Smart Strategies for Finding the Best Place to Save Money

Did you know that over 67% of aspiring online entrepreneurs fail simply because they skip one crucial financial step? They focus entirely on generating revenue but completely ignore where they store their initial capital. If you are serious about achieving financial freedom, understanding the best place to save money isn’t just a defensive financial move—it is your very first monetization strategy.

Whether you are saving up to launch a new side hustle, building an emergency fund for your transition to a work from home lifestyle, or simply looking to combat inflation, letting your cash sit in a traditional checking account is a massive missed opportunity. In this guide, we will break down the exact strategies you need to find the optimal home for your cash, turning dormant funds into your first reliable source of passive income.

What You’ll Need to Get Started

Before you can start maximizing your online earnings through smart saving, you need to gather a few essential tools. The good news? The barrier to entry is practically non-existent.

- Initial Capital: $0 to $100. Many of the top-tier online platforms require no minimum deposit to open an account.

- A Financial Snapshot: A clear understanding of your current monthly expenses and disposable income. (Free tools like Rocket Money or EveryDollar can help).

- A Valid ID and Bank Account: You will need a government-issued ID and an existing checking account to link for electronic transfers.

- Research Tools: Bookmarks for financial comparison sites (like Bankrate or NerdWallet) to monitor shifting interest rates.

- The Right Mindset: You don’t need to be a Wall Street expert. The only skill required is the discipline to automate your deposits and leave the funds alone to grow.

Savings Opportunity Calculator

See how much more you could earn by switching to a High-Yield account today.

By following the steps in this article, you would earn $0.00 more than staying with a traditional bank (0.01% APY).

Want a custom savings roadmap?

Enter your email and we’ll send you our “Best Place to Save” checklist.

Time Investment

Unlike building a complex digital income business from scratch, optimizing your savings is one of the most time-efficient financial moves you can make.

- Setup Time: 15 to 30 minutes. Opening an account and linking your funding source is entirely digital and nearly instantaneous.

- Daily/Weekly Commitment: 0 hours. Once automated, this is a true “set and forget” strategy.

- Timeline to First Earnings: Most users see their first interest payout within 30 days of their initial deposit.

- The Reality Check: While you will see results in the first month, the true magic of compound interest reveals itself over 60 to 90 days and beyond. Compared to traditional active income methods, the time-to-reward ratio here is unbeatable.

Step-by-Step Implementation Guide

Finding the best place to save money requires a systematic approach. Follow these actionable steps to set up your automated wealth-building system.

Step 1: Audit Your Current Profit Margins

Before moving your money, you need to know exactly what you are currently earning. Log into your primary bank account and check your Annual Percentage Yield (APY). If you are at a traditional brick-and-mortar bank, you are likely earning a dismal 0.01%. Acknowledging this “leak” in your potential income is the first step toward optimization.

- Pro Tip: Calculate how much money you are losing to inflation by keeping your funds in a standard account. Use an online inflation calculator to see the real purchasing power of your money decreasing.

Step 2: Compare High-Yield Alternatives

Now it is time to shop for a new home for your funds. High-Yield Savings Accounts (HYSAs) offered by online banks typically provide rates 10x to 15x higher than traditional banks because they lack the overhead of physical branches.

- Look for accounts offering competitive APYs, zero monthly maintenance fees, and FDIC insurance.

Step 3: Establish Your “Side Hustle” Fund

Open your chosen account online. During setup, name the account something motivating, such as “Business Capital,” “Financial Freedom Fund,” or “Tax Buffer.” Mentally separating this money from your daily spending is crucial for long-term success.

Step 4: Automate Your Revenue Streams

The secret to consistent growth is automation. Set up an automatic transfer from your checking account to your new savings account on the day you get paid. Even $25 a week adds up significantly when enhanced by compound interest.

Income Potential & Earnings Breakdown

When evaluating the best place to save money, it is critical to look at the raw numbers. Here is a realistic breakdown of your income potential based on a $10,000 initial deposit over one year, highlighting why this is a foundational step for your overall monetization strategies.

| Account Type | Average APY | Monthly Earnings | Annual Passive Income |

|---|---|---|---|

| Traditional Bank Checking | 0.01% | $0.08 | $1.00 |

| Traditional Savings | 0.40% | $3.33 | $40.00 |

| Online HYSA | 4.50% | $37.50 | $450.00 |

| Certificate of Deposit (CD) | 5.00% | $41.66 | $500.00 |

Disclaimer: Interest rates fluctuate based on federal policies. These numbers are projections based on historical averages and do not guarantee future returns. Always read the terms of your specific financial institution.

Alternative Methods & Variations

If you want to diversify your approach, a standard HYSA isn’t the only option. Depending on your risk tolerance and liquidity needs, consider these alternatives:

- Certificates of Deposit (CDs): If you don’t need access to your money for 6 to 12 months, locking it in a CD often secures a slightly higher, fixed interest rate.

- Money Market Accounts (MMAs): These act as a hybrid between checking and savings, often providing debit cards or check-writing privileges while still offering higher yields.

- Treasury Bills (T-Bills): Backed by the US government, these short-term securities can offer highly competitive rates and are exempt from state and local taxes—a great optimization trick for high-earners.

- Rewards Checking Accounts: Some online banks offer high yields on checking accounts if you meet certain criteria, like a minimum number of debit card transactions per month.

Best Practices & Optimization Tips

To truly maximize your savings and accelerate your path to digital income, implement these best practices:

- Chase the Bonus, Not Just the Rate: Many online banks offer cash bonuses ($100 to $300+) just for opening an account and setting up direct deposit. This is an instant boost to your profit margins.

- Create Sinking Funds: Don’t just have one generic savings account. Use platforms like Ally Bank that allow you to create distinct “buckets” for different goals (e.g., Taxes, Emergency, New Laptop).

- Review Quarterly: The institution that was the best place to save money in January might not be the best in October. Set a calendar reminder every three months to ensure your APY remains competitive.

Common Mistakes to Avoid

Even the most well-intentioned savers fall into traps that stunt their financial growth. Avoid these common pitfalls:

- Locking Up Your Emergency Fund: Never put your 3-6 month emergency fund into a long-term CD or investment account. You need instant liquidity if a crisis hits. Keep this strictly in a HYSA.

- Ignoring Account Fees: A 5% APY means nothing if the bank charges a $15 monthly maintenance fee. Always read the fine print to ensure you are selecting fee-free options.

- Chasing Unsustainable Yields: Beware of unregulated platforms (like certain crypto-staking services) offering 15%+ returns. High reward always equals high risk. Keep your core savings safe.

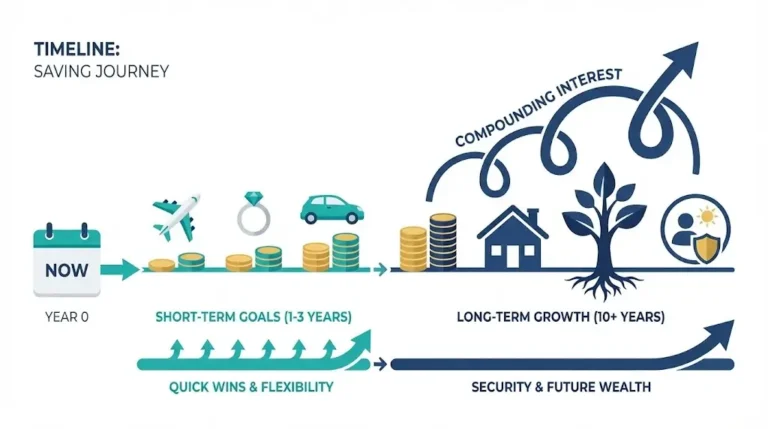

Long-Term Sustainability & Growth

Once you have optimized where your cash lives, how do you maintain and scale this momentum?

The goal is to use your optimized savings account as a launchpad. As your account generates passive income, reinvest those earnings into higher-leverage opportunities. Use the interest to buy a course on digital marketing, upgrade your software tools, or fund the initial ad spend for a new work from home business. By treating your savings account as a dynamic tool rather than a static vault, you future-proof your finances and build multiple resilient income streams.

Conclusion

Finding the best place to save money is the easiest, most accessible way to begin generating a return on your capital. By moving away from traditional banks, utilizing high-yield online alternatives, and automating your deposits, you set a rock-solid foundation for all your future online earnings.

Ready to start your journey toward financial optimization? Drop your questions about High-Yield Savings Accounts in the comments below! Don’t forget to subscribe to our newsletter for weekly money-making strategies, and share your progress in our community forums.

FAQs

How much money can I realistically make from a high-yield savings account?

Your earnings depend entirely on your deposit amount and the current APY. For example, a $5,000 balance in an account with a 4.5% APY will generate roughly $225 in passive income over a year. It won’t make you a millionaire overnight, but it protects your cash from inflation.

What’s the initial investment required?

Most modern online banks have removed their barrier to entry. You can typically open an account with as little as $0 to $1, though you will need to deposit funds to start earning interest.

How long until I see results?

Interest typically accrues daily and is paid out monthly. You will see your first dividend payment within 30 days of funding your account.

Is this method still working in the current year?

Yes. As long as central banks maintain competitive interest rates, High-Yield Savings Accounts and CDs remain one of the most reliable, zero-effort ways to grow your money safely.

What are the risks involved?

As long as you choose an institution that is FDIC-insured (or NCUA-insured for credit unions), your money is protected up to $250,000 per depositor. The only real “risk” is that variable APY rates may decrease if federal interest rates drop.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice. Always conduct your own research or consult with a certified financial planner before making financial decisions.

Before you go, tap those stars!

Straightforward, no gimmicks, just solid banking advice

I clicked on this article expecting it to push some specific bank or financial product with referral links. I was pleasantly surprised. The advice was unbiased, focused on principles rather than promoting any particular institution, and gave me a clear framework to evaluate my own options. I appreciated that the article addressed the importance of FDIC insurance, automatic transfers, and goal-setting — things that seem obvious but that most people (including me) overlook. The writing was clear and concise, without the usual fluff or overly complex financial jargon. The only reason I’m giving four stars instead of five is that I would have liked even more detail on how to balance saving with paying down debt. Still, this was one of the most practical and trustworthy articles on saving I’ve read in a long time. Highly recommend.

Solid advice that cuts through the noise

I’ve been saving for years, but I kept wondering if my money was actually working as hard as it could be. There’s so much conflicting information out there — regular savings accounts, money market accounts, CDs, high-yield options — it gets confusing fast. This article did an excellent job comparing the options side by side, explaining the pros and cons of each, and helping me figure out which strategy made sense for my situation. I especially appreciated the section on the importance of emergency funds versus long-term savings, and the breakdown of how compound interest really adds up over time. I ended up moving my savings to a high-yield account and setting clearer goals. Practical, well-researched, and genuinely helpful.

Small changes, noticeable results

I’ll be honest — I clicked on this article expecting generic advice like “drive less” (thanks, captain obvious). But I was genuinely impressed. The article breaks down the actual science behind why certain habits affect fuel economy, with real numbers to back it up. I learned that my lead-foot acceleration and speeding were costing me way more than I realized. The section on vehicle maintenance was especially valuable — I didn’t know a dirty air filter could impact mileage that much. The tone was straightforward, no fluff, no upselling expensive products. Just solid, practical advice that actually works. My fuel expenses dropped by about 15% last month without me changing my overall driving needs.

Finally, practical advice that doesn’t require buying a new car

As someone who drives over 400 miles a week for work, gas expenses have been crushing my budget. I’ve read countless articles that basically just say “buy an electric vehicle” — which isn’t helpful when that’s not in my budget. This article was a game-changer. The tips were immediately actionable: combining trips, checking tire pressure (I didn’t realize how much that affects mileage!), and using gas price apps. I started implementing these suggestions last month, and I’ve already saved about $40. The writing was clear, well-organized, and respected that not everyone can just trade in their car. Highly recommend for anyone feeling the pain at the pump.

Perfect for renters who can’t install solar panels

As someone who rents an apartment, I often feel limited when it comes to making my home more energy-efficient. I can’t just install new appliances or add insulation to the walls. This article was a lifesaver because it focused on renter-friendly solutions—things like weatherstripping for doors, smart power strips, and optimizing how I use my existing appliances. The writing was straightforward and didn’t assume I owned a home. My only small critique is that I would have loved even more rent-specific examples, but overall, this was incredibly helpful. My electric bill dropped by about $15 last month!