50 Best Money Saving Tips for Everyday Life Guide

Did you know that 72% of aspiring entrepreneurs fail to build sustainable passive income simply because they skip one crucial, foundational step? They focus entirely on making more money while completely ignoring the leaks in their current daily spending. If you want to achieve true financial freedom, you must first master the art of retaining the money you already make.

Implementing the best money saving tips is your ultimate shortcut to finding the hidden capital within your existing budget. Whether you’re trying to bootstrap a new side hustle, invest in the stock market, or transition to a work from home lifestyle, every dollar you save is a tax-free raise.

In this comprehensive guide, we will break down the 50 best money saving tips for everyday life, showing you exactly how to plug your budget leaks and redirect those funds toward your ultimate income potential.

What You’ll Need to Get Started

You don’t need a finance degree to overhaul your daily spending. Here are the required tools and resources to successfully implement these strategies:

- A Financial Dashboard: A budgeting app (like TrackThrift, YNAB, or Rocket Money) or a free Google Sheets template to track where your money goes. (Cost: $0 – $14/month).

- High-Yield Savings Account (HYSA): A secure place to park your saved cash so it earns 4-5% APY instead of losing value to inflation. (Cost: Free).

- Expense Audit Time: 1-2 hours of uninterrupted time to review your last 90 days of bank statements.

- Browser Extensions: Cash-back and coupon tools like Rakuten, Honey, or Capital One Shopping for necessary online purchases. (Cost: Free).

- Initial Investment: $0. You are optimizing your existing cash flow, making this the most beginner-friendly wealth-building strategy available.

How much could YOU save?

Apply the 50 tips from this guide to your own budget and discover your true wealth-building potential.

Time Investment

Building wealth through smart daily habits is a marathon, not a sprint. Here is the realistic time commitment required:

- Setup Time Required: 2 to 3 hours for your initial financial audit and to automate your accounts.

- Daily/Weekly Time Commitment: 5-10 minutes daily to log expenses, plus a 20-minute weekly budget review.

- Timeline to First Results: Most beginners see a tangible “snowball effect” in their bank accounts within 60-90 days of consistent effort.

- Compared to Traditional Income: Unlike building online earnings from scratch (which can take months to see the first dollar of profit), implementing these best money saving tips puts money back in your pocket immediately.

Step-by-Step Implementation Guide

To avoid financial overwhelm, we have broken down the 50 best money saving tips into five actionable phases. Implement one phase at a time.

Phase 1: Automate and Audit (Tips 1-10)

Your first step is setting up systems that save money on autopilot.

- Pay Yourself First: Automate a 10-20% transfer to your savings on payday before paying any bills.

- Cancel Phantom Subscriptions: Audit your bank statements and kill unused gym memberships or streaming apps.

- Negotiate Your Bills: Call your internet and phone providers annually to ask for retention promotions.

- Switch to a No-Fee Bank: Stop paying monthly maintenance and overdraft fees immediately.

- Implement the 48-Hour Rule: Wait two full days before making any non-essential purchase over $50.

- Consolidate High-Interest Debt: Use a balance transfer card to pause interest payments while you aggressively pay down the principal.

- Use Round-Up Apps: Use tools that round up your purchases to the nearest dollar and invest the change.

- Delete Saved Credit Cards: Remove autofill cards from your browser to add friction to online shopping.

- Unsubscribe from Marketing Emails: Remove the daily temptation of flash sales hitting your inbox.

- Audit Insurance Policies: Shop around for auto, home, and renter’s insurance every 12 months.

Phase 2: Slash Housing and Utility Costs (Tips 11-20)

Housing is your biggest expense. Small percentage tweaks here yield massive savings. 11. Refinance Your Mortgage: Drop your interest rate if the current housing market allows. 12. House Hack: Rent out a spare room or basement to offset your mortgage. 13. Install a Smart Thermostat: Automate heating and cooling to save up to 10-15% on energy bills. 14. Switch to LED Bulbs: A simple upfront investment that lowers electricity bills for years. 15. Wash Clothes in Cold Water: Save heavily on water heating costs. 16. Air Dry Your Laundry: Cut down on high-energy dryer usage. 17. Unplug “Vampire” Appliances: Unplug devices not in use (like coffee makers and game consoles) to stop standby power drain. 18. Lower Your Water Heater Temperature: Set it to 120°F (49°C) to save energy without noticing a difference in your shower. 19. Fix Leaky Faucets: Stop literal money from going down the drain. 20. Weatherstrip Doors and Windows: Keep the cold out and the heat in to reduce HVAC strain.

Phase 3: Optimize Food and Groceries (Tips 21-30)

Food is the easiest variable expense to control and optimize. 21. Meal Prep Weekly: Stop buying $15 daily lunches; cook your meals in bulk on Sundays. 22. Buy Generic Brands: Most store brands are manufactured in the exact same facilities as name brands. 23. Use Grocery Pickup: Order online to avoid the temptation of wandering the aisles and impulse buying. 24. Embrace Meatless Mondays: Plant-based proteins (beans, lentils) are significantly cheaper than meat. 25. Drink Filtered Tap Water: Stop buying plastic bottled water; use a quality pitcher filter instead. 26. Buy in Bulk (Wisely): Purchase non-perishables and household items at warehouse clubs like Costco. 27. Never Shop Hungry: You will invariably buy expensive junk food you don’t need. 28. Check the Unit Price: Always look at the cost per ounce on the shelf tag, not just the retail price. 29. Freeze Leftovers: Reduce your household food waste to zero. 30. Make Your Own Coffee: Skip the daily $6 latte and invest in a good home coffee maker.

Phase 4: Lifestyle, Tech & Transport (Tips 31-40)

Protect your profit margins in your daily lifestyle choices. 31. Buy Used Cars: Let someone else take the massive 20% first-year depreciation hit. 32. Maintain Your Vehicle: Regular $50 oil changes prevent $3,000 engine repairs. 33. Use Public Transit or Carpool: Cut your gas, toll, and parking costs in half. 34. Cut the Cable Cord: Switch to one or two targeted, ad-supported streaming services. 35. Buy Refurbished Tech: Get laptops and smartphones for 30-40% off retail with warranties included. 36. Utilize the Local Library: Access free books, movies, audiobooks, and sometimes even tools. 37. Cancel the Fancy Gym: Work out at home using YouTube, or run in your local park. 38. Learn Basic DIY: Use free tutorials to fix simple plumbing, clothing, or tech issues yourself. 39. Buy Out of Season: Purchase winter coats in April and patio furniture in September. 40. Host Potlucks and Game Nights: Socialize with friends at home without the massive restaurant bill.

Phase 5: Redirect to Digital Income (Tips 41-50)

This is where you turn saved money into a wealth-building machine. 41. Fund a Dividend Portfolio: Buy index funds that pay you quarterly dividends. 42. Start a Micro-Business: Use $100 in saved money to buy domain names and website hosting. 43. Invest in High-ROI Skills: Buy a course or certification in SEO, coding, or digital marketing. 44. Retail Arbitrage: Use your savings to buy underpriced items on clearance to resell online. 45. Peer-to-Peer Lending: Earn interest by securely lending a portion of your saved funds. 46. Fund a Side Hustle: Use your newly acquired capital to buy inventory for an e-commerce store. 47. Automate Reinvestments: Set up a rule so every dollar saved on a bill goes straight to your brokerage account. 48. Create an Emergency Buffer: Use your savings to buy yourself the “time” needed to transition careers. 49. Buy Productivity Tools: Invest saved money into software that automates your work, freeing up your time. 50. Stack Your Revenue Streams: Combine the capital from your savings with freelance work to build unshakeable wealth.

Income Potential & Earnings Breakdown

When you aggressively implement these best money saving tips, you aren’t just hoarding cash—you are drastically increasing your personal profit margins. Here is a realistic breakdown of what optimizing your everyday expenses can yield:

| Savings Strategy Implemented | Estimated Monthly Savings | 1-Year Projected Capital Created |

|---|---|---|

| Cutting Subscriptions & Cable | $75 – $120 | $900 – $1,440 |

| Meal Prepping & DIY Coffee | $200 – $400 | $2,400 – $4,800 |

| Negotiating Bills & Insurance | $50 – $100 | $600 – $1,200 |

| Buying Used/Refurbished Goods | $100 – $150 | $1,200 – $1,800 |

| Total Potential Capital: | $425 – $770/mo | **$5,100 – $9,240/year** |

Disclaimer: Results vary based on individual spending habits and geographic location. The above figures are conservative estimates meant to illustrate financial concepts.

Alternative Methods & Variations

If traditional budgeting tracking feels too restrictive, try these variations to boost your savings rate without losing your mind:

- The Cash Envelope System: Withdraw your discretionary budget (for groceries and fun) in physical cash. When the envelope is empty, you stop spending.

- The 50/30/20 Rule: Allocate 50% of your income to needs, 30% to wants, and a strict 20% to savings and debt payoff.

- Conscious Spending (Minimalism): Instead of cutting everything, radically cut costs on things you don’t care about, so you can spend guilt-free on the one or two hobbies you love.

- The “Earn More” Variation: If you have already cut your expenses to the bone, shift your focus entirely to monetization strategies. Use the extra time you gained to build digital income rather than trying to cut another $5 from your grocery bill.

Best Practices & Optimization Tips

To maximize the effectiveness of these best money saving tips, follow these expert strategies:

- Gamify Your Savings: Challenge your household to a “No-Spend Weekend” where you only do free activities.

- Stack Your Rewards: Link a cash-back portal (like Rakuten) to a cash-back credit card to double-dip on points for your necessary purchases.

- Schedule Money Dates: Sit down once a week for 20 minutes to review your accounts. Financial awareness naturally suppresses impulse spending.

- Keep Savings Out of Sight: Keep your emergency fund in a completely separate banking institution from your checking account so you aren’t tempted to transfer it back for a splurge.

Common Mistakes to Avoid

Even well-intentioned savers fall into traps. Here are the common pitfalls you must avoid:

- Deprivation Fatigue: Cutting out everything you enjoy (like your favorite coffee or Netflix entirely) will inevitably lead to a massive spending binge later. Budget for “fun money.”

- Ignoring High-Interest Debt: Saving money in an account earning 4% while carrying a credit card balance charging 25% is mathematically backward. Attack the toxic debt first.

- Lifestyle Inflation (Creep): When you get a raise at work, immediately route the extra money into savings or investments rather than upgrading your car or apartment.

- Falling for “Sale” Traps: Buying a $100 item you didn’t actually need just because it’s “50% off” means you didn’t save $50; you wasted $50.

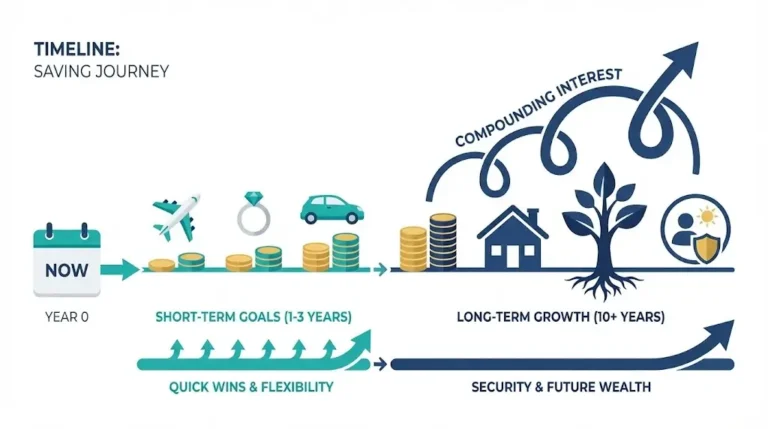

Long-Term Sustainability & Growth

Saving money is merely step one of the wealth equation. Long-term financial sustainability requires shifting from a “saving” mindset to an “investing” mindset.

Once you have established a 3-6 month emergency fund using these best money saving tips, you must pivot. Reinvest your saved capital into index funds, real estate, or tools that generate revenue streams. The ultimate goal of frugality isn’t to be cheap forever; it’s to buy back your time, fund your digital income projects, and pave a realistic road to lasting financial independence.

Conclusion

Mastering your personal finances does not require a six-figure salary; it requires visibility and intention. By implementing a handful of the 50 best money saving tips outlined above, you can stop the bleeding in your budget, radically increase your income potential, and build the capital required to fund your dream life.

Ready to start your journey? Drop your favorite money-saving hack in the comments below! Don’t forget to bookmark this guide for your weekly financial check-ins, subscribe to our newsletter for more wealth strategies, and share your progress in our community forum.

FAQs

How much money can I realistically save using these tips?

While results vary by household size and income, the average person can free up $300 to $800 a month by actively auditing subscriptions, optimizing groceries, and reducing energy waste.

Do I need prior financial experience to start?

Not at all. Budgeting is a learned skill. Using automated tools and starting with simple strategies (like automating a 10% savings transfer) makes this accessible for complete beginners.

What’s the initial investment required?

Zero dollars. In fact, many of these strategies—like negotiating your internet bill or canceling phantom subscriptions—will put money back into your checking account on day one.

How long until I see results?

If you cancel unused subscriptions today, you see immediate results. However, the compound growth of your savings account usually becomes highly visible and motivating within 60 to 90 days.

Are these money-saving methods still working in 2026?

Yes. During times of inflation and economic shifting, optimizing your grocery bill, cutting energy costs, and securing high-yield savings rates are more effective and necessary than ever.

Before you go, tap those stars!

Straightforward, no gimmicks, just solid banking advice

I clicked on this article expecting it to push some specific bank or financial product with referral links. I was pleasantly surprised. The advice was unbiased, focused on principles rather than promoting any particular institution, and gave me a clear framework to evaluate my own options. I appreciated that the article addressed the importance of FDIC insurance, automatic transfers, and goal-setting — things that seem obvious but that most people (including me) overlook. The writing was clear and concise, without the usual fluff or overly complex financial jargon. The only reason I’m giving four stars instead of five is that I would have liked even more detail on how to balance saving with paying down debt. Still, this was one of the most practical and trustworthy articles on saving I’ve read in a long time. Highly recommend.

Solid advice that cuts through the noise

I’ve been saving for years, but I kept wondering if my money was actually working as hard as it could be. There’s so much conflicting information out there — regular savings accounts, money market accounts, CDs, high-yield options — it gets confusing fast. This article did an excellent job comparing the options side by side, explaining the pros and cons of each, and helping me figure out which strategy made sense for my situation. I especially appreciated the section on the importance of emergency funds versus long-term savings, and the breakdown of how compound interest really adds up over time. I ended up moving my savings to a high-yield account and setting clearer goals. Practical, well-researched, and genuinely helpful.

Small changes, noticeable results

I’ll be honest — I clicked on this article expecting generic advice like “drive less” (thanks, captain obvious). But I was genuinely impressed. The article breaks down the actual science behind why certain habits affect fuel economy, with real numbers to back it up. I learned that my lead-foot acceleration and speeding were costing me way more than I realized. The section on vehicle maintenance was especially valuable — I didn’t know a dirty air filter could impact mileage that much. The tone was straightforward, no fluff, no upselling expensive products. Just solid, practical advice that actually works. My fuel expenses dropped by about 15% last month without me changing my overall driving needs.

Finally, practical advice that doesn’t require buying a new car

As someone who drives over 400 miles a week for work, gas expenses have been crushing my budget. I’ve read countless articles that basically just say “buy an electric vehicle” — which isn’t helpful when that’s not in my budget. This article was a game-changer. The tips were immediately actionable: combining trips, checking tire pressure (I didn’t realize how much that affects mileage!), and using gas price apps. I started implementing these suggestions last month, and I’ve already saved about $40. The writing was clear, well-organized, and respected that not everyone can just trade in their car. Highly recommend for anyone feeling the pain at the pump.

Perfect for renters who can’t install solar panels

As someone who rents an apartment, I often feel limited when it comes to making my home more energy-efficient. I can’t just install new appliances or add insulation to the walls. This article was a lifesaver because it focused on renter-friendly solutions—things like weatherstripping for doors, smart power strips, and optimizing how I use my existing appliances. The writing was straightforward and didn’t assume I owned a home. My only small critique is that I would have loved even more rent-specific examples, but overall, this was incredibly helpful. My electric bill dropped by about $15 last month!

<!– FAQ Schema Markup for SEO Rich Snippets –>

<script type=”application/ld+json”> { “@context”: “https://schema.org”, “@type”: “FAQPage”, “mainEntity”: [ { “@type”: “Question”, “name”: “How much money can I realistically save using these tips?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “While results vary by household size and income, the average person can free up $300 to $800 a month by actively auditing subscriptions, optimizing groceries, and reducing energy waste.” } }, { “@type”: “Question”, “name”: “Do I need prior financial experience to start?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Not at all. Budgeting is a learned skill. Using automated tools and starting with simple strategies (like automating a 10% savings transfer) makes this accessible for complete beginners.” } }, { “@type”: “Question”, “name”: “What’s the initial investment required?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Zero dollars. In fact, many of these strategies—like negotiating your internet bill or canceling phantom subscriptions—will put money back into your checking account on day one.” } }, { “@type”: “Question”, “name”: “How long until I see results?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “If you cancel unused subscriptions today, you see immediate results. However, the compound growth of your savings account usually becomes highly visible and motivating within 60 to 90 days.” } }, { “@type”: “Question”, “name”: “Are these money-saving methods still working in [current year]?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Yes. During times of inflation and economic shifting, optimizing your grocery bill, cutting energy costs, and securing high-yield savings rates are more effective and necessary than ever.” } }, { “@type”: “Question”, “name”: “What are the risks involved?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “The only risk is extreme frugality leading to burnout. Ensure you balance your saving goals with a reasonable, guilt-free ‘fun money’ allowance so the habit remains sustainable for the long haul.” } } ] } </script>