Choosing the Best App for Managing Money: A Complete Guide

Did you know that 74% of Americans admit to struggling with money management, and over 60% are currently living paycheck to paycheck? Many aspiring online entrepreneurs fail to launch their digital ventures not because their ideas are bad, but because they lack the initial cash flow to fund them. If you want to achieve true financial freedom, you cannot skip the foundational step of tracking your capital. Finding the best app for managing money is the crucial first move to plugging the leaks in your budget. By taking control of your personal finances, you instantly free up the seed money required to build a side hustle, invest in passive income, and ultimately transform your financial trajectory.

Quick Answer

The most effective way to optimize your finances is by using a zero-based budgeting tool like YNAB (You Need A Budget), Empower, or Monarch Money. These platforms automatically sync with your bank accounts, categorize your spending in real-time, and help you identify the hidden cash you need to fund future investments.

The “Hidden Money” Calculator

How much could a money management app recover for you? Enter your estimated monthly habits below.

You could be saving an extra:

$0

per month (That’s $0 a year!)

Ready to stop guessing and start tracking?

A budget isn’t a restriction; it’s a tool to find hidden cash. Don’t let another month of savings slip through the cracks. Visit our partner web app to take full control of your finances today.

What You’ll Need to Get Started

You do not need a degree in finance to start treating your personal bank account like a profitable business. Here is exactly what you need to begin optimizing your money:

- A Smart Device: A smartphone or laptop (mobile apps currently dominate 72% of the financial tracking market).

- Active Bank Accounts: Your primary checking, savings, and any credit card accounts.

- A Budgeting Application: Free options like EveryDollar or premium tools like YNAB ($14.99/month) and Monarch Money.

- Initial Investment: $0 to start. Most premium apps offer a 30-day free trial.

- Clear Financial Goals: Know why you are tracking your money (e.g., saving $500 to start a work from home business).

Time Investment

The “Budget App Paradox” is that people think tracking money takes hours. With modern software, the heavy lifting is completely automated.

- Setup Time Required: 45 to 60 minutes to link your bank accounts, set up categories, and establish your baseline budget.

- Daily/Weekly Time Commitment: Just 2 to 5 minutes a day. Nearly 80% of successful app users check their balances weekly to categorize transactions.

- Timeline to First Results: Most beginners see a significant cash flow improvement in 30 to 60 days. Within this timeframe, you will spot unused subscriptions and impulse buys, instantly boosting your personal profit margins.

- Compared to Traditional Earning: Earning an extra $100 online might take 5 hours of freelance work. Finding $100 by managing your money through an app takes 5 minutes.

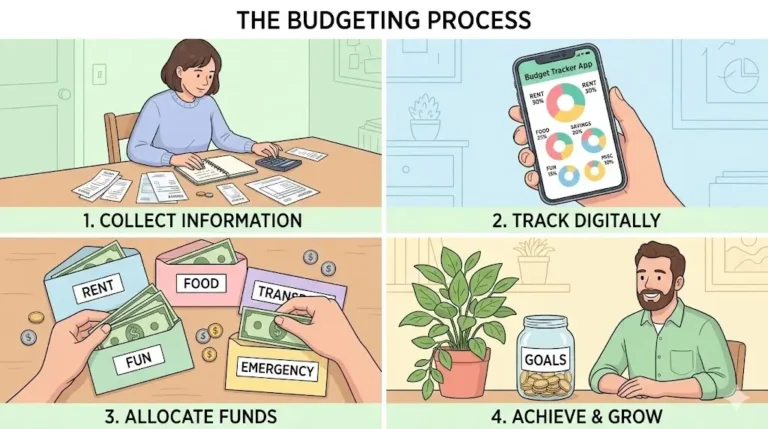

Step-by-Step Implementation Guide

1. Identify Your Financial Objective

Before downloading anything, define your goal. Are you trying to track digital income from a new venture? Are you trying to cut expenses to fund a side hustle? Your goal determines your tool. For strictly cutting expenses, an app like Rocket Money is ideal. For comprehensive net-worth tracking, Empower is better.

2. Select and Download the Right App

Go to your app store and download your chosen platform. If you are entirely new to budgeting, start with a zero-based budgeting app. This method ensures every single dollar is assigned a specific “job” before the month even begins, preventing accidental overspending.

3. Securely Link Your Financial Accounts

Open the app and use its secure, encrypted portal (usually powered by Plaid) to link your checking, savings, and credit cards. Pro Tip: If you have separate accounts for your online earnings, link those too, but categorize them under a “Business” or “Side Hustle” tab to keep your data organized.

4. Categorize Your Past 30 Days of Spending

Let the app analyze your last month of transactions. Group them into basic categories: Needs (Rent, Utilities), Wants (Dining out, Entertainment), and Savings/Investments. This provides a stark, honest look at your current baseline.

5. Automate and Monitor Daily

Set up push notifications for large purchases and low balances. Spend three minutes every morning reviewing the previous day’s transactions while drinking your coffee. Consistency here is the secret to increasing your income potential.

Income Potential & Earnings Breakdown

How does managing your money translate to actual earnings? In the digital economy, capital retention is just as powerful as capital generation.

- Beginner Savings (Months 1-3): $150 – $300/month reclaimed by eliminating ghost subscriptions and reducing dining out.

- Advanced Optimization (Months 3-12): $500+/month saved and redirected into income-producing assets (stocks, online businesses, certifications).

- The Compounding Effect: If an app helps you “find” $300 a month in wasted spending, and you redirect that into a business with strong profit margins, that $3,600 a year can easily become a $10,000+ annual revenue stream.

- Payment Structures: The “payout” is immediate. Money not spent is tax-free money earned.

Alternative Methods & Variations

If a comprehensive, automated app feels overwhelming, there are several variations to achieve the same financial control:

- The Spreadsheet Method: For maximum privacy and control, use a Google Sheets template. It requires manual data entry but allows infinite customization for tracking complex revenue streams.

- The Envelope System (Digital or Physical): Withdrawing cash for discretionary spending categories. When the cash is gone, you stop spending.

- Hybrid Tracking: Using a free app like EveryDollar for daily discretionary spending, while using a dashboard like Empower solely for tracking long-term investment growth.

- Banking Native Apps: Many modern digital banks (like Ally or SoFi) have built-in budgeting tools that sort your money into “buckets,” requiring zero third-party software.

Best Practices & Optimization Tips

To get the absolute highest return on investment from your financial app, implement these expert strategies:

- Create a “Side Hustle” Category: Always separate your W-2 income from your online earnings. This makes reinvesting your digital profits much simpler.

- Use the 70-20-10 Rule: Optimize your app to budget 70% of income for living expenses, 20% for debt/savings, and 10% strictly for building new monetization strategies.

- Audit Your App Quarterly: As your income grows, your budget should evolve. Don’t let lifestyle creep consume your new earnings; manually adjust your app to push excess cash into investments.

- Leverage Tax Tracking: If you work from home, use your app’s tagging feature to label internet bills, software, and home office supplies for easy tax write-offs at the end of the year.

Common Mistakes to Avoid

The failure rate for personal budgeting is surprisingly high. Avoid these critical pitfalls that derail financial progress:

- The Complexity Trap: Trying to track 45 different micro-categories (e.g., separating “Coffee” from “Fast Food”). Keep it simple: use 5 to 7 broad categories to avoid decision paralysis.

- Ignoring Cash Transactions: If you make cash purchases and fail to log them manually, your app’s data becomes inaccurate, leading to a false sense of security.

- Mixing Personal and Business Funds: This is the #1 mistake new entrepreneurs make. Never run your side hustle expenses through your personal checking account. It makes tracking your true profit margins impossible.

- Using Guilt as Motivation: If you overspend one week, don’t abandon the app. Apps are meant to be a GPS recalculating your route, not a judge punishing your mistakes.

Long-Term Sustainability & Growth

Finding the best app for managing money is only the beginning. To turn good budgeting into lasting wealth, you must focus on sustainable growth.

- Reinvesting the Surplus: The ultimate goal of your budgeting app isn’t just to save money; it’s to generate capital. Automatically sweep your end-of-month surplus into a brokerage account or a high-yield business savings account.

- Future-Proofing: As you transition from an employee to an entrepreneur, upgrade to software that handles both personal budgeting and business accounting (like QuickBooks Solopreneur).

- Automation is Key: The less you touch your money, the faster it grows. Set your app to automatically move a percentage of every paycheck into your investment accounts before you even see the balance.

Conclusion

Selecting the best app for managing money is the ultimate prerequisite for building wealth in the digital age. By securely linking your accounts, categorizing your spending, and cutting unnecessary waste, you instantly generate the seed capital needed for your next great venture. Remember, the path to financial freedom doesn’t start with making a million dollars; it starts with managing your first thousand correctly.

Ready to start your journey? Drop your favorite budgeting app or biggest financial hurdle in the comments below! Subscribe for weekly money-making strategies, and share your progress in our community to stay accountable.

FAQs

What is the best app for managing money as a beginner?

For complete beginners, YNAB (You Need A Budget) and EveryDollar are excellent because they teach the zero-based budgeting method, which forces you to be intentional with every dollar you earn.

Is it safe to link my bank account to budgeting apps?

Yes. Reputable apps use read-only, bank-level encryption (often through third-party services like Plaid). They cannot move your money; they can only read the transaction data.

How much money can I realistically save using these apps?

Users consistently report saving between $200 and $600 in their first few months simply by identifying forgotten subscriptions, negotiating bills, and curbing impulse purchases through better awareness.

Do I need prior experience to use financial software?

No prior financial experience is necessary. Modern apps are designed with intuitive, user-friendly interfaces that do the complex math for you automatically.

How long until I see results in my finances?

You will gain immediate clarity on day one. However, tangible financial results—like a growing savings account or paid-off debt—usually become highly visible within 60 to 90 days of consistent tracking.

Can I use these apps to track my side hustle or online earnings?

Absolutely. Many apps allow you to create custom categories and tags. You can tag specific deposits as “Online Earnings” and track your specific business expenses to monitor your overall profit margins.

Before you go, tap those stars!

Straightforward, no gimmicks, just solid banking advice

I clicked on this article expecting it to push some specific bank or financial product with referral links. I was pleasantly surprised. The advice was unbiased, focused on principles rather than promoting any particular institution, and gave me a clear framework to evaluate my own options. I appreciated that the article addressed the importance of FDIC insurance, automatic transfers, and goal-setting — things that seem obvious but that most people (including me) overlook. The writing was clear and concise, without the usual fluff or overly complex financial jargon. The only reason I’m giving four stars instead of five is that I would have liked even more detail on how to balance saving with paying down debt. Still, this was one of the most practical and trustworthy articles on saving I’ve read in a long time. Highly recommend.

Solid advice that cuts through the noise

I’ve been saving for years, but I kept wondering if my money was actually working as hard as it could be. There’s so much conflicting information out there — regular savings accounts, money market accounts, CDs, high-yield options — it gets confusing fast. This article did an excellent job comparing the options side by side, explaining the pros and cons of each, and helping me figure out which strategy made sense for my situation. I especially appreciated the section on the importance of emergency funds versus long-term savings, and the breakdown of how compound interest really adds up over time. I ended up moving my savings to a high-yield account and setting clearer goals. Practical, well-researched, and genuinely helpful.

Small changes, noticeable results

I’ll be honest — I clicked on this article expecting generic advice like “drive less” (thanks, captain obvious). But I was genuinely impressed. The article breaks down the actual science behind why certain habits affect fuel economy, with real numbers to back it up. I learned that my lead-foot acceleration and speeding were costing me way more than I realized. The section on vehicle maintenance was especially valuable — I didn’t know a dirty air filter could impact mileage that much. The tone was straightforward, no fluff, no upselling expensive products. Just solid, practical advice that actually works. My fuel expenses dropped by about 15% last month without me changing my overall driving needs.

Finally, practical advice that doesn’t require buying a new car

As someone who drives over 400 miles a week for work, gas expenses have been crushing my budget. I’ve read countless articles that basically just say “buy an electric vehicle” — which isn’t helpful when that’s not in my budget. This article was a game-changer. The tips were immediately actionable: combining trips, checking tire pressure (I didn’t realize how much that affects mileage!), and using gas price apps. I started implementing these suggestions last month, and I’ve already saved about $40. The writing was clear, well-organized, and respected that not everyone can just trade in their car. Highly recommend for anyone feeling the pain at the pump.

Perfect for renters who can’t install solar panels

As someone who rents an apartment, I often feel limited when it comes to making my home more energy-efficient. I can’t just install new appliances or add insulation to the walls. This article was a lifesaver because it focused on renter-friendly solutions—things like weatherstripping for doors, smart power strips, and optimizing how I use my existing appliances. The writing was straightforward and didn’t assume I owned a home. My only small critique is that I would have loved even more rent-specific examples, but overall, this was incredibly helpful. My electric bill dropped by about $15 last month!