Practical Budgeting Tips for Beginners to Manage Money

Disclaimer: This article provides general financial information and is not intended as professional investment or financial advice. Individual financial situations vary; please consult with a certified financial expert before making significant changes to your financial plan.

Did you know that 78% of full-time workers live paycheck to paycheck, regardless of whether they earn $30,000 or $100,000 a year? It is a startling statistic that proves one thing: your ability to reach financial freedom isn’t determined by how much you make, but by how well you manage what you keep. Most people fail to build a sustainable side hustle or generate passive income simply because their primary revenue streams are leaking through poor planning.

If you feel like your money vanishes the moment it hits your account, you need more than just willpower; you need actionable budgeting tips that work in the real world. In this guide, we’ll break down exactly how to take control of your finances, optimize your profit margins, and create a foundation for long-term wealth—even if you’ve never used a spreadsheet in your life.

What You’ll Need to Get Started

You don’t need expensive software or a degree in accounting to manage your money effectively. Here are the essential budgeting tips tools you’ll need:

- Bank Statements: Access to your last 30–60 days of transactions (digital or paper).

- Budgeting Platform: * Free Alternative: A simple Google Sheet or a physical notebook.

- Tools: Apps like Mint, YNAB (You Need A Budget), or EveryDollar.

- An Emergency Fund Account: A separate high-yield savings account where you won’t be tempted to spend.

- Initial Investment: $0. Budgeting is a process of optimization, not a purchase.

- Skill Requirements: Basic addition/subtraction. If you can use a calculator, you can master these monetization strategies.

The “Money Leak” Calculator

How much could YOU save by following these steps?

Time Investment

Managing your money is a high-leverage activity. A small amount of time spent now yields massive income potential later.

- Setup Time: 60 to 90 minutes for your initial audit and category setup.

- Daily Maintenance: 2 to 5 minutes to log expenses or review your app.

- Weekly Check-in: 15 minutes to ensure you are staying within your limits.

- Timeline to Results: Most beginners see an “extra” $200–$500 in their account within the first 30 days simply by identifying “ghost” expenses (unused subscriptions and impulse buys). Compared to a work from home job, budgeting provides an immediate return on your time.

Step-by-Step Implementation Guide

Follow these sequential steps to turn these budgeting tips into a lifestyle that leads to financial freedom.

Step 1: Track Every Penny for 30 Days

You cannot manage what you do not measure. Use an app or a notebook to record every transaction. This reveals your true “burn rate.” Most people find that small $5–$10 purchases are the primary reason they lack digital income to invest.

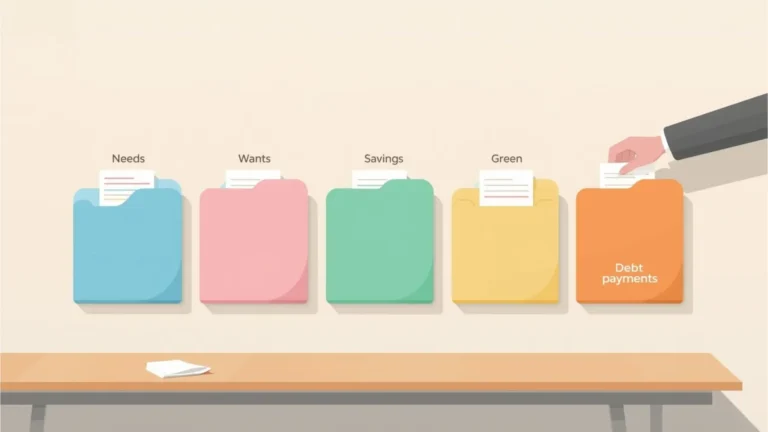

Step 2: Categorize Your Spending (The 50/30/20 Rule)

Divide your spending into three buckets:

- 50% Needs: Housing, utilities, groceries, insurance.

- 30% Wants: Dining out, Netflix, hobbies, travel.

- 20% Savings/Debt: Retirement, emergency fund, or paying off credit cards.

Step 3: Identify Your “Money Leaks”

Look at your “Wants” category. Identify three recurring expenses you can eliminate immediately. This could be a gym membership you don’t use or a premium cable package. These recovered funds become the seed capital for your future online earnings.

Step 4: Automate the Process

Set up “Auto-Pay” for your bills and “Auto-Transfer” for your savings. When your savings move to a different account automatically, you remove the “decision fatigue” that leads to overspending.

Income Potential & Savings Breakdown

Budgeting isn’t just about saving; it’s about “finding” money you already have. By optimizing your current revenue streams, you essentially give yourself a raise.

| Spending Category | Average Monthly Spend | Budgeted Amount | Monthly “Profit” Found |

|---|---|---|---|

| Dining & Takeout | $450 | $200 | **$250** |

| Subscriptions | $120 | $40 | **$80** |

| Impulse Shopping | $200 | $50 | **$150** |

| Total Monthly Gain | $480 |

If you invest that $480 monthly into a diversified index fund with a 7% return, in 10 years you would have over $80,000. That is the power of turning budgeting tips into a long-term monetization strategy.

Alternative Methods & Variations

Every financial personality is different. If the 50/30/20 rule doesn’t fit, try these:

- The Envelope System: Use physical cash for “discretionary” spending. Once the envelope is empty, spending stops. This is great for those who struggle with “invisible” credit card spending.

- Zero-Based Budgeting: Every dollar has a job. Income minus expenses must equal zero at the end of the month.

- Anti-Budgeting: Focus only on your savings goal. If you save 20% off the top, you are free to spend the rest however you want.

Best Practices & Optimization Tips

- Use the 24-Hour Rule: For any purchase over $50, wait 24 hours. Most impulse urges fade, protecting your profit margins.

- Shop with a List: Never enter a grocery store without a plan. This prevents high-margin “impulse” buys that stores use to drain your wallet.

- Negotiate Fixed Bills: Call your internet or insurance provider annually. A 15-minute phone call can often save you $20–$50 per month.

- Leverage Cashback: Use apps like Rakuten for necessary purchases to create small passive income flows.

Common Mistakes to Avoid

- Being Too Restrictive: If your budget is too tight, you will “crash” and binge-spend. Allow for small rewards.

- Ignoring Small Expenses: A $5 daily latte is $1,825 a year. Small leaks sink big ships.

- Forgetting “Sinking Funds”: Don’t forget non-monthly expenses like car registration or holiday gifts. Divide these by 12 and save for them monthly.

- Lack of Transparency: If you have a partner, you must both be on board. Budgeting in isolation often leads to conflict and failure.

Long-Term Sustainability & Growth

To maintain your results, you must shift from a “saving” mindset to a “reinvestment” mindset. Once your emergency fund is full, use your extra cash to build digital income assets. Whether it’s starting a blog, investing in stocks, or a work from home consulting business, your budget provides the oxygen for these projects to grow. Revisit your budget every six months to adjust for inflation and lifestyle changes.

Conclusion

Applying these budgeting tips is the first step toward true financial freedom. By managing your money with intention, you stop being a passenger in your financial life and start becoming the pilot. Remember, a budget doesn’t tell you what you can’t do; it tells you what you can do with the money you have.

Ready to start your journey? Drop your biggest budgeting challenge in the comments! Subscribe for weekly online earnings strategies, and share your progress in our community. Download our free “First-Month Budget Template” to get started today!

Frequently Asked Questions (FAQs)

How much money can I realistically save with these budgeting tips?

Most beginners find $200 to $500 in “lost” money within their first month by simply cutting unused subscriptions and reducing dining out.

Do I need prior experience with finance?

No. Budgeting is about behavior, not math. If you can follow a basic plan, you have enough experience to succeed.

What’s the initial investment?

The initial investment is zero dollars. In fact, the goal of budgeting is to increase the amount of money you have available.

How long until I see results?

You will see a difference in your bank balance by the end of your first full month of tracking and categorizing.

Is this method still working in 2026?

Yes. While the tools (apps vs. paper) change, the mathematical principles of spending less than you earn never go out of style.

What are the risks involved?

The only risk is “budget burnout” if you are too restrictive. Balance is key to long-term sustainability.

Before you go, tap those stars!

Straightforward, no gimmicks, just solid banking advice

I clicked on this article expecting it to push some specific bank or financial product with referral links. I was pleasantly surprised. The advice was unbiased, focused on principles rather than promoting any particular institution, and gave me a clear framework to evaluate my own options. I appreciated that the article addressed the importance of FDIC insurance, automatic transfers, and goal-setting — things that seem obvious but that most people (including me) overlook. The writing was clear and concise, without the usual fluff or overly complex financial jargon. The only reason I’m giving four stars instead of five is that I would have liked even more detail on how to balance saving with paying down debt. Still, this was one of the most practical and trustworthy articles on saving I’ve read in a long time. Highly recommend.

Solid advice that cuts through the noise

I’ve been saving for years, but I kept wondering if my money was actually working as hard as it could be. There’s so much conflicting information out there — regular savings accounts, money market accounts, CDs, high-yield options — it gets confusing fast. This article did an excellent job comparing the options side by side, explaining the pros and cons of each, and helping me figure out which strategy made sense for my situation. I especially appreciated the section on the importance of emergency funds versus long-term savings, and the breakdown of how compound interest really adds up over time. I ended up moving my savings to a high-yield account and setting clearer goals. Practical, well-researched, and genuinely helpful.

Small changes, noticeable results

I’ll be honest — I clicked on this article expecting generic advice like “drive less” (thanks, captain obvious). But I was genuinely impressed. The article breaks down the actual science behind why certain habits affect fuel economy, with real numbers to back it up. I learned that my lead-foot acceleration and speeding were costing me way more than I realized. The section on vehicle maintenance was especially valuable — I didn’t know a dirty air filter could impact mileage that much. The tone was straightforward, no fluff, no upselling expensive products. Just solid, practical advice that actually works. My fuel expenses dropped by about 15% last month without me changing my overall driving needs.

Finally, practical advice that doesn’t require buying a new car

As someone who drives over 400 miles a week for work, gas expenses have been crushing my budget. I’ve read countless articles that basically just say “buy an electric vehicle” — which isn’t helpful when that’s not in my budget. This article was a game-changer. The tips were immediately actionable: combining trips, checking tire pressure (I didn’t realize how much that affects mileage!), and using gas price apps. I started implementing these suggestions last month, and I’ve already saved about $40. The writing was clear, well-organized, and respected that not everyone can just trade in their car. Highly recommend for anyone feeling the pain at the pump.

Perfect for renters who can’t install solar panels

As someone who rents an apartment, I often feel limited when it comes to making my home more energy-efficient. I can’t just install new appliances or add insulation to the walls. This article was a lifesaver because it focused on renter-friendly solutions—things like weatherstripping for doors, smart power strips, and optimizing how I use my existing appliances. The writing was straightforward and didn’t assume I owned a home. My only small critique is that I would have loved even more rent-specific examples, but overall, this was incredibly helpful. My electric bill dropped by about $15 last month!