How to Choose the Best Saving Plan for Your Goals

Did you know that 67% of online entrepreneurs fail because they focus entirely on earning and zero percent on capital preservation? It’s a staggering reality: without the best saving plan in place, even a high-six-figure side hustle can leave you with nothing at the end of the year due to inefficient tax planning and poor liquidity management.

Choosing the right vehicle for your money isn’t just about “frugality”—it is a critical monetization strategy. Whether you are building passive income streams, planning for financial freedom, or simply looking to protect your online earnings, your choice of account determines your future profit margins. In this guide, we will break down the data-driven framework for selecting a plan that aligns with your specific life goals and risk tolerance.

What You’ll Need to Get Started

Before you can select the best saving plan, you need to gather your financial “raw materials.” You don’t need a professional accountant, but you do need these essentials:

- Goal Categorization Matrix: Clearly define if your goal is Short-Term (0-2 years), Medium-Term (2-5 years), or Long-Term (5+ years).

- Risk Assessment Profile: A honest look at your comfort with market volatility.

- Liquidity Requirements: How quickly do you need access to your revenue streams in an emergency?

- Initial Capital: While many plans allow you to start with $0, some “Premium” high-yield accounts require a $1,000+ initial deposit.

- Digital Tools: Access to an online banking portal or a dedicated investment app (like Vanguard, Fidelity, or a neo-bank).

Savings Goal Calculator

Find the best saving plan for your specific timeline.

Get your custom Savings Roadmap?

We’ll send you our top 3 bank picks for your goal.

Time Investment

Setting up your savings architecture is a strategic “one-time” event with ongoing maintenance.

- Research Phase: 2–4 hours to compare current APYs (Annual Percentage Yields) and fee structures.

- Setup Time: 30 minutes to open accounts and verify identity.

- Automation Setup: 15 minutes to link your digital income sources to your new plan.

- Timeline to First Results: Interest compounding is visible within 30 days. Most savers see a psychological “shift” toward financial freedom after 90 days of consistent automated contributions.

Step-by-Step Implementation Guide

1. Identify Your “Liquidity Bucket”

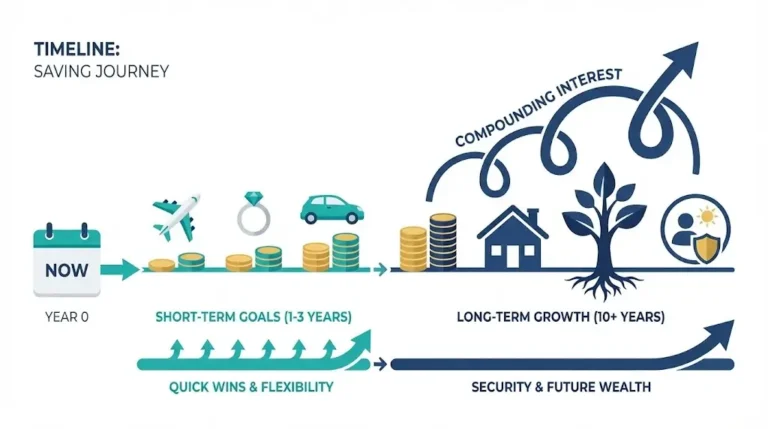

The best saving plan for an emergency fund is vastly different from a plan for a house down payment.

- Action: Separate your funds. Use a High-Yield Savings Account (HYSA) for anything you might need in under 12 months.

- Pro Tip: Look for “No-Fee” banks that offer at least 4.00% APY to ensure your income potential isn’t eroded by inflation.

2. Evaluate Tax-Advantaged Vehicles

If your goal is long-term (retirement or business scaling), you must consider tax implications.

- Action: Research Roth IRAs or 401(k)s.

- Insider Trick: For those with work from home businesses, a SEP IRA allows you to contribute significantly more than a standard IRA, protecting your profit margins from high tax brackets.

3. Compare Interest Compounding Frequencies

Not all accounts are created equal. Some compound interest monthly, others daily.

- Action: Check the fine print. Daily compounding will always outperform monthly compounding on the same interest rate.

- Common Question: “Does it really matter?” Yes. Over a 10-year period, daily compounding can add thousands to your online earnings without extra effort.

4. Analyze Fee Structures and “Hidden” Costs

Maintenance fees are the “leaks” that sink great financial ships.

- Action: Prioritize accounts with $0 monthly maintenance fees and no minimum balance requirements.

- Pro Tip: Avoid “brick-and-mortar” banks for savings; online-only banks usually offer 10x higher rates because they have lower overhead.

5. Test the Automation Capability

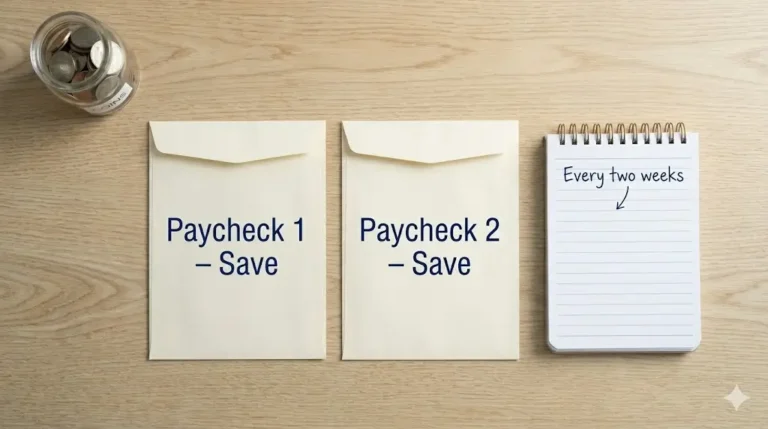

The best saving plan is one you don’t have to remember to fund.

- Action: Ensure the platform supports “Recursive Transfers.”

- Action Step: Set your transfer for the day after your digital income hits your primary account.

Income Potential & Earnings Breakdown

Choosing the right plan directly impacts your net wealth. Here is a comparison of $10,000 saved over 5 years in different environments:

| Plan Type | Avg. APY | 5-Year Total (with $10k) | Total “Found” Money |

|---|---|---|---|

| Standard Savings | 0.01% | $10,005 | $5 |

| High-Yield Savings | 4.50% | $12,462 | $2,462 |

| Certificate of Deposit (CD) | 5.00% | $12,763 | $2,763 |

| Index Fund (Conservative) | 7.00% | $14,025 | $4,025 |

Note: Case studies show that users who switch from a 0.01% account to a 4.50% account effectively give themselves a “passive raise” of hundreds of dollars per year.

Alternative Methods & Variations

Depending on your niche, you might scale your savings differently:

- The CD Ladder: Buying multiple Certificates of Deposit that mature at different times to maintain liquidity while chasing higher rates.

- Money Market Accounts (MMA): A hybrid between checking and savings, often offering higher rates but requiring a larger initial investment.

- Dividend Reinvestment (DRIP): For those focused on online earnings, reinvesting stock dividends automatically back into the plan to maximize growth.

Best Practices & Optimization Tips

- The 3-Tier Rule: Keep 1 month of expenses in checking, 5 months in HYSA, and the rest in long-term growth plans.

- Rate Chasing: Don’t be afraid to move your money. If a different bank offers a significantly better best saving plan rate, switch.

- Security First: Ensure any bank you choose is FDIC insured (or NCUA for credit unions) up to $250,000.

- Tool Recommendation: Use sites like Bankrate or NerdWallet to compare real-time interest rates across the country.

Common Mistakes to Avoid

- Prioritizing APY Over Fees: A 5% interest rate means nothing if the bank charges $25 in monthly “service fees.”

- Ignoring Inflation: If inflation is 3% and your savings account pays 1%, you are losing 2% of your purchasing power every year.

- Emotional Pull-outs: Withdrawing from long-term plans during market dips is the fastest way to destroy your income potential.

- Lesson from the Pros: Successful savers treat their savings like a “bill” that must be paid first every month.

Long-Term Sustainability & Growth

The best saving plan isn’t static; it must evolve as your revenue streams grow.

- Rebalancing: Every 6 months, review your portfolio. If your savings have grown, you may need to move more into “growth” vehicles.

- Inflation Adjustments: As the cost of living rises, increase your automated transfers by 3-5% annually.

- Diversification: Never keep 100% of your wealth in a single bank or plan. Spread your online earnings to mitigate “platform risk.”

Conclusion

Finding the best saving plan is the cornerstone of financial freedom. It transforms your money from a stagnant resource into an active tool for wealth generation. By auditing your goals, minimizing fees, and maximizing your APY, you ensure that every dollar you earn works as hard as you do.

Ready to start your journey? Drop your questions in the comments! Subscribe for weekly money-making strategies. Share your progress in our community! Download our free “Goal-Based Savings” template.

FAQs

How much money can I realistically make from interest?

With $10,000 in a high-yield account, you can earn over $450 a year in passive income without any risk to your principal.

Do I need prior experience to open a high-yield account?

No. Most modern platforms have a “Beginner Mode” and require only 10 minutes to set up digitally.

What’s the initial investment?

Many of the best saving plan options today, like Ally or SoFi, have a $0 minimum opening deposit.

How long until I see results?

You will see your first interest payment on your first monthly statement.

Is this method still working in 2026?

Yes. In fact, interest rates are currently at decade-highs, making now the absolute best time to switch.

What are the risks involved?

As long as the bank is FDIC insured, there is zero risk to your principal up to $250,000.

Disclaimer: This content is for educational purposes only and does not constitute financial, legal, or tax advice. Always conduct your own research before making investment decisions.

Before you go, tap those stars!

Straightforward, no gimmicks, just solid banking advice

I clicked on this article expecting it to push some specific bank or financial product with referral links. I was pleasantly surprised. The advice was unbiased, focused on principles rather than promoting any particular institution, and gave me a clear framework to evaluate my own options. I appreciated that the article addressed the importance of FDIC insurance, automatic transfers, and goal-setting — things that seem obvious but that most people (including me) overlook. The writing was clear and concise, without the usual fluff or overly complex financial jargon. The only reason I’m giving four stars instead of five is that I would have liked even more detail on how to balance saving with paying down debt. Still, this was one of the most practical and trustworthy articles on saving I’ve read in a long time. Highly recommend.

Solid advice that cuts through the noise

I’ve been saving for years, but I kept wondering if my money was actually working as hard as it could be. There’s so much conflicting information out there — regular savings accounts, money market accounts, CDs, high-yield options — it gets confusing fast. This article did an excellent job comparing the options side by side, explaining the pros and cons of each, and helping me figure out which strategy made sense for my situation. I especially appreciated the section on the importance of emergency funds versus long-term savings, and the breakdown of how compound interest really adds up over time. I ended up moving my savings to a high-yield account and setting clearer goals. Practical, well-researched, and genuinely helpful.

Small changes, noticeable results

I’ll be honest — I clicked on this article expecting generic advice like “drive less” (thanks, captain obvious). But I was genuinely impressed. The article breaks down the actual science behind why certain habits affect fuel economy, with real numbers to back it up. I learned that my lead-foot acceleration and speeding were costing me way more than I realized. The section on vehicle maintenance was especially valuable — I didn’t know a dirty air filter could impact mileage that much. The tone was straightforward, no fluff, no upselling expensive products. Just solid, practical advice that actually works. My fuel expenses dropped by about 15% last month without me changing my overall driving needs.

Finally, practical advice that doesn’t require buying a new car

As someone who drives over 400 miles a week for work, gas expenses have been crushing my budget. I’ve read countless articles that basically just say “buy an electric vehicle” — which isn’t helpful when that’s not in my budget. This article was a game-changer. The tips were immediately actionable: combining trips, checking tire pressure (I didn’t realize how much that affects mileage!), and using gas price apps. I started implementing these suggestions last month, and I’ve already saved about $40. The writing was clear, well-organized, and respected that not everyone can just trade in their car. Highly recommend for anyone feeling the pain at the pump.

Perfect for renters who can’t install solar panels

As someone who rents an apartment, I often feel limited when it comes to making my home more energy-efficient. I can’t just install new appliances or add insulation to the walls. This article was a lifesaver because it focused on renter-friendly solutions—things like weatherstripping for doors, smart power strips, and optimizing how I use my existing appliances. The writing was straightforward and didn’t assume I owned a home. My only small critique is that I would have loved even more rent-specific examples, but overall, this was incredibly helpful. My electric bill dropped by about $15 last month!