific examples, but overall, this was incredibly helpful. My electric bill dropped by about $15 last month!