A Comprehensive Guide to Saving for a House Deposit

Did you know that nearly 67% of prospective homebuyers feel overwhelmed and delay their homeownership dreams simply because they rely entirely on a single traditional paycheck to reach their savings goals?

In today’s shifting economic landscape, the traditional advice of just “skipping your morning coffee” is no longer enough. If you are serious about saving for a house deposit, you need a modernized approach. This isn’t just about aggressive budgeting; it’s about strategically expanding your income, leveraging digital opportunities, and ultimately achieving financial freedom faster than you thought possible. Whether you are starting from zero or halfway to your goal, this guide will show you how to combine smart savings tactics with modern online earnings to secure your dream home.

Quick Answer

To successfully save for a house deposit in today’s market, you must calculate your exact target (usually 5% to 20% of the property value), automate your monthly savings into a high-yield account, and actively accelerate your timeline by establishing a digital side hustle or alternative revenue streams.

What You’ll Need to Get Started

Before you start aggressively stashing away cash, you need the right infrastructure. Saving a massive lump sum requires more than willpower; it requires specific tools and strategies. Here is your essential starter kit:

- A High-Yield Savings Account (HYSA): Stop leaving your money in a traditional checking account earning 0.01%. Look for an HYSA offering competitive APY (Annual Percentage Yield) to let compound interest work for you. Estimated Cost: Free.

- A Dedicated Budgeting Tool: Whether it’s a free app like Mint or EveryDollar, or a customized zero-based budgeting spreadsheet, you need to track every penny. Estimated Cost: $0 – $10/month.

- Digital Skills for a Side Hustle: To accelerate your deposit, you’ll need a marketable skill. Think freelance writing, graphic design, virtual assistance, or digital marketing. Beginner-friendly alternatives: taking online surveys, virtual data entry, or participating in the gig economy.

- Clear Financial Goals: You need a concrete number. Knowing whether you need $15,000 or $50,000 dictates your entire strategy.

Time Investment

Building a house deposit is a marathon, not a sprint, but your timeline heavily depends on your strategy.

- Initial Setup Time: 3 to 5 hours to audit your finances, set up your budgeting tools, and open your high-yield savings accounts.

- Daily/Weekly Commitment: 15 minutes a day for expense tracking, plus 10–15 hours a week dedicated to a side hustle or building passive income streams to accelerate your goal.

- Timeline to First Earnings (Side Hustles): If you leverage work from home opportunities like freelancing, most beginners see their first digital income within 30 to 60 days of consistent effort.

- Timeline to Goal: Depending on your target home price and your ability to scale your income potential, saving for a house deposit typically takes the average buyer 2 to 5 years. However, adding just $1,000/month in online earnings can cut this timeline in half.

Step-by-Step Implementation Guide

Step 1: Calculate Your Exact Target Deposit

Don’t aim for a vague “lot of money.” Determine the median home price in your desired area. Decide if you are aiming for a conventional 20% deposit (to avoid private mortgage insurance) or leveraging a first-time buyer program that might only require 3% to 5%.

- Pro Tip: Always add 3-5% extra to your savings goal to cover unexpected closing costs and moving fees.

Step 2: Audit and Optimize Your Expenses

Print out your last three months of bank statements. Categorize your spending into needs and wants. Ruthlessly cut subscriptions you don’t use and negotiate your recurring bills (like internet and car insurance).

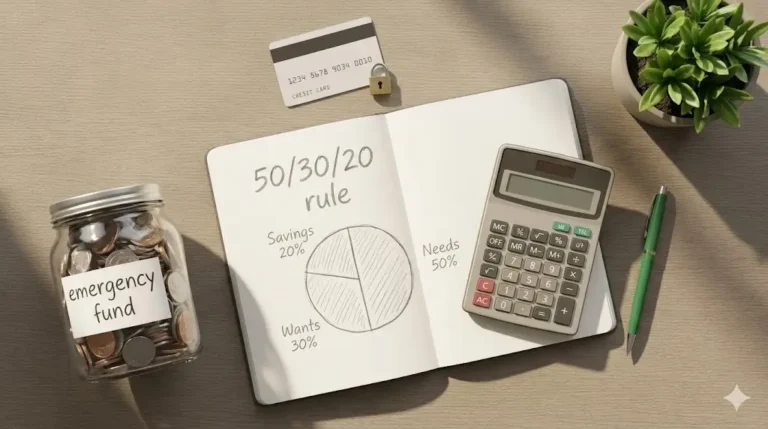

- Insider Trick: Use the 50/30/20 rule as a baseline, but while saving for a house deposit, try to push your savings rate to 30% or even 40% by minimizing your “wants.”

Step 3: Launch a Digital Side Hustle

You can only cut your expenses so much; there is a floor to how little you can spend. However, there is no ceiling to your income potential. Launching a digital side hustle is the ultimate accelerator. Utilize platforms like Upwork or Fiverr to offer services. This allows you to generate work from home revenue streams that go entirely toward your house fund.

- Pro Tip: Treat your side hustle money as if it doesn’t exist. Route these earnings directly into your house deposit account to avoid lifestyle inflation.

Step 4: Automate Your Savings

Relying on memory to transfer money at the end of the month is a recipe for failure. Set up automatic transfers from your checking account to your high-yield savings account the day after your paycheck hits.

Income Potential & Earnings Breakdown

When you rely solely on your primary salary, your savings rate is fixed. By integrating monetization strategies and side hustles, the math changes dramatically.

- Beginner Level (Freelance/Gig Work): $500 – $1,000 per month. (Adds $6,000 – $12,000 annually to your deposit fund).

- Intermediate Level (Consulting/Digital Products): $1,000 – $3,000 per month. Here, your profit margins are higher because you are selling expertise rather than just time.

- Advanced Level (Passive Income Streams): $3,000+ per month. Through affiliate marketing, ad revenue on a blog, or selling digital courses, this income can eventually surpass your day job.

Case Study Example: Sarah, a teacher, was saving $400 a month from her salary. Her timeline for a $40,000 deposit was 8.3 years. By starting a weekend digital marketing side hustle earning an extra $800/month, she tripled her monthly savings to $1,200, achieving her goal in under 3 years.

Alternative Methods & Variations

If the traditional savings route feels too steep, consider these alternative approaches to reach homeownership:

- Low-Deposit Mortgage Schemes: Investigate government-backed loans (like FHA loans in the US) which often require as little as 3.5% down. This drastically reduces the cash you need upfront.

- House Hacking: Buy a multi-family property (like a duplex) with a low down payment, live in one unit, and rent out the other. The rental income pays your mortgage, allowing you to save for your next, ideal single-family home.

- The “Co-Buying” Strategy: Partnering with a trusted family member or friend to pool your resources. This cuts the required deposit in half for both parties, though it requires strict legal agreements.

- Geographic Arbitrage: Utilize your work from home flexibility to move to a lower cost-of-living area. You can save money much faster when your rent is slashed in half.

Best Practices & Optimization Tips

To maximize your results and hit your deposit target as efficiently as possible, follow these optimization strategies:

- Maximize Profit Margins on Side Hustles: If you are freelancing online, continually upskill. Moving from general virtual assistance to specialized software consulting allows you to double your hourly rate without working more hours.

- Bank Your Windfalls: Any unexpected money—tax refunds, work bonuses, or cash gifts—must immediately be deposited into your house fund.

- Use Visual Trackers: Print out a savings thermometer and put it on your fridge. Coloring it in as you hit milestones releases dopamine and keeps you motivated during the long slog.

- Leverage Cash-Back Tools: Use credit cards with high cash-back rewards for your normal daily expenses (paying the balance in full every month, of course) and sweep that cash-back directly into your deposit savings.

Common Mistakes to Avoid

The journey to buying a home is filled with financial landmines. Be mindful of these high-failure-rate pitfalls:

- Falling Victim to Lifestyle Creep: When your online earnings increase, it’s tempting to upgrade your car or wardrobe. Prevention: Stick to your original baseline budget. 100% of new income should go to the house fund.

- Taking on New Debt: Financing a new car or running up credit cards will not only eat into your savings but will ruin your debt-to-income (DTI) ratio, making it impossible to get approved for a mortgage.

- Investing Your Deposit in the Stock Market: If you plan to buy a house within the next 3 to 5 years, do not put your deposit money into volatile stocks or crypto. A sudden market downturn could wipe out your deposit right when you are ready to buy. Keep it safe in an HYSA.

- Forgetting Closing Costs: Many beginners save exactly 20% and forget that closing costs, appraisals, and inspection fees will cost an additional 2-5% of the loan amount.

Long-Term Sustainability & Growth

Saving for a house deposit is an incredible financial boot camp. The habits you build now will set the foundation for lifelong wealth.

Once you secure the keys to your new home, do not abandon the systems you’ve built. The digital side hustle you started? Keep it running. Transition those revenue streams from a “savings fund” to an “investment fund.” Use your newly acquired online earnings to aggressively pay down your mortgage principal, invest in index funds, or save for a rental property. The ultimate goal is not just homeownership, but total financial freedom where passive income covers your mortgage entirely.

Conclusion

Saving for a house deposit in the modern era requires a dual approach: ruthlessly optimizing your current expenses while aggressively expanding your income potential through side hustles and digital ventures. By automating your savings, avoiding new debt, and leveraging high-yield accounts, that set of keys is closer than you think.

Ready to start your journey? Drop your biggest savings challenge in the comments below! Don’t forget to subscribe to our newsletter for weekly money-making strategies, and share your progress in our community. Let’s get you into your dream home!

FAQs

How much money can I realistically make from a side hustle to fund my deposit?

Beginners can realistically make an extra $500 to $1,000 a month with consistent effort in digital freelancing or gig work. As you build your skills, this income potential can grow to $2,000+ per month, significantly reducing your saving timeline.

Do I need prior experience to start generating digital income?

No! There are plenty of beginner-friendly online monetization strategies, such as virtual assistance, data entry, and basic content writing, that require zero prior experience—just a willingness to learn and a reliable internet connection.

What is the minimum initial investment needed to start saving?

To start saving, your initial investment is $0. Simply open a free high-yield savings account. If you’re starting a side hustle to accelerate your savings, most digital service-based businesses can be started with just a laptop and free software.

How long until I see results and reach my house deposit goal?

If you rely only on a strict budget, it takes an average of 3 to 5 years to save a deposit. However, by adding multiple revenue streams, many readers achieve their deposit goals in 18 to 24 months.

Is working from home and freelancing still a viable way to save money in the current year?

Absolutely. The digital economy is larger than ever. Businesses are constantly outsourcing work to freelancers, making it one of the most reliable ways to generate supplemental income for your house deposit.

What are the risks involved in saving for a house deposit?

The main risk is inflation outpacing your savings rate, which is why keeping your money in a high-yield account is crucial. Another risk is investing short-term savings into volatile markets (like stocks or crypto) which could result in a loss of principal right before you need to buy.